COLOMBIA: BanRep Governor Villar Says Central Bank Risks Losing Credibility

- Speaking at a banking conference in Cartagena earlier, BanRep Governor Villar reiterated his hawkish stance as he said that additional interest rate hikes may be needed, following last week's larger-than-expected 100bp increase.

- Villar said that recent policy rate decisions have been painful and that the central bank needed to act as it risks losing its inflation-targeting credibility.

- As a reminder, sell-side analysts expect the Board to continue its aggressive hiking cycle ahead, with perhaps a 50bp move in March and 100-200bp of further tightening in total this year.

- Separately, Public Credit Director Javier Cuellar said at the same conference that the government will present a financing plan in the coming days.

- "*Colombia risks losing inflation-targeting credibility: Villar" – BBG

- "*Villar says Colombia low unemployment probably unsustainable"

- "*Colombia primary fiscal deficit is pressuring inflation"

- "*Intervention to affect Colombia peso level doesn't work"

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

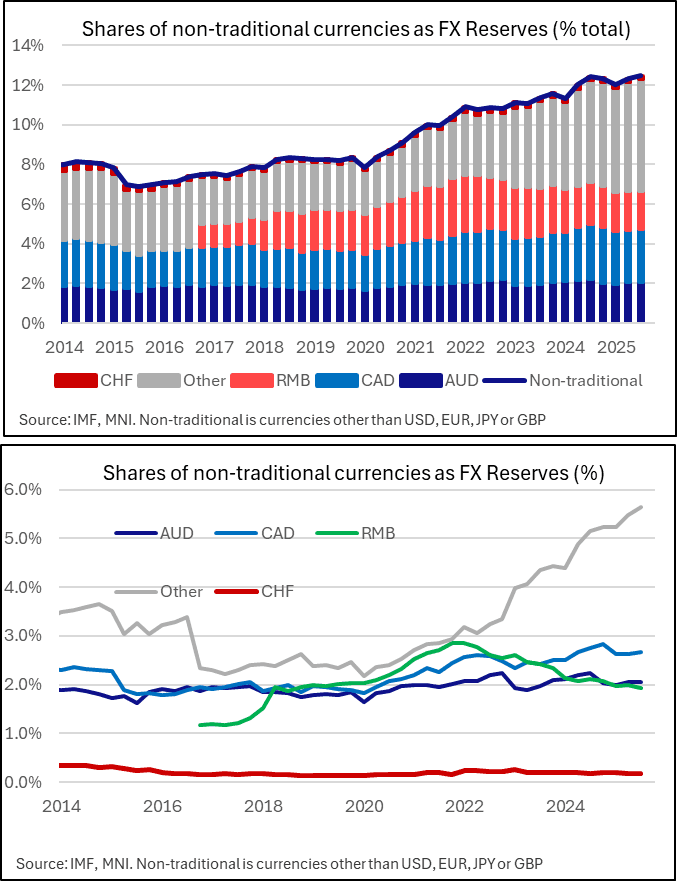

FOREX: “Other” Category’s Share Of Non-traditional FX Reserves Still Growing

The share of FX reserves accounted for by “non-traditional” currencies (that is, not USD, EUR, JPY and GBP) ticked up to 12.5% (vs 12.3% in Q2). Within this basket, the “other” category continues to increase (5.6% in Q3 vs 5.5% in Q2, 5.0% in Q1).

- There is no detail within this “other basket”, which reflects the likes of NOK, SEK, NZD and EM currencies.

- Late last year, the FT summarised an analysis from Standard Chartered, which tried to estimate the most likely candidate "other" currencies. Summarising Standard Chartered via this FT report: "Surprisingly, a number of statistical threads point to NOK as a major component of the ‘other currencies’ component of reserves. It stands out as the currency that is most correlated with changes in the USD value of other reserves. Changes in ZAR, SEK and NZD also have consistently high correlations with changes in the other currency reserves, and they are also frequently mentioned as reserve currencies. Our judgment is that correlations over 0.70 represent some presence in reserve portfolios. Changes in SGD, COP, THB, PLN, IDR and KRW provide a second tier of correlation with changes in ‘other currencies’ at around 0.60".

- It’s of course important to remember that these markets are very small in the context of the global reserve system. However, in the case of the Scandis, increased availability of local currency assets in Sweden (higher bond issuance) and Norway (central bank certificates) could generate some additional reserve diversification flows on the margin in the quarters ahead.

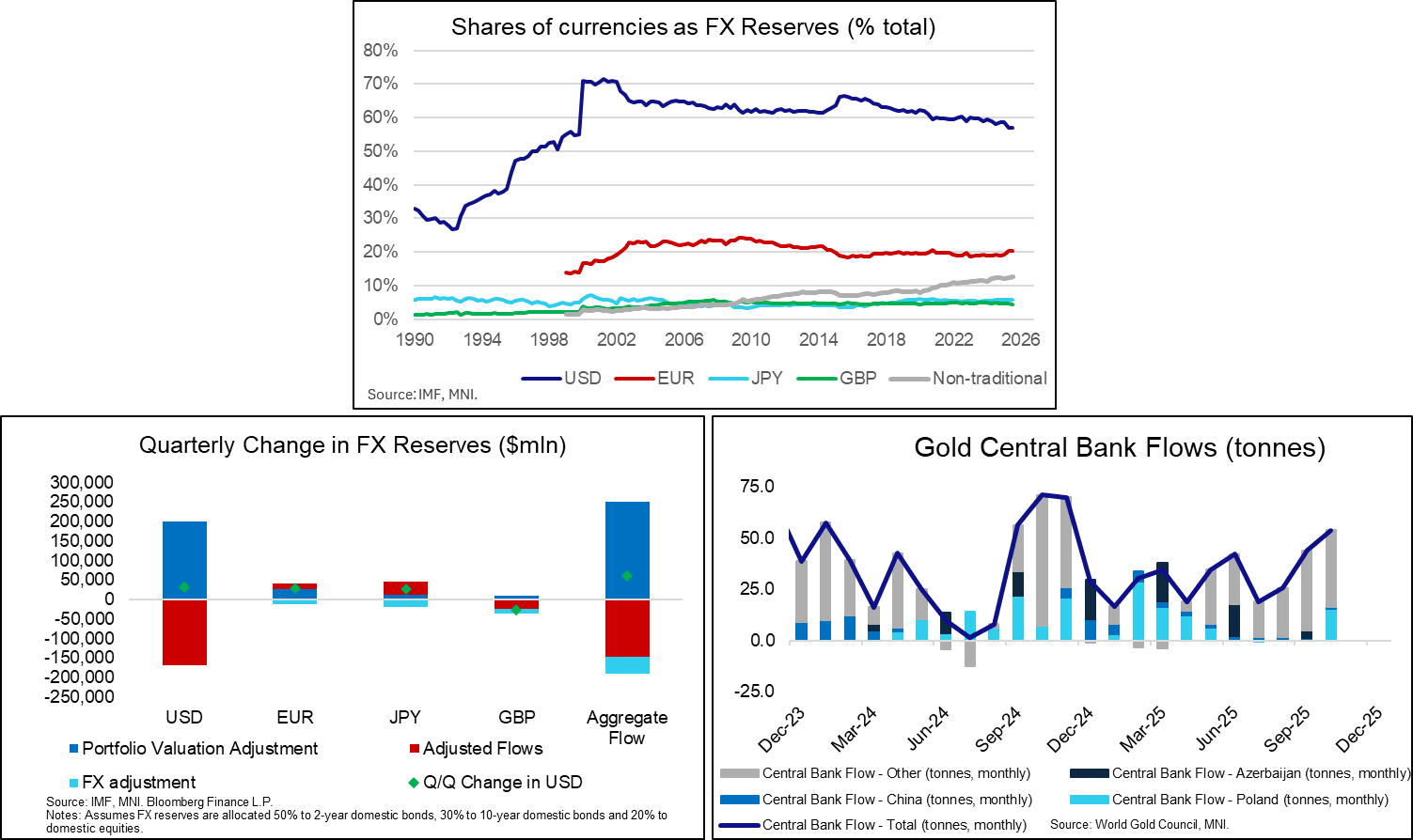

FOREX: IMF Q3 COFER Data Points To Valuation Adjusted USD Selling In Q3

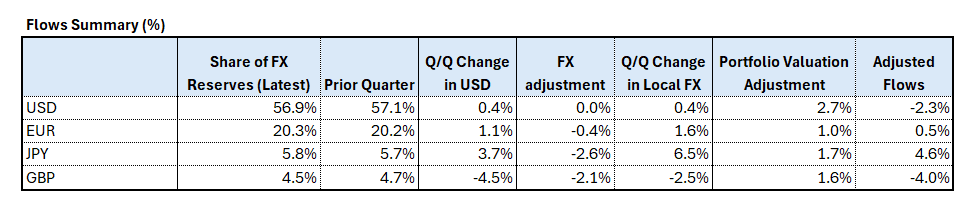

IMF COFER data for Q3 was released before the Christmas break. A profound fear for markets after Liberation Day 2025 was a broad, one-way diversification out of dollars for reserve managers. The data provides some evidence of movements out of the dollar, but these changes are still occurring at a glacial pace. The USD’s share of total reserves fell to 56.9%. This was little changed from Q2’s 57.1% but still the lowest proportion since 1999 (i.e. prior to an IMF methodological change noted below). We estimate that portfolio valuation effects prevented a larger fall in the USD’s share of total reserves.

- We estimate “actual” net FX reserve flows using basic portfolio allocation assumptions and exchange rate changes. We assume that reserves in a given currency are allocated 50% to domestic 2-year bonds (e.g. 2-year USTs for USD), 30% to domestic 10-year bonds and 20% to domestic equities (e.g. S&P 500 for USD).

- We estimate that the 0.4% Q/Q rise in USD reserves (to $7.414trln) represented a 2.7% increase in portfolio valuations, offset by a 2.3% decrease in actual USD reserve holdings.

- See the table below for adjusted flows in USD, EUR, JPY and GBP.

- The USD value of total reserves rose by ~$90bln to $13.025trln in Q3, with USD, EUR, JPY and GBP reserves rising ~$60bln to $11.4trln. Considering these four currencies only, we estimate a portfolio valuation and FX adjusted net flow of minus $146bln (portfolio valuations increased $250bln, offset by $43bln of FX adjustments).

- That may provide evidence in favour of increased build-up of non-FX reserves such as gold. World Gold Council data indicates that central bank gold buying accelerated through Q3 (and continued in October). Central Banks reportedly purchased 88.7 tonnes of gold in Q3, after 96.1 tonnes in Q2 and 81.8 tonnes in Q1. These flows remain one bullish structural driver of the gold price, with reserve managers generally considered less price sensitive than traditional institutional/retail investors.

- Note: “Starting in 2025Q3, with revisions back to 2000Q1, the COFER dataset no longer includes an unallocated component”: See here for more

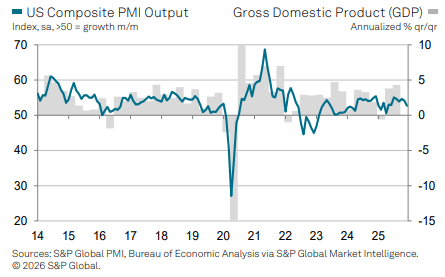

US DATA: Final Service PMI Trimmed In Dec, Input Cost Inflation Sting Softened

The final S&P Global US services PMI was revised lower for December for a joint low with June and last lower in April after wide-ranging tariff announcements at the time. New orders saw their weakest increase in over eighteen months (chiming with the 20-month low in the flash release) whilst services cost inflation was revised a little softer but still clearly very strong (operating expenses increased by their most since last May vs the steepest in over three years in the flash). The composite activity index points to downward momentum in Q4 real GDP growth after the strong 4.3% annualized in Q3.

- Services PMI: 52.5 in Dec final (flash and cons 52.9) after 54.1 in Nov.

- Composite PMI: 52.7 in Dec final (flash 53.0) after 54.2 in Nov.

- The downward revision for services is in contract to the unrevised final manufacturing reading reported last week.

Opening highlights from the S&P Global press release (full release here):

- “The US service sector continued to expand at the end of 2025, according to the latest PMI data from S&P Global.

- However, with new business inflows rising to the weakest degree in over a year-and-a-half, growth of activity faltered and was the lowest since last April. Confidence in the outlook also weakened, whilst employment volumes stagnated, failing to rise for the first time since last February.

- Tariffs and higher labor-related costs meanwhile drove typical operating expenses up to the greatest degree since last May. Firms passed on their higher costs by raising selling prices at a quicker pace.”