CZECHIA: Babiš Cabinet Wins Confidence Vote

Jan-16 08:24

- Andrej Babiš's coalition government won a vote of confidence in the Chamber of Deputies after the longest-ever confidence debate lasting three days. All 108 MPs from the ruling coalition formed by ANO, SPD and the Motorists voted in favour of the motion, with 91 opposition MPs voting against.

- Babiš said that his coalition will not allow for his prosecution in the Stork's Nest case amid his concern that the judges could act on political motives. His remarks were then echoed by Chamber of Deputies Speaker Tomio Okamura.

- President Petr Pavel is in Kyiv and will meet with his local counterpart Volodymyr Zelensky and other senior officials. He told reporters that Ukraine welcomed new Czech PM's decision to continue the so-called ammunition initiative.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BTP TECHS: (H6) Recovery Extends

Dec-17 08:23

- RES 4: 121.33 High Oct 21 and a key resistance area

- RES 3: 121.37 High Nov 13

- RES 2: 121.24 High Nov 26

- RES 1: 120.34/77 Intraday high / High Dec 3

- PRICE: 120.28 @ 08:07 GMT Dec 17

- SUP 1: 119.54 Low Dec 12

- SUP 2: 119.13 Low Dec 10 and the bear trigger

- SUP 3: 118.00 Round number support

- SUP 4: 118.84 2.000 proj of the Nov 13 - 20 - 26 price swing

Gains in BTP futures appear corrective. However, the contract has traded above initial resistance at 120.17, the Nov 20 low. A continuation higher would signal scope for an extension towards 120.77, the Dec 3 high. On the downside, a reversal lower would refocus attention on key support at 119.13, the Dec 10 low and a bear trigger. Clearance of this level would confirm a resumption of the downtrend.

US TSY OPTIONS: TY Calls Lifted

Dec-17 08:22

Some upside exposure sought in recent trade:

- TYF6 113.50 calls paper paid 0-03 on ~4K over a few clips

- TYG6 114.00 calls paper paid 0-10 on 2.5K over a couple of clips

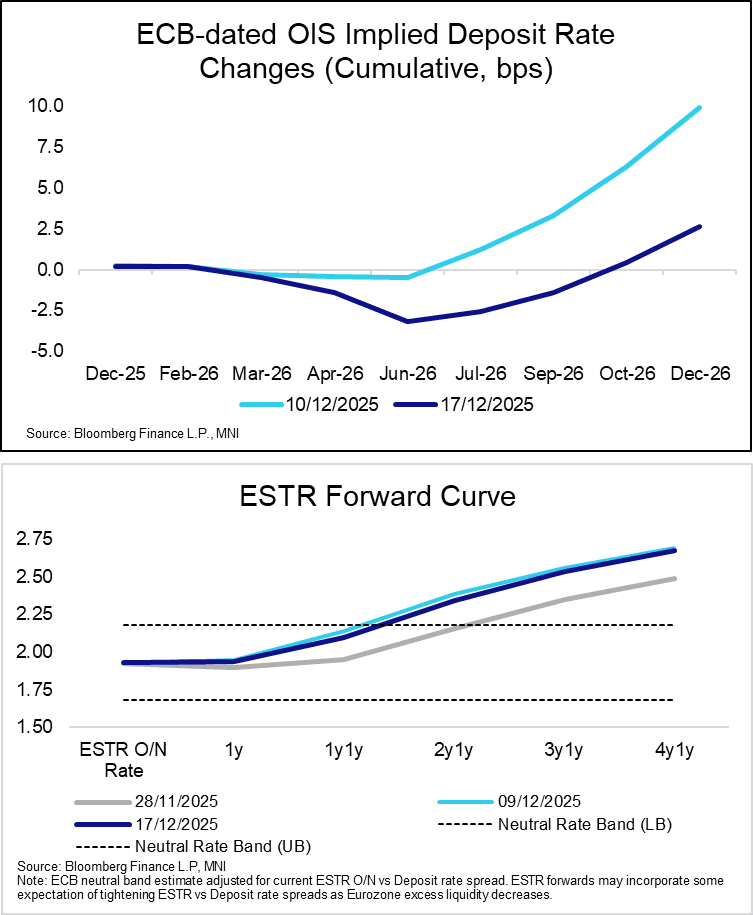

STIR: Risks To Tomorrow's ECB Decision More Balanced As Hawkish Repricing Fades

Dec-17 08:20

Risks to tomorrow’s ECB decision are becoming increasingly more balanced, with the EUR front-end fading a degree of recent hawkish repricing. ECB-dated OIS now price just 3bps of hikes the end of next year, down from an extreme of 10bps last Wednesday.

- Primary focus for tomorrow remains on the updated macroeconomic projections and the balance of risks to inflation and growth. Analysts expect upward revisions to both GDP and core HICP projections.

- We expect a repeat of a data-dependent and meeting-by-meeting approach, with no pre-determined path.

- MNI’s full ECB preview is here

- Markets still judge the next move in ECB rates to be a hike, with the ESTR 1y1y rate at 2.09% (versus an overnight rate of 1.93%). Improving regional growth momentum and the expected impulse from higher German fiscal spending have raised the bar to near-term cuts.

- Intraday, Euribor futures are +0.5 to +3.0 ticks through the blues, with dovish spillover from the softer-than-expected UK inflation report.