GBPUSD TECHS: Bears Remain In The Driver's Seat

- RES 4: 1.2550 50-day EMA

- RES 3: 1.2548 High Sep 11 and Low Aug 25

- RES 2: 1.2351/2425 High Sep 21 / High Sep 19

- RES 1: 1.2265 High Sep 25

- PRICE: 1.2146 @ 05:58 BST Sep 27

- SUP 1: 1.2120 76.4% retracement of the Mar 8 - Jul 14 bull leg

- SUP 2: 1.2075 38.2% retracement of the Sep ‘22 - Jul ‘23 bull leg

- SUP 3: 1.2028 Low Mar 16

- SUP 4: 1.2011 Low Mar 15

GBPUSD remains in a clear downtrend and the pair traded lower again Tuesday. Support at 1.2308, the May 25 low, was breached last week. The move down confirms a resumption of the bear trend and maintains the bearish price sequence of lower lows and lower highs. The focus is on 1.2120, a Fibonacci retracement. On the upside, initial firm resistance is seen at 1.2425, the Sep 19 high. Short-term gains would be considered corrective.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SCHATZ TECHS: (U3) Corrective Cycle Remains In Play

- RES 4: 105.325 High Jun 14

- RES 3: 105.295 High Aug 8 and a key resistance

- RES 2: 105.255 High Aug 9

- RES 1: 105.230 High Aug 24

- PRICE: 104.995 @ 05:24 BST Aug 28

- SUP 1: 104.905/760 Low Aug 23 / 15 and the bear trigger

- SUP 2: 104.741 76.4% retracement of the Jul 6 - Aug 8 bull leg

- SUP 3: 104.620/104.570 Low Jul 11 / 6 and the bear trigger

- SUP 4: 104.470 2.00 projection of the Jun 1 - 8 - 12 price swing

Schatz futures rallied last Wednesday resulting in a move above both the 20- and 50-day EMAs. The break higher signals scope for a stronger short-term recovery and an extension would expose the next key resistance at 105.295, the Aug 8 high. Moving average studies continue to highlight a downtrend and this suggests recent gains are part of a correction. Support to watch lies at 104.905, the Aug 23 low. A break would be bearish.

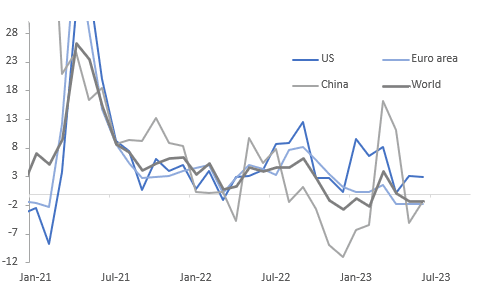

GLOBAL: Asia & Euro Area See Weak Export Volumes

CPB data showed global export volume growth remained weak in June in both developed and emerging nations, especially in Asia. Advanced economies’ export growth rose 0.2% m/m to be down 0.6% y/y an improvement from -1.6% and outpacing EM which fell 1% m/m to be down 2.6% y/y after -0.5% y/y. Annual export growth contracted across Asia, except Japan which returned to positive territory, but generally saw some improvement.

- Export volumes from Japan grew 1.1% y/y in June after falling 3.5%, whereas advanced Asia ex Japan fell 3.8% y/y but improved from May’s -6.4%.

- China’s exports fell 1.3% y/y after falling 5.1%, while emerging Asia ex China saw shipments worsen to -8.4% y/y from +0.2% in May.

- The euro area was another weak spot in June with volumes falling 1.7% y/y after -1.8%. The UK on the other hand saw growth of 4.9% y/y. The US continued its run of positive outcomes since April 2022 with exports growing 2.9% y/y in June.

Source: MNI - Market News/Refinitiv/CPB

AUSSIE BONDS: Mixed, Near Session Cheaps, RBA Bullock Speaks Tomorrow

ACGBs (YM -3.0 & XM flat) are dealing at or near session lows. Retail sales data for July printed stronger than expected, although additional spending at catering and takeaway food outlets linked to the 2023 FIFA Women’s World Cup and school holidays boosted the overall result.

- The cash ACGB curve has bear-flattened, with yields flat to 2bp higher. The AU-US 10-year yield differential is 1bp higher at -7bp, after dealing at -10bp earlier in the local session.

- Swap rates are higher, with pricing flat to 2bp higher. EFPs are little changed, with the curve flatter.

- The bills strip has bear-steepened, with pricing -1 to -5.

- RBA-dated OIS is 2-8bp firmer for meetings beyond November, with Sep’24 leading.

- S&P Global Ratings reported that home loan arrears remained very low in Q2 rising to 0.97% for prime mortgages from 0.95% in Q1 and falling to 3.47% for non-prime from 3.7% due to the number of loans increasing. However, Roy Morgan released data showing the number of people at risk of mortgage stress rising 642k on a year ago to a record 1.5mn in the 3 months to July. (The Australian)

- Tomorrow the local calendar sees a speech from RBA Governor-Elect Bullock, titled “Climate Change and Central Banks”. On Wednesday, the CPI Monthly for July is on tap.