US TSYS: Back To Little Changed, Claims Details and Supply Watched

Oct-09 10:49

- Treasuries have recently pared losses for back little changed on the day, having held yesterday’s ranges throughout whilst consolidating the flattening seen.

- Today sees likely another unusual jobless claims release with the potential for state-level figures to be published but not a national print. Supply could also see some attention with heavy bill issuance plus 30Y supply after yesterday’s somewhat soft 10Y auction.

- Cash yields range from 0.4bp higher (2s) to 0.2bp lower (30s).

- 5s30s around 99bps is back at late September levels, having troughed at 96bp on Sep 29 for its lowest since late Jul/early Aug.

- TYZ5 trades at 112-21 (+01+) having held within yesterday’s narrow range throughout, on subdued cumulative volumes of 195k.

- The contract earlier this week quickly lifted back above the 50-day EMA (currently 112-13) after a short-lived clearance, but doesn’t yet trouble resistance at 113-00 (Sep 24 high). The trend structure remains bullish.

- Data: Weekly jobless claims (0830ET), where, as with last week, we could see state-level figures released but not the national print. The wholesale trade report, nominally at 1000ET, is unlikely to be released.

- Fedspeak: Our focus is on Gov. Barr at 1245ET - see separate Fed bullet

- Coupon issuance: US Tsy $22B 30Y bond auction re-open - 912810UM8 (1300ET). Yesterday’s 10Y tailed by 0.5bp and the bid-to-cover slipped from 2.65 to 2.45. Last month’s 30Y was on the screws whilst the bid-to-cover was more promising as it increased from 2.27 to 2.38.

- Bill issuance: US Tsy $110B 4W & $95B 8W bill auctions (1130ET)

- Politics: Trump hosts cabinet meeting (1100ET), Trump in bilateral meeting with President of Finland (1015ET)

- QT matters: Yesterday’s FOMC minutes are starting to eye a QT endgame. SOMA deputy manager Remache, (who late last month spoke on how to identify a reserve regime shift from "abundant" to "ample") said that with QT running at the current pace and overnight reverse repo facility usage remaining "very low", reserves were expected "to be close to the $2.8 trillion range by the end of the first quarter of next year if runoff were to continue at the current pace." That's a level that would probably be considered by most on the FOMC to be in or near "ample" territory (Gov Waller in July identified $2.7T as a "rough" guess).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

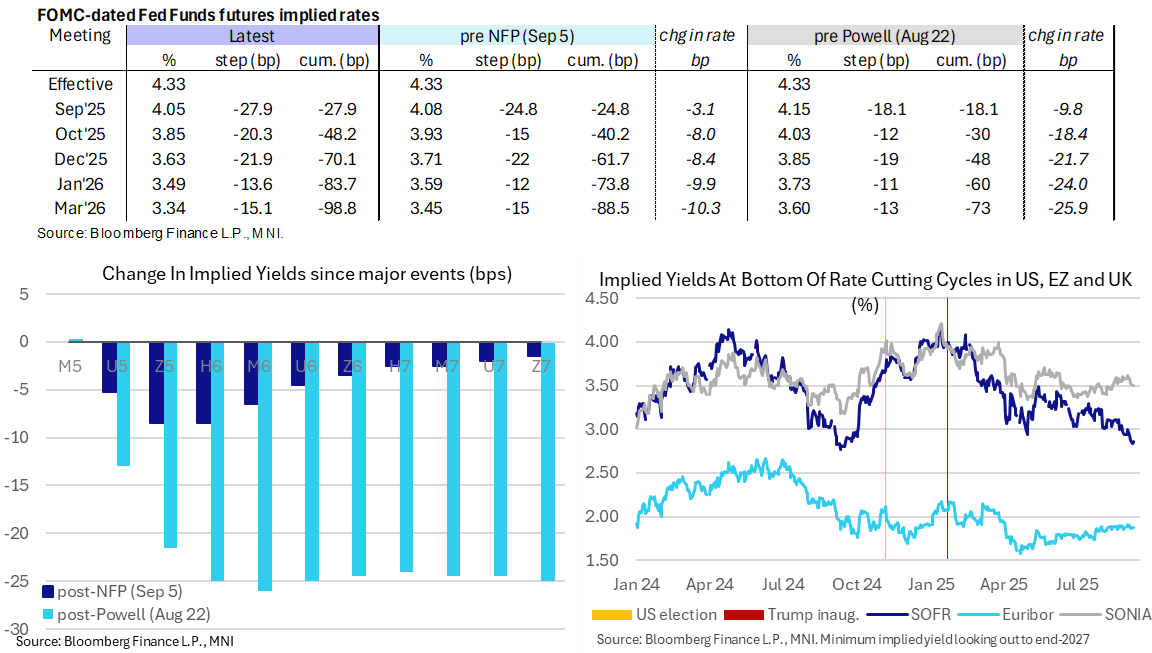

STIR: 70bp Of Fed Cuts Seen To Year-End With Payroll Revision Estimate Eyed

Sep-09 10:31

- Fed Funds implied rates are 1.5bp higher on the day for end-2025 rates, pulling a little further away from fully pricing three consecutive rate cuts, but remain within post-NFP ranges ahead of payrolls benchmark revisions at 3pm.

- Cumulative cuts from 4.33% effective: 28bp Sep 17, 48bp Oct, 70bp Dec, 83.5bp Jan and 99bp Mar.

- The SOFR implied terminal yield of 2.86% (SFRH7) is 2bp higher on the day after yesterday saw a fresh lowest close since Sept 2024 (when it saw cycle lows in the high 2.7s), hovering just shy of 150bp of cuts ahead from current levels.

- Today’s US macro docket is headlined by the preliminary estimate for payrolls benchmark revisions at 1000ET. There’s a wide range of estimates here but we judge the median expectation to be circa -750k. MNI Preview: https://media.marketnews.com/US_Prelim_Benchmark2025_Preview_f1d718139b.pdf

- On a related note, the WSJ reports that advisers to President Trump are preparing a report laying out alleged shortcomings of the BLS’s jobs data including revisions.

- Tomorrow (Sep 10), the Senate banking committee will vote to approve CEA's Miran for the Fed Board of Governors at 1000ET. He would still have to be approved by the full Senate to be fully confirmed but this is moving quickly enough to assume that he will be at the FOMC table at the Sept 16-17 meeting.

LOOK AHEAD: Tuesday Data Calendar: BLS Survey Revision, 3Y Note Sale

Sep-09 10:28

- US Data/Speaker Calendar (prior, estimate)

- 09/09 0600 NFIB Small Business Optimism: reported 100.8 vs. 100.3 prior (100.5 est)

- 09/09 1000 BLS Prelim Benchmark Revision to Est Survey Data (-818k, -700k)

- 09/09 1130 US Tsy $85B 6W bill auction

- 09/09 1300 US Tsy $58B 3Y Note auction (91282CNY3)

GBP: Sustainability of GBP Strength Rests on Fiscal Policy Mix

Sep-09 10:26

- Outside of JPY strength, GBP's gains today standout despite a lack of local drivers. The Gilt curve and, in particular, the longer-end has regained a sense of stability after being marked sharply higher into the end of August. How valid and long-lasting this market sustainability proves to be should determine GBP/USD's ability to correct back above 1.3595 and make meaningful headway toward the bull trigger of the July 1st high at 1.3789.

- While the initial cabinet reshuffle last week did little to shore up confidence headed into the Autumn Budget, there are some signs that - at least - the government are recognizing and looking to act on the economic challenges facing the UK. The appointment of economic advisers (including former BoE Deputy Governor Shafik) to No 10 suggests a renewed urgency on invigorating growth, and FT reports today that Chancellor Reeves is to tell ministers they must fight inflation, scrap the regulatory burden, resist public sector pay demands and back fiscal rules further bolster this view.

- Whether this economic focus changes to the outcomes of the UK Budget remains to be seen - but recognition that economic issues need addressing support the argument for conviction on November 26th. A fiscal policy mix that meets this requirement and placates back bencher preferences will, however, be a difficult task. As such, efforts to increase the efficiency of the state are likely to fall on cuts to the civil service, more restricted departmental budgets and regulatory reform - leaving welfare state spending a material issue in the medium-term.