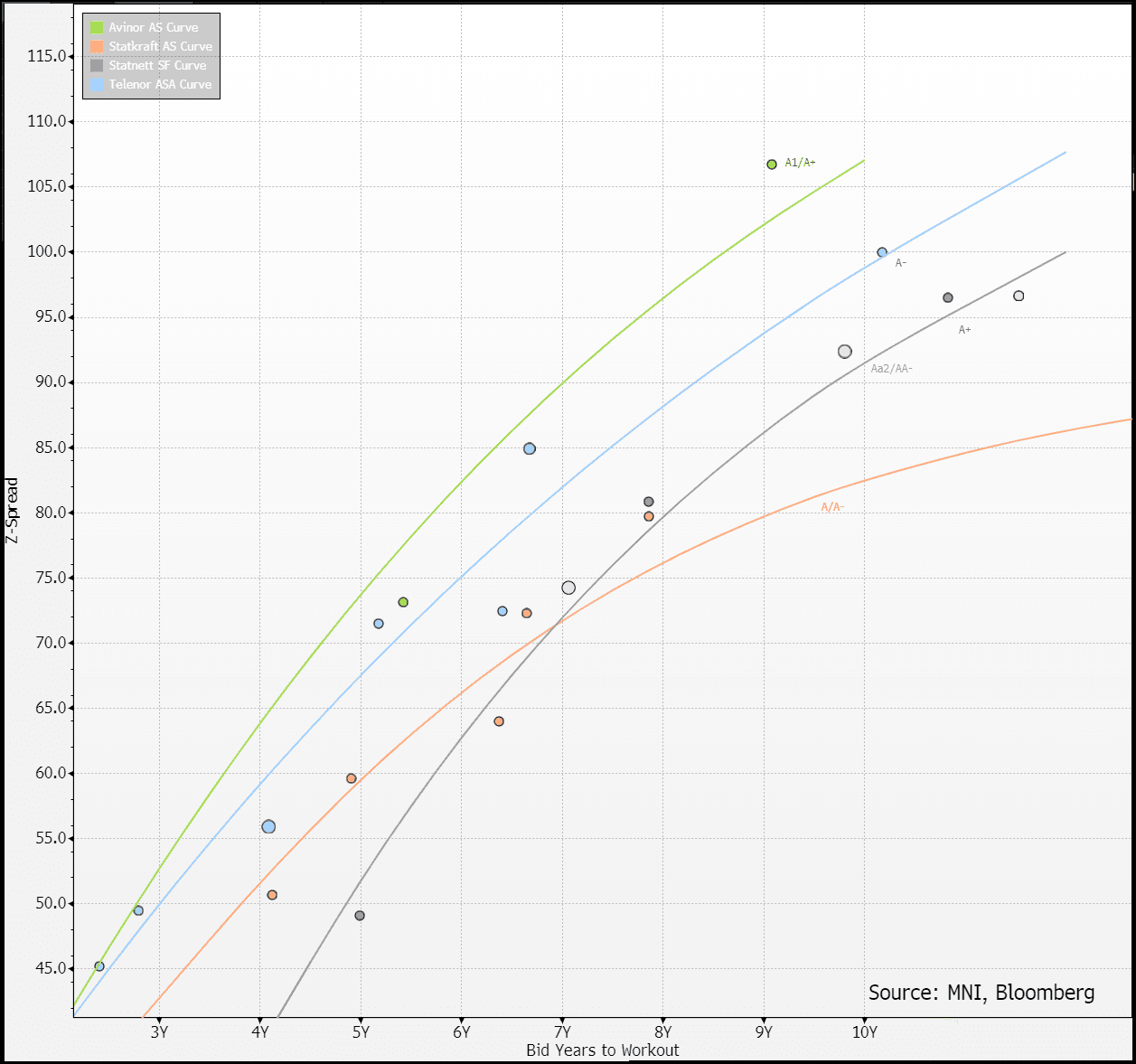

EU TRANSPORTATION: Avinor | RV

(AVINOR; A1/A+) (+4 uplift)

(Norway state owned; Aaa/AAA)

We see value on Avinor-34s well through the offer side (B+102/Z+103/3.4%)

We also see some value on the 30s.

€300m due this year (matured yesterday) - for which we would expect supply. 1Q earnings 26 May.

Avinor is our lowest beta pick among airports largely on full ownership from Norway Government.

FY24 results were fine. YTD passenger traffic running +4%.

Norway itself has the max AAA rating, spending is financed by substantial oil and gas revenues, runs fiscal and current account surplus and has the world's largest sovereign wealth fund (at ~€1.7T, over 3x GDP). I.e. very little rating risk.

Outside of screening value against airports and broader transport/consumer names, it also looks attractive against other Norwegian state owned/backed companies (below).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITIES: New Year-to-Date Lows for Jun-25 E-mini S&P Contract

Latest slippage in stock futures presses the e-mini S&P through the mid-March lows of 5559.75, making for fresh YTD lows for the June-25 future, making for a 10.9% drop off the December high.

- Price was lower in the March future (5509.25) ahead of expiry here - meaning the continuation chart is still off support for now. Tech and growth-sensitive names still quite clearly underperforming ahead of the open; the NASDAQ comp is off 1.6% vs. The e-mini S&P's 1.2% and the Dow's 0.6%.

- Magnificent Seven names are slipping pre-market: Tesla (-5.3%), Microsoft (-1.3%), NVIDIA (-4.0%), Meta Platforms (-2.3%), Apple (-0.6%), Amazon (-2.2%).

- Tariff concerns remain quite clearly the driver here, with markets still uncertain over the specifics and details of tariffs set to be unveiled on Wednesday's Liberation Day. Should convention for the previous phases of tariffs be followed, tariffs will come into effect at 0001ET/0501BST on Wednesday - leaving a tight timeline for the White House to provide further details.

GERMAN DATA: Retail Sales Stronger-Than-Expected in February, Outlook Mixed

German February retail sales volumes were notably stronger than expected as they increased 0.8% M/M (sa, cons 0.0) along with an upward revised 0.7% M/M in Jan (from 0.2%). It has seen retail sales start the year on a more robust note after a mixed Christmas last year, which included a heavy -1.0% M/M in December.

- It left sales up 4.9% Y/Y on a calendar-adjusted basis, admittedly driven by some strong increases in mid-2024, with recent moderation fading. Whilst the latest two months have clearly been strong, the 3M/3M metric stood at -0.2% non-annualised.

- Looking ahead, 3M/3M momentum should mechanically firm in March but there are signs of mixed trends. GfK consumer confidence for instance missed expectations last week and remained broadly unchanged despite its survey period at least partially being able to capture any shift in sentiment following the German fiscal announcement on March 4.

- Across categories, February's uptick appears broad-based, with food sales up 0.8% M/M, and non-food sales up 0.6% (both in real terms). Internet and mail orders meanwhile ticked up 1.0% M/M.

OUTLOOK: Price Signal Summary - Short-Term Bull Cycle In Bunds Remains Intact

- In the FI space, Bund futures have started the week on a bullish note, extending the recovery that started Mar 11. Recent gains are considered corrective, however, the breach of the 20-day EMA has exposed resistance at 129.41, the Jan 14 low (pierced). Clearance of this level would strengthen a bullish theme and open the 130.00 handle and 130.26, the 61.8% retracement of the Feb 28 - Mar 11 bear leg. Key short-term support to watch lies at 127.74, the Mar 25 low.

- The short-term trend outlook in Gilt futures remains bearish, however, today’s gap higher highlights a bullish start to this week’s trading session, and signals scope for a stronger recovery near-term. An extension would open 92.55, a trendline resistance drawn from the Mar 4 high. Clearance of this level would strengthen the short-term bull cycle. Key support and the bear trigger has been defined at 90.55, the Mar 27 low.