AUD: Aussie Recovering From Earlier Drop

AUDUSD dipped to 0.6640 earlier in the session, the lowest since before the RBA surprise hike this week, but it is now back at around 0.6692, 0.3% above the NY close. The USD index has continued moving down and is 0.3% lower following -0.7% yesterday.

- Aussie has recovered some ground against its crosses after dropping on the back of the sharp risk reversal earlier in APAC trading and is now up slightly on the day. AUDJPY is +0.1% to around 89.99 while AUDNZD is 1.0714. AUDEUR is +0.1% to 0.6038 and AUDGBP +0.1% to 0.5316.

- The Australian March trade balance widened to $15.27bn on the back of stronger commodity exports, particularly iron ore. See Trade Surplus Widens Further On Stronger Commodity Exports.

- Equity markets are mixed with the ASX down 0.2% but the Hang Seng up 1.1%. S&P e-minis are up slightly. Oil has climbed back to its NY close and WTI is trading around $68.63/bbl. Copper is up 1.5% and iron ore is around $104/t.

- Later the ECB meets and is expected to hike rates 25bp. In the US, there are Q1 unit labour costs, March trade and April Challenger job cuts data. On Friday, the RBA publishes its Statement on Monetary Policy which includes the full set of forecasts.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS AUCTION: PREVIEW: 10-Year JGB Supply Due

The Japanese MOF will today sell Y2.7tn of 10-Year JGBs, opening JB#370. The MOF last sold 10-Year debt on 2 March, the auction drew cover of 7.550x at an average yield of 0.500%, average price of 100.00, high yield of 0.500%, low price of 100.00, with 30.8365% of bids allotted at the high yield.

- Those looking to position for a steeper curve (e.g. via 10s vs. 20s, 30s or 40s), given the flattening seen YtD and the recent adjustments in BoJ Rinban purchase bands, may use this auction as a liquidity event for entry into a long 10s leg.

- Still, uncertainty re: BoJ policy in the months ahead may limit steepener strategies to a tactical horizon.

- Elsewhere, the allure of new paper will be a positive for demand, as will the assumed yield pickup vs. the current on-the-run 10s.

- March’s auction was particularly well received, as it acted as a liquidity event for short cover ahead of the latest BoJ decision. This means that the auction metrics seen last time out could skew perception re: the strength of impending auction.

- We also note that the events of the last few weeks have triggered a round of short cover in JGBs. A reduction in the short base is another negative for demand.

- All in, there should be enough baseline demand to generate smooth enough takedown, although the above variables muddy the outlook.

- Results due at 0435BST/1235JST.

RBNZ: MNI RBNZ Preview - April 2023: Another 25bp, Tightening Bias To Stay

- A step down to 25bp from February’s 50bp is widely expected at the April 5 meeting bringing the OCR to 5%, the highest since 2008. A pause and 50bp hike are also likely to be discussed.

- Given that another 25bp rise is expected, the guidance part of the accompanying statement will be particularly important to the outlook for monetary policy. It will probably acknowledge the very weak Q4 GDP data while reiterating that inflation remains too high and the labour market too tight. The RBNZ is likely to keep its options open while maintaining its tightening bias.

- Click to view full preview: MNI RBNZ Preview - April 2023

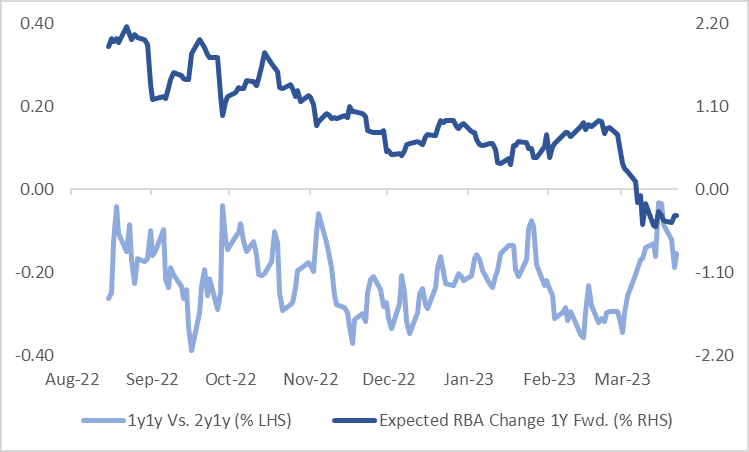

AUSSIE SWAPS: 1y1y Vs. 2y1y Steepener?

As highlighted previously, the recent flattening in 1-year swap Vs. 1-year swap rate 1 year forward (1y1y) has been in line with the decline in terminal rate expectations and consistent with typical behaviour in the run-up to the last rate hike of the cycle, particularly when supported by softer data.

- If the RBA pauses today one could expect 1y Vs. 1y1y to steepen into the release of Q1 CPI on 26 April and the RBA’s May meeting, if a favourable CPI print is forthcoming. Beyond that, history would suggest price action is somewhat volatile until there are clearer signs of an easing bias.

- Given the likelihood of volatility 1y Vs. 1y1y, a better play historically on RBA eventually shifting to an easing bias has been to position for a steeper 1y1y Vs. 2y1y. While it tends to offer less upside, it tends to be far less volatile.

- With the market pricing 23bp of easing by year-end, a better entry level for a 1y1y Vs. 2y1y steepener may present itself after today’s RBA decision if an explicit tightening bias is maintained.

Figure 1: Expected Cash Rate Change 1y Fwd. (%) & 1y1y Vs. 2y1y (%)

Source: Bloomberg / MNI - Market News