FOREX: AUD Crosses - Claw Back Some Of The Unemployment Rate Losses

US stocks have powered once again to new all-time highs as US data continues to outperform. This morning has seen US futures open a little stronger as Waller talks up rate cuts, ESU5 +0.12%, NQU5 +0.10%. The AUD has bounced across the board as a result clawing back some of its losses in response to yesterday's weaker employment data.

- EUR/AUD - Overnight range 1.7857 - 1.7941, Asia is currently trading around 1.7865. The pair seems to be consolidating in a 1.7650 - 1.8050 range as the market awaits some clearer direction.

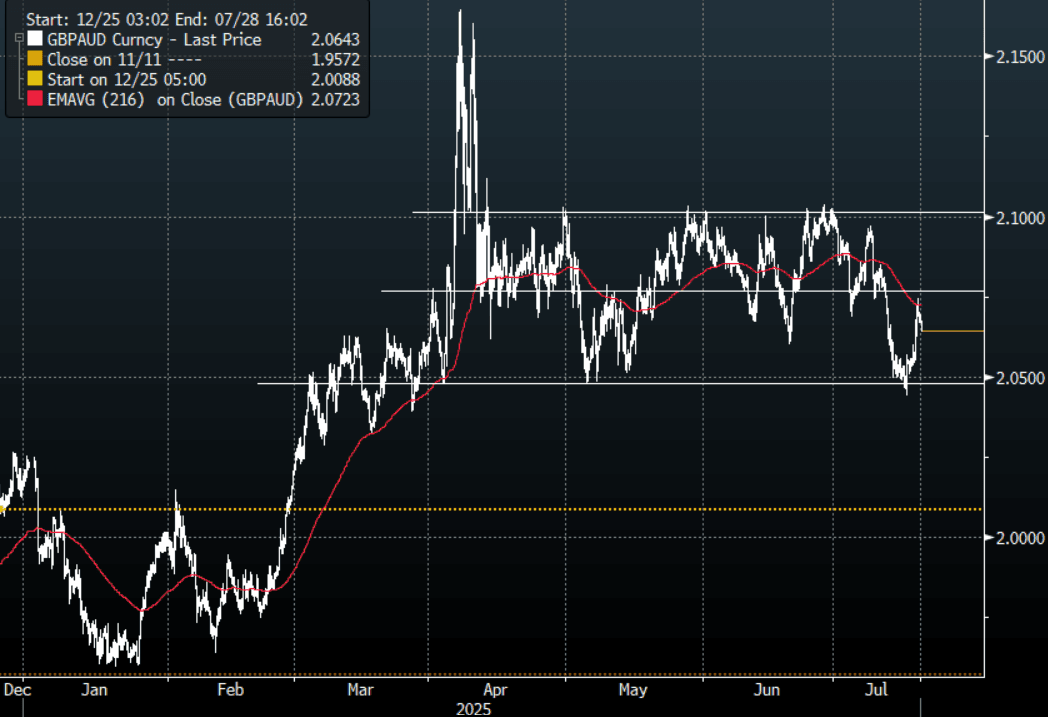

- GBP/AUD - Overnight range 2.0628 - 2.0746, Asia is trading around 2.0640. The bounced nicely off its support around 2.0500 and last night found some good supply in exactly the right spot as well drifting back off from the 2.0750 area. This pair is also now back within its wider 2.0450 - 2.1050 range with the 2.0750/2.0800 area acting as the pivot.

- AUD/JPY - Overnight range 96.00 - 96.50, Asia is trading around 96.60. The pair found good demand back towards the breakout area around 96.00, and this will need to hold to build a platform from which to probe higher again. The positive risk backdrop providing tailwinds.

- AUD/NZD - Overnight range 1.0922 - 1.0951, the cross is dealing in Asia around 1.0925. The cross moved lower in response to the AU Employment data. Dips back to 1.0850/1.0900 should still find support as the pair tries to build momentum to move higher.

Fig 1: GBP/AUD spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

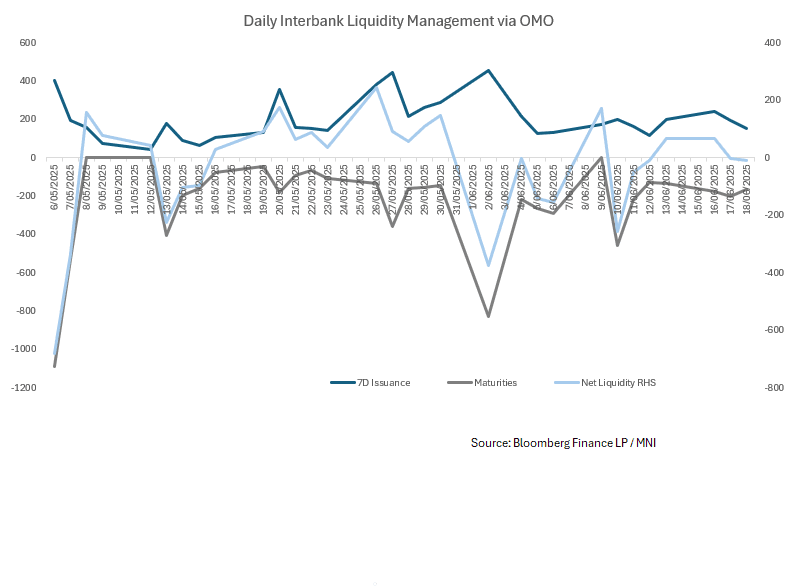

CHINA: Central Bank Withdraws CNY7.7bn via OMO

- The PBOC issued CNY156.3bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY164 bn

- Net liquidity withdrawal CNY7.7 bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.43%, from prior close of 1.52%.

- The China overnight interbank repo rate is at 1.36%, from the prior close of 1.38%.

- The China 7-day interbank repo rate is at 1.55%, from the prior close of 1.50%.

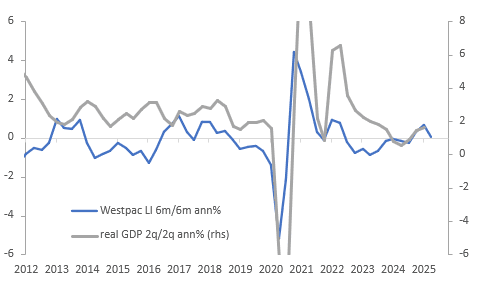

AUSTRALIA DATA: Westpac Lead Index Signals Slower Growth

The Westpac lead indicator fell 0.06% m/m in May after -0.01% but this resulted in the 6-month annualised rate falling to -0.08%, the weakest since September but importantly signalling that growth could ease to below trend over the second half of the year. The measure peaked in February and has been trending lower since as global uncertainty has risen and some domestic factors were also soft but Westpac believes these local “drags” are “temporary”.

- A disappointing recovery is likely to add to the argument for the RBA to ease policy further, especially if underlying inflation moves towards the 2.5% band mid-point. Westpac continues to expect the Board to be cautious given labour market tightness (May data print June 19) and be on hold on July 8 but then cut 25bp on August 12.

- The domestic economy appears to be struggling due to the end of public spending on some big projects but the private sector remains sluggish. Global uncertainty is also delaying investment decisions.

- A large share of the deterioration in the 6-month rate has been due to the stalling in the recovery of residential building approvals and the drop in hours worked, which hasn’t been helped by higher consumer inflation and unemployment expectations. Commodity and equity prices have also been a drag but to a lesser degree. However, US IP has added to the lead index.

Australia Westpac LI vs GDP growth

Source: MNI - Market News/LSEG

MNI: CHINA PBOC CONDUCTS CNY156.3 BLN VIA 7-DAY REVERSE REPO WEDS

- CHINA PBOC CONDUCTS CNY156.3 BLN VIA 7-DAY REVERSE REPO WEDS