GILTS: Bearish U-Turn Ahead Of Huge Data Week

Between the surprisingly strong UK GDP print this morning and US PPI data this afternoon, UK rates have staged an impressive bearish U-turn.

- BoE peak hike pricing has rebounded smartly and suddenly looks set to finish the week higher. Not long after Thursday's softer-than-expected US CPI print, BoE terminal pricing to Mar 2024 had slipped to a post-June 13 low close of 5.73% after 6 falls in 7 days. Today it's up nearly 8bp at 5.81%, up 3bp on the week. September hike pricing has firmed 3bp, with a 25bp hike now 92% priced, vs 80% yesterday.

- Meanwhile the UK curve has bear steepened: 10Y yields have popped to the highest since Jul 13, up 17bp on the day and 21bp from Thursday's low. A close around here could mark the 2nd biggest daily rise of the year (Feb 6th's 19bp rise is the high).

- Notably the drift lower in rates earlier this week has come without much of a UK-specific driver, which will stand in stark contrast with the major docket of UK data next week including labour market numbers on Tuesday and CPI on Wednesday, with retail sales rounding out the schedule next Friday.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CANADA: Macklem: Base Case For No Recession

Q: We still haven’t got the recession that people were talking about last year. Are we still talking about a soft landing or is a recession on the cards.

A: Macklem: Growth has surprised on the upside. We still think that the increases in rates are still feeding through to the economy. Our forecast shows a path to price stability with no recession.

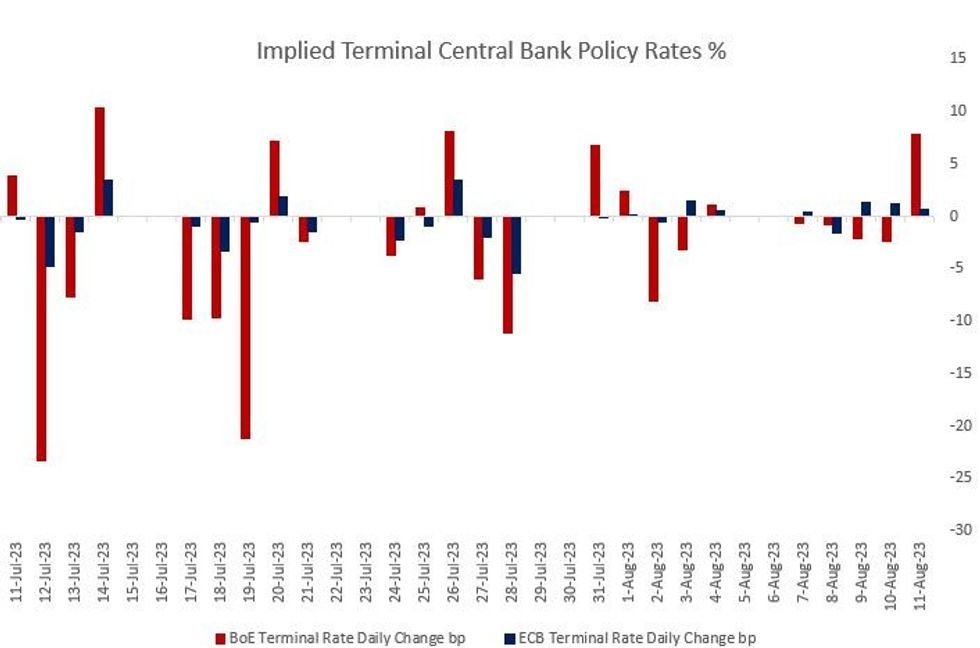

STIR: Post-CPI Drop Wipes Out July's Rise In BoE Peak Hike Pricing

BoE terminal rate pricing continues to fall following the softer-than-expected US inflation report, with OIS implying Mar 2024 Bank Rate at 6.26% (126bp of further hikes left in the cycle, -22.6bp on the day).

- If this holds, all of July's rise will have been wiped out - nearly one 25bp hike has been removed from the cycle today alone, and 40bp from the July peak. August MPC pricing is down to 42bp (from 46bp coming into the week).

- ECB pricing has been less impacted, off 3.2bp on the day but still holding on to the 4% level (at 4.01%, 51bp of further hikes are priced to Dec 2023).

Source: MNI, BBG

Source: MNI, BBG

STIR: Mixed Midday Trade

Surge in post-data call structure buying ebbs slightly ahead midday, tactical reversals noted with some chunky put spread buys as underlying futures drift near highs.

- +5,000 SFRH4 96.00/97.00 call spds, 10.0

- Block, 25,000 SFRU3 94.62/94.87 2x1 put spds, 14.0 ref 94.615

- appr 30,000 SFRU3 94.50 puts, 2.75 ref 94.615