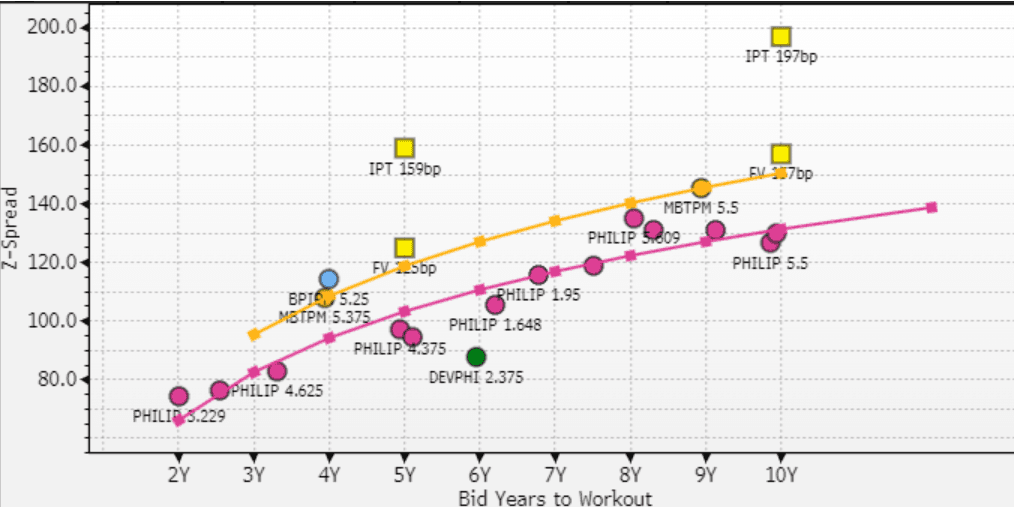

EM CREDIT SUPPLY: Bank of the Philippine Isl.(BPIPM, Baa2/BBB+/BBB-) - $ deal FV

We provided a fair value estimate yesterday on a possible 5y and 10y deal, the rational indicated below. Compared to yesterday we adjusted the 5y estimate a few bp wider, maintaining the 7bp spread to the Metropolitan Bank & Trust Company (MBTPM) $ curve.

New Issue: $Benchmark 5y & 10yr fixed

IPT 5y: T+130a (z+159bp)

FV 5y: T+96bp (z+125bp)

IPT 10y: T+155a (z+197bp)

FV 10y: T+117bp (z+159bp)

Bank of the Philippine Islands (BPIPM), one of the largest in the Philippines, is coming to the market with a $ 5y fixed and 10y fixed deal. Fair value estimates to follow.

The company reported full year results early February, which were more or less in line with expectations. Net income rose 20% YoY to PHP62bn on the back of record revenues. Balance sheet and asset quality metrics were weaker however, with a CET1 ratio at 13.8% (-150bp YoY) and NPL ratio at 2.13% (+29bp YoY).

In terms of a fair value for a theoretical 5y and 10y fixed, we compare the existing Bank of the Philippine Islands $ 3/29 to Metropolitan Bank & Trust Company (MBTPM) $ curve, as well as the more liquid Philippines sovereign curve.

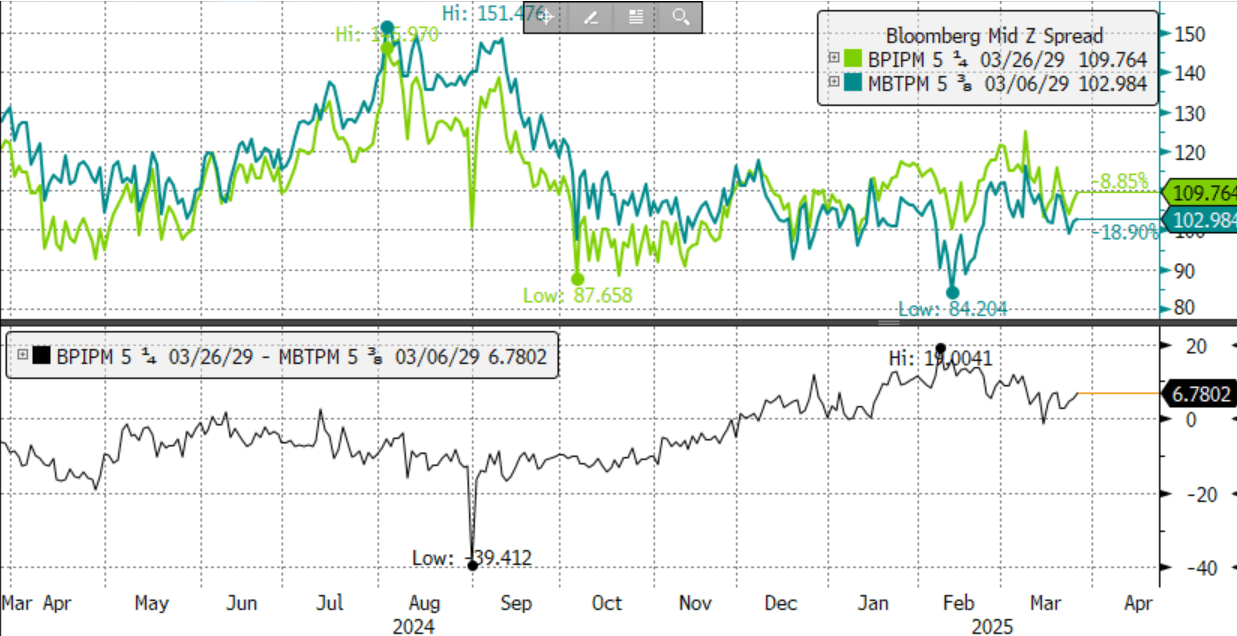

We note (see chart) that the recent spread differential between the BPIPM and MBTPM 2029 bonds has recently indicated BPIPM trading around 7bp wide to MBTPM, which we use as a guide to fair value. For a 5yr we estimated FV at z+125bp area (T+96bp) and a 10y at z+157bp area (T+117bp).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: Asian Equites Drop As Tech Stocks Take A Beating

Asian equities declined sharply, with the MSCI Asia Pacific Index falling as much as 1.4%, led by losses in Chinese technology stocks following Donald Trump’s latest measures targeting Chinese investments. Alibaba (-7.9%), Tencent, and TSMC were among the biggest drags, while the Hang Seng Tech Index tumbled 4.4%, its worst drop since November.

- Hong Kong and mainland Chinese stocks led regional losses as investors reassessed geopolitical risks after Trump’s new directive to restrict Chinese investments in US tech and strategic sectors. This triggered profit-taking in AI-related stocks, which had previously rallied on optimism surrounding DeepSeek and President Xi’s engagement with corporate leaders. The HSI is -1.70%, while the CSI is -0.70%.

- Japan’s markets opened lower after a three-day break, with the Nikkei 225 down 0.95% as concerns over AI demand weighed on sentiment. Hitachi (-6.2%) dragged the Topix 0.40% lower, while trading houses like Mitsubishi Corp. gained after Warren Buffett signaled a potential increase in his Japanese holdings.

- Australia's ASX 200 is 0.80% lower as corporate earnings drove stock-specific volatility. Adairs tumbled 12%, extending Monday’s losses after reporting 1H25 EBITDA of A$39.1M, well below the A$61.5M consensus estimate, with revenue also missing expectations. Zip surged 16% after providing strong full-year revenue guidance, posting record cash earnings, and reporting a 40.3% YoY increase in US TTV, reinforcing confidence in its FY25 two-year targets. Domino’s fell 11% after reiterating a 1H loss, citing ongoing weakness in France and Japan.

- Elsewhere, South Korea’s central bank cut rates by 25bps to 2.75%, a widely expected move, the KOSPI is 0.20% lower, while Taiwan's TAIEX is -1.30% as TSMC trades -1.90% lower. Meanwhile, oil edged higher, gold hovered near record levels, and US 10yr yield slipped to 4.4% as investors sought safe havens amid rising geopolitical tensions and anticipation of Nvidia’s earnings later this week.

STIR: RBA Dated OIS Pricing Mixed Relative To Pre-RBA Levels

RBA-dated OIS pricing is steady to 6bps softer across meetings today, with late 2025 and early 2026 leading the decline.

- As a result, pricing is now mixed compared to last Tuesday’s pre-RBA levels—meetings through September are flat to 3bps firmer, while those beyond are 2-4bps softer.

- This shift comes despite RBA Governor Bullock cautioning that market expectations for further rate cuts are not assured.

- Markets assign a 13% probability to a 25bp rate cut in April, with a cumulative 53bps of easing priced by year-end, based on an effective cash rate of 4.09%.

Figure 1: RBA-Dated OIS – Today Vs. Pre-RBA Levels

Source: MNI – Market News / Bloomberg

AUSSIE BONDS: Richer & At Session Bests Despite Post-Cut Rebound In Cons Conf

ACGBs (YM +4.0 & XM +3.5) are stronger and at Sydney session highs.

- Today, the local calendar is light, ahead of January's CPI Monthly tomorrow.

- Australian consumer confidence strengthened last week to mark its highest level since May 2022 as households cheered the RBA's first rate cut since the pandemic, according to ANZ and Roy Morgan Research.

- Cash US tsys are ~2bps richer in today’s Asia-Pac session after yesterday’s gains.

- Cash ACGBs are 4bps richer with the AU-US 10-year yield differential at +2bps.

- Swap rates are 3-4bps lower.

- The bills strip has bull-flattened, with pricing +1 to +5.

- The AOFM plans to sell A$800mn of the 3.75% 21 April 2037 bond tomorrow and A$700mn of the 1.75% 21 November 2032 bond on Friday.