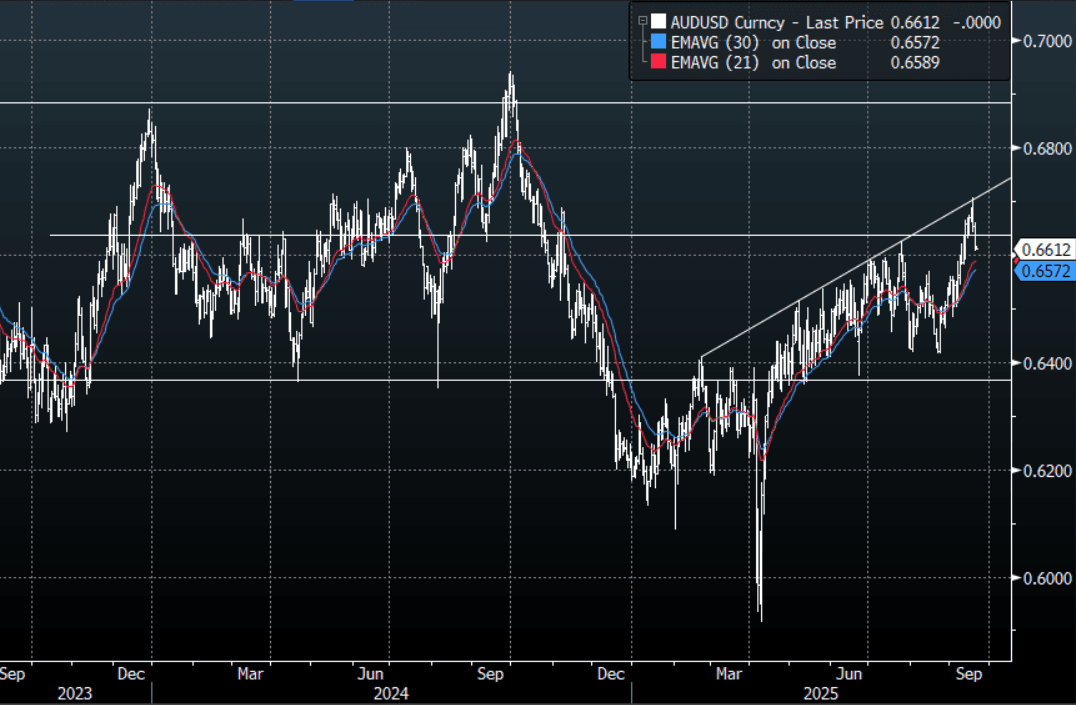

AUD: AUD/USD - Pulls Backs As The USD Gets Some Relief

The AUD/USD had a range overnight of 0.6607-0.6660, Asia is trading around 0.6610. US stocks did what they do best and made new highs as US yields bounced off their lows. This saw the USD get some welcome relief though time will tell how long the reprieve lasts. The AUD/USD should still see dips supported for now with the first buy-zone back towards the 0.6550 area.

- MNI POLICY: RBA Sees Risk That NAIRU Slightly Lower Than 4.5%. Internal analysis of recent economic data suggests the non-accelerating inflation rate of unemployment (NAIRU) may be 10-20 basis points below the Reserve Bank of Australia’s 4.5% estimate, which is based on model outputs likely distorted by the pandemic years, MNI understands. Former staffers have called on the RBA to revise its NAIRU estimate lower for some time.

- (Bloomberg) -- The Reserve Bank of Australia’s most trusted model of the neutral cash rate implies a “significant downward revision” to its estimates while the job market is seen as tighter than previously thought, according to internal documents released Thursday under a Freedom of Information Act request.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD857m), 0.6750(AUD1.17b). Upcoming Close Strikes : 0.6525(AUD705m Sept 22), 0.6650(AUD906m Sept 23), 0.6720(AUD791m Sept 24) - BBG

- CFTC Data last week shows Asset managers slightly increasing their shorts -68333(Last -66025), the Leveraged community pulled back the shorts they had just started to rebuild -5081(Last -11860).

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OIL: US Crude & Gasoline Stocks Fall Last Week

Bloomberg reported that there was a US crude inventory draw of 2.4mn barrels last week, more than offsetting last week’s 1.5mn build, but with only 100k at Cushing. Gasoline stocks fell 1mn barrels but distillate rose 500k, according to people familiar with the API data. The official data is out on Wednesday.

AUSSIE 3-YEAR TECHS: (U5) Holding Bulk of Rally

- RES 3: 97.190 - High May 5 2023

- RES 2: 96.932 - 76.4% of Mar-Nov ‘23 bear leg

- RES 1: 96.860 - High Apr 07

- PRICE: 96.580 @ 15:46 BST Aug 19

- SUP 1: 95.900 - Low Jan 14

- SUP 2: 95.760 - Low 14 Nov ‘24

- SUP 3: 95.480 - Low Jan 11 2023 and a major support

Aussie 3-yr futures gapped sharply higher on the back of the recent soft US NFP data, and last week’s CPI print should also prove supportive. Recent price action has narrowed the gap with resistance at 96.730, the Sep 17 ‘24 high, leaving 96.860 as the next key level. Any continuation lower would instead strengthen a bearish theme. This would refocus attention on 95.760, the 14 Nov ‘24 low. Conversely, a reversal higher would refocus attention on 96.860, the Apr 7 high.

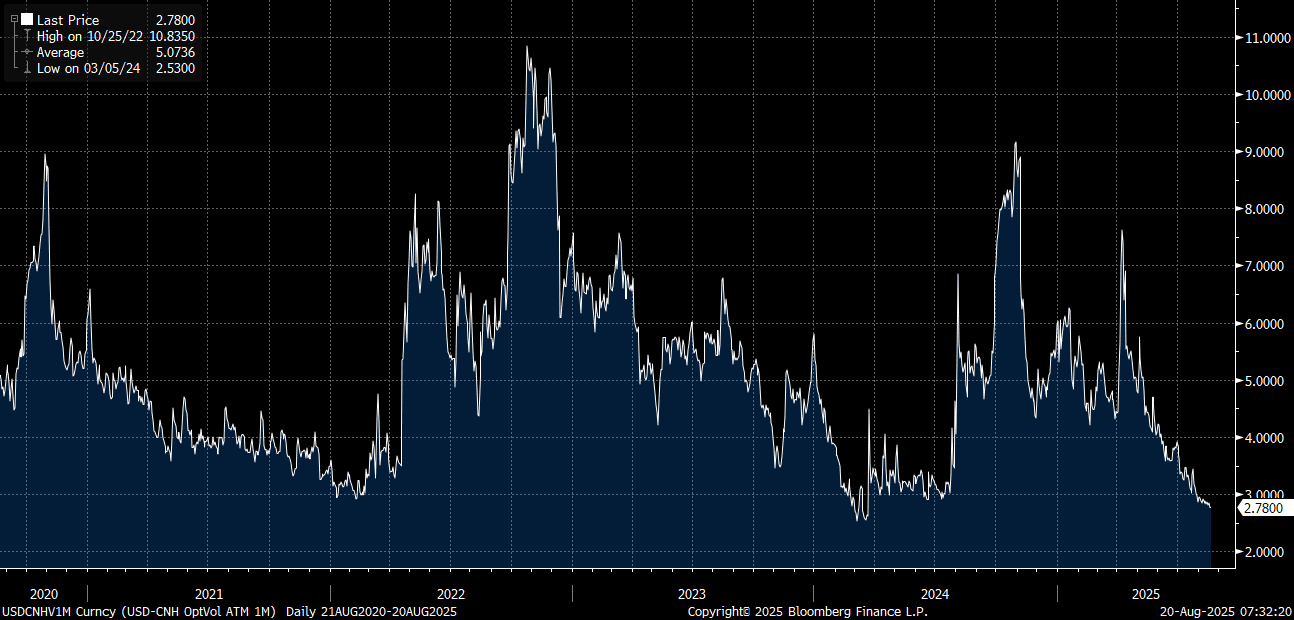

CNH: USD/CNH Implied Vols Continue To Decline, LPRs Seen Steady Today

Very low volatility persists for the yuan. USD/CNH sits near 7.1875 in early Wednesday dealings, after little movement in Tuesday's session. Broader USD indices were up for the session, albeit not at the same pace seen from Monday. Most of the USD gains were against higher beta FX, with weakness in US equities helping the move. Spot USD/CNY finished up at 7.1824, while the CNY CFETS basket tracker rose 0.13% to 96.20 (per BBG).

- Well worn ranges persist for USD/CNH as a catalyst for a range break remains absent. We sit close to the 20 and 50-day EMA points, while upside focus will rest with any retest above 7.2000. August lows at 7.1681 remain intact. 1 month implied USD/CNH vol is tracking towards 2024 lows, see the chart below.

- The Golden Dragon equity index fell 0.90% in US trade, but the China to global equity ratio sits close to late July highs, although this isn't providing much positive impetus to CNH at this stage.

- Via BBG: "Money managers are scaling back their bearish stance on China, adding technology and consumer stocks to their portfolios amid a four-month-long rally, according to an HSBC Holdings Plc survey." (see this link).

- US-CH government bond yield differentials remain within recent ranges. Note today we have the 1yr and 5yr loan prime rate decisions. No change is expected (1yr currently at 3.00%, 5yr at 3.50%), as these metrics have taken on less policy relevance over the past 12 months.

Fig 1: USD/CNH Implied 1 month Volatility

Source: Bloomberg Finance L.P./MNI