ITALY: Bank of Italy Cuts 2026 GDP Forecast By Two Tenths

"*BANK OF ITALY CUTS 2026 GDP FORECAST TO 0.6%; PRIOR 0.8%" Bloomberg

The Bank of Italy's 0.6% projection for 2026 is a tenth below the Government's 0.7% projection in its budget plan.

- We've previously noted that the biggest risk facing italian fiscal consolidation is the growth outlook, rather than primary balance dynamics.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CANADA: Lower Bound of CADJPY Range in Focus as BOC Awaited

- A sharp sell-off in USDCAD this week amid the broad greenback weakness has resulted in a break of the 20-and-50-day EMAs. This undermines a recent bullish theme, and spot has significantly narrowed the gap to key short-term support at 1.3727, the Aug 27 low.

- A break of this level would strengthen a bearish threat and targets on the downside would include 1.3637 and 1.3576, lows from late July.

- The Bank of Canada is expected to cut its benchmark overnight rate by 25bp to 2.50% today. Data since the July meeting have been almost unambiguous in tilting the balance toward a further easing, culminating with softer core CPI trends in August’s inflation report released yesterday. Our full preview is here: https://mni.marketnews.com/48mKSq9

- With the statement broadly expected to leave the door open to another rate cut in October, any dovish reaction for Canadian assets would place the focus on EURCAD, which broke to fresh cycle highs on Tuesday, continuing to place the cross at the highest level since 2009. 1.6329 provides the next horizontal resistance point.

- In similar vein, there have been a cluster of daily lows around the 106.00 mark for CADJPY, and a break below this point would highlight a S-T range breakout, initially targeting 104.85, the July 01 low.

SWEDEN: MNI 2026 Swedish Budget Preview

Click here for the full PDF analysis

The Swedish 2025 budget bill will be presented in full on Monday (Sep 22), the day before the Riksbank decision. In total, SEK80bln of unfunded reforms are set to be presented, excluding defence spending/military aid to Ukraine. The Government has been announcing details of the budget over the past few weeks – we estimate just over SEK60bln (out of SEK80bln) has been announced so far.

- The most significant unfunded reforms include a temporary reduction in food VAT (SEK15.9bln in 2026), a reduced tax on work and pensions (SEK21.4bln in 2026), a reduced electricity tax (SEK6.5bln in 2026) and a temporary reduction in employer contributions for the hiring of young people (SEK6.1bln in 2026).

- There are broadly two channels for markets the consider with respect to the budget: The impact on Riksbank (i.e. monetary) policy and the impact on National Debt Office/NDO (i.e. issuance) plans.

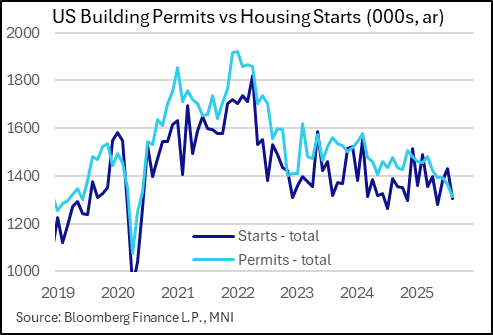

US DATA: Housing Activity Resumes Downtrend After Nascent Summer Pickup

Residential construction activity fared worse in August than expected, with building permits hitting fresh cycle lows after a brief uptick was seen in June and July.

- Permits came in at 1,312k (SA annualized), a drop of 50k from prior and well below the 1,370k consensus. This marks a new cycle low for this key leading indicator of construction activity, with the prior low set at the start of the pandemic in 2020 and before that, June 2019. Permits have only risen % M/M in 2 of the last 12 months, and are now down 11.1% Y/Y.

- Multi-unit permits fell 6.4% to 456k, the 2nd-lowest since 2020, with single-family permits down 2.2% to 856k, a 29-month low. Most of the weakness in volume terms is concentrated in the US South region, which experienced a boom in the early stages of the pandemic as Americans relocated. It's still the biggest region for permits by far (691k vs 621k for the Northeast, Midwest, and West combined in August), but has now fallen sharply in 4 of the last 5 months including 10% in the last 2 months alone.

- It was a similar story for housing starts, which basically lag permits. They fell 122k in August to 1,307k SA ann., vs 1,365k expected, with weakness in both single-family and multi-unit starts. That's not quite a fresh cycle low, with May having seen 1,282k, but likewise it appears that the Jun/Jul jump may have been fleeting.

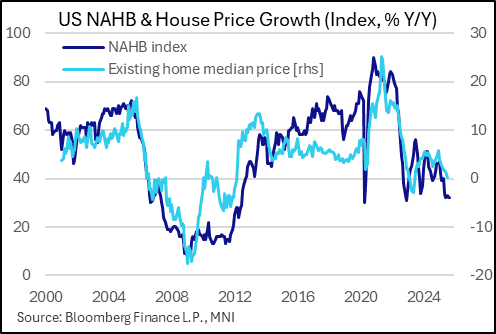

- Little improvement is expected. The NAHB Housing Market Index for September released Tuesday showed continued weakness in single-family homebuilder sentiment, with a headline score of 32 (33 expected, 32 prior), near the historic lows it's been for the last 4 months (ticked up to 33 in July), amid weak prospective buyer traffic and present sales offset by a small tick-up in expected future sales (still at depressed levels). And per the NAHB, "39% of builders reported cutting prices in September, up from 37% in August and the highest percentage in the post-Covid period".

- Estimates for residential investment have fallen since the start of the quarter, with the Atlanta Fed's GDPNow initially showing an expected 1.8% Q/Q SAAR growth in the category in Q3 after -4.7% in Q2 and -1.3% in Q1; however that's fallen to -4.6% in the latest update (albeit off the low of -8.2% seen after housing starts and home sales figures for July). We would expect the estimate to be pulled back again after this data.

- Apart from the GDP growth impact, it's likely house prices will continue to soften amid extraordinarily low affordability metrics and a softening labor market.