EU BASIC INDUSTRIES: BASIC INDUSTRIES: Week in Review

Sep-06 13:15

- Macro concerns linger with iron ore hovering around the lows, while weak Germany and France Industrial Production data will be a concern to the beleaguered chemical sector.

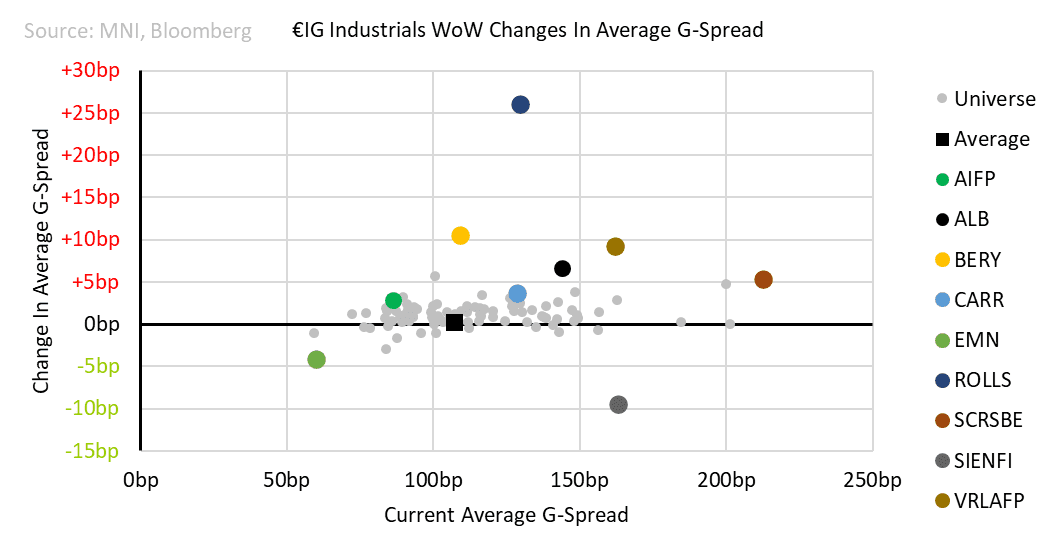

- Rolls-Royce was in focus with defective fuel lines discovered in some A350s with Trent XWB-97 engines. While there were tail risks, this has always looked manageable, and the latest updates point in that direction too. Tests can be carried out without removing the engine and are rolling out swiftly with most planes finding no issues. Nonetheless, spreads are 26bp wider on the week with 14bp coming from the bund rally; as a former HY name the bonds are still quoted on cash price, 35c lower on the week.

- Givaudan signalled M&A interest, with no impact on spreads so far. This could be a slow burner and unlikely to be transformational but worth watching with spreads here.

- Arkema was the only name active in primary with a 10Y deal.

- MTU Aero Engines made double headlines with Moody’s moving from outlook stable to positive and a 7Y mandate announced.

- Spreads generally held up well, with crossover names taking the impact of lower rates. Albemarle sentiment remains weak following the Fitch downgrade to BBB- last week with Lithium prices still pressured on oversupply as EV adoption forecasts continue to deteriorate.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY FUTURES: BLOCK: Sep'24 2Y Sale

Aug-07 13:13

- -5,000 TUU4 103-10.62, sell through 103-10.75 post time bid at 0907:56ET, DV01 $191,000. Contract trades 103-10.12 last (-1.25).

GILTS: Early Ranges Prevail, Initial Support In Futures Intact

Aug-07 13:11

Gilt futures have failed to re-test this morning’s low, leaving initial support at the Jun 21 high (99.23) untouched. Contract last -41 at 99.55

- The pullback from this week’s high represents an unwind of overbought conditions, with the technical trend remaining bullish.

- Yields little changed to 4bp higher, steepening theme intact.

- 2s10s hit fresh ’24 highs today, while 5s30s is still shy of its January YtD peak after failing to break above that level on Monday.

- UK headline flow remains subdued, with no meaningful risk events scheduled until next week’s labour market and CPI data.

PIPELINE: Corporate Issuance Roundup: Off Sidelines as Markets Calm Down

Aug-07 13:03

- Date $MM Issuer (Priced *, Launch #)

- 8/7 $Benchmark Meta Platforms 5Y +80a, 7Y +95a, 10Y +105a, 30Y +140a, 40Y +155a

- 8/7 $Benchmark BMW 2Y +100a, 2Y SOFR, 3Y +110a, 3Y SOFR, 5Y +135a, 7Y +150a

- 8/7 $Benchmark VW Group 2Y +110a, 2Y SOFR, 3Y +125a, 5Y +150a

- 8/7 $Benchmark Coca-Cola 10Y +100a, +30Y +125a, 2064 tap+140a

- 8/7 $Benchmark HCA Inc, 4/1/31 tap +150a, 10Y +175a, 30Y +200a

- 8/7 $Benchmark Sherwin-Williams +3Y +110a, 7Y +140a

- 8/7 $Benchmark Quanta Services 3Y +125, 10Y +160a

- 8/7 $Benchmark Unilever Capital 3Y +80a, 10Y +110a

- 8/7 $Benchmark BorgWarner 5Y +150a, 10Y +175a

- 8/7 $Benchmark GE Healthcare 5Y +140a

- 8/7 $Benchmark D.R. Horton 10Y +150a

- 8/7 $1.5B Lightning Power 8NC3 7.5%a

- 8/7 $500M Idex WNG 5Y +145a