FOREX: AUD Only Moderately Corrects Lower Amid Broader Risk Selloff

Feb-12 17:35

- Sharp risk off sentiment has been on show across global markets Thursday, with pressure most notable across the equity, precious metal and crypto complexes. Despite this, major currencies have taken the developments in their stride, with the USD index holding close to unchanged levels on the session and EURUSD holding a very contained 38pip range.

- Most notable adjustments are being seen for AUD crosses, with the likes of AUDCHF and AUDJPY declining close to 1%, although the price action has had a sense of relative stability compared to other asset classes throughout the period of waning sentiment. Indeed, given the Australian dollar’s impressive performance across 2026 so far, the corrections are very moderate at this stage.

- Japanese yen volatility continues to be the most interesting aspect of the G10 currency markets this week, following the Japanese election on Sunday.

- Given the magnitude of the USDJPY move, it is perhaps unsurprising to see the pair generate some demand in the low 152’s, with the 3.5% decline in just four sessions falling just shy of 152.10 support, and the technical bear trigger. A solid turnaround from the 152.27 lows prompted a 153.76 session high over the NY crossover, however, spot has subsequently consolidated back below the 153 mark.

- If the price action following yesterday’s US employment report is anything to go by, the pair’s inability to consolidate any meaningful upward momentum could be a sign that further downside is imminent. The gap to the pre-October election lows is at 147.47

- Swiss Franc resilience has resumed today, with EURCHF seeing a renewed push back towards 0.91, narrowing the gap to Tuesday’s cycle lows at 0.9095. The overall bearish dollar narrative is also weighing notably on USDCHF, which edges closer to cycle lows, located 0.7605.

- Markets will await inflation data from both Switzerland and the US on Friday. Eurozone flash GDP data will also be released.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

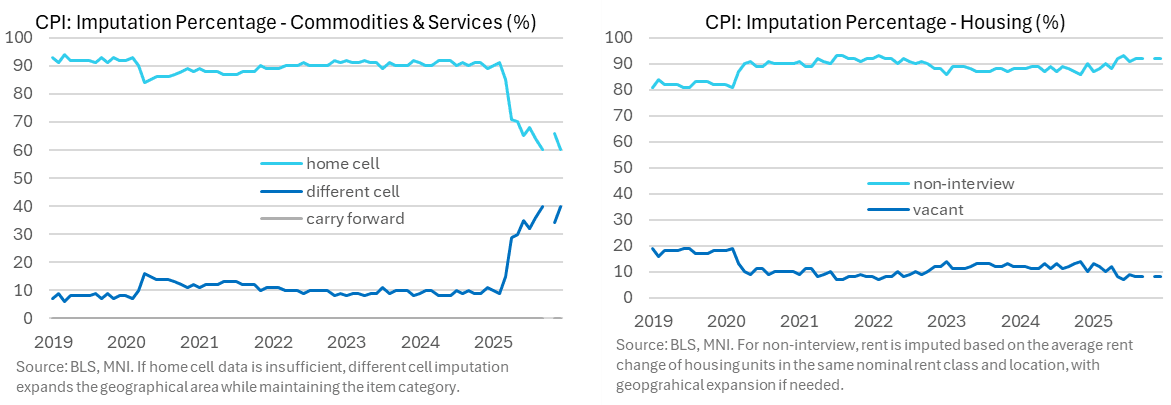

US DATA: CPI Imputation Shares Reverse Tentative Improvement Seen In November

Jan-13 17:24

- The December CPI report saw a reversal in the modest improvement in imputation shares seen with the November report relative to September for the commodities & services side of the report.

- Different cell imputation rose back to 40% after 34% in Nov for a joint record high with September in data going back to 2019. This is the share of the non-housing survey that had to widen the geographical area when it came to collecting each specific item.

- This share started the year at 10% before climbing following budget and staff cuts, whilst it previously peaked at 15% in the pandemic when in-person surveys weren’t possible.

- The housing survey imputation shares were similar to prior months meanwhile, with a 92% non-interview share of 92% after the same in both Nov and Sep. For these non-interview cases: “rent is imputed by the average change in rent observed for housing units within the same nominal rent class (low, medium, or high rent) within the same location. If this source pool is insufficient, the pool is expanded across geography similar to the method used in the C&S survey.”

US TSYS/SUPPLY: Preview 30Y Bond Auction Re-Open

Jan-13 17:22

Tsy futures remain firmer ahead of the $22B 30Y Bond auction re-open (912810UP1) at 1300ET. WI currently running around 4.836%, 6.3bp cheap to last month's sale. Today's results will be available shortly after the competitive auctions closes at 1300ET.

- December auction recap: Treasury futures hold near recent highs (USH6 +16 at 115-28) after the $22B 30Y auction re-open (912810UP1) near in-line: 4.773% high yield vs. 4.774% WI; bid-to-cover at 2.36x vs. 2.29x prior.

- Peripheral measures: indirect take-up receded to 65.38% vs. 71.0% prior; direct bidder take-up rose to 23.46% vs. 14.05% prior; primary dealer take-up 11.16% vs. 14.056% prior.

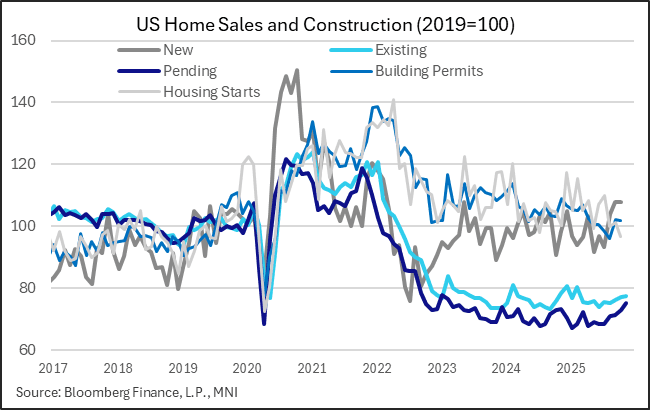

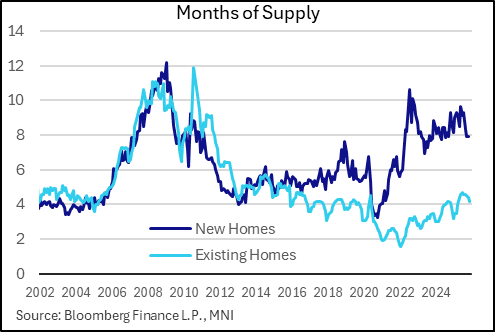

US DATA: New Home Sales Add To Evidence Of Thawing Housing Activity

Jan-13 17:09

New home sales looked strong and steady in a combined September/October report, with 738k/737k single-family home sales reported in those months marking the best back-to-back numbers since early 2022 (figures are in seasonally-adjusted, annual rate terms). That was better than the consensus expectation for sales to average 712k in those months.

- This provides another sign that the residential real estate market is thawing. Overall, existing sales are picking up, and with pending sales rising to a 33-month high in November, there are clearer signs of thawing in the residential sales market, with inventories tightening modestly.

- On the latter, the boom in new supply has faded and and sales have picked up: there were 488k homes for sale at the end of October, meaning 7.9 months of supply, vs 8.3 in August, 8.6 at the recent peak in May, and the lowest since September 2024.

- With mortgage rates dipping but still extremely elevated, price reductions appear to be part of the story in the sales pickup: median prices fell 8% Y/Y, and we know from homebuilders' surveys that discounting/incentives remain a key sales strategy.

- There was a substantial regional divergence: sales soared in the Midwest (+14% over the 2 months) and South (+15%) but plummeted in the West (-30%) and Northeast (-14%), with sales in the West the lowest since mid-2022 but South/Midwest the strongest since mid-2021.