FOREX: AUD & NZD Weakness Continues, Fresh Cycle Lows

AUD and NZD weakness has again been a feature of G10 FX trade today. Both pairs have made fresh cycle lows. The BBDXY index is little changed and is holding above 1289 at this stage.

- AUD/USD has fallen to 0.6310/15, fresh lows back to oct last year. We are off around 0.30% versus end Tuesday levels in NY. We had the Mid-Year Economic and Fiscal Outlook, the FY26 deficit has been revised up 0.1pp to 1.6% of GDP, FY27 0.4pp to 1.3% and FY28 0.2pp to 1.0%. This, along with soft growth expectations is a likely AUD negative.

- The metals backdrop is softer, with iron ore and copper weaker, continuing the recent softness in this space.

- Regional equity sentiment is mixed, China/HK markets are higher but this isn't helping the higher beta plays. For AUD/USD next support will be eyed at 0.6300.

- NZD/USD is back to 0.5740, off by the same amount as AUD. NZD/USD appears stuck in a falling wedge within a broader bearish trend, showing mixed signals with Monday’s morning star pattern followed by Tuesday’s bearish reversal. There isn't much support for the pair until 0.5600.

- USD/JPY has drifted lower this afternoon, last back around 153.40/45, little changed for the session. We are still above intra-session lows from Tuesday (153.16). EUR/USD has edged up slightly, last back above 1.0500.

- US yields have ticked down, losses a little beyond 1bps at this stage, which may helping EUR and JPY. US equity futures opened lower but are now modestly higher.

- Looking ahead, the Fed decision is announced and a 25bp rate cut is widely expected. There are also US November housing starts/building permits and Q3 current account data, as well as UK November CPI/PPI. The ECB’s Lane speaks.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: USD/JPY Volatile, But Little Net Change, Ueda Doesn't Give Dec Hike Hints

The BBDXY USD index is down modestly, but up from session lows. We were last near 1285, only off 0.05% versus Friday NY closing levels. Lows were near 1283 earlier, while we aren't too far away from session highs. Highs from last week in the index remain intact (around 1290).

- USD/JPY has seen the largest degree of volatility today, more than a 100pip range. Early bias, ahead of BoJ Governor Ueda's speech was lower, but we found support at 153.80/85 and rebounded to 155.14 as Ueda spoke. We sit back near 154.45 in latest dealings, only down a touch in yen terms for the session.

- The BoJ Governor spoke about further policy adjustments, if forecasts are realised, but didn't give a sense of urgency. This may mean a wait and see approach through the December meeting. The new year may provide more information around the 2025 wage outlook as well.

- US yields are down slightly at the front end of the curve, but not displaying sharp shifts. US equity futures are up after cash losses in Friday US trade

- AUD/USD is a touch higher, but has been range bound, last near 0.6465/70. It may be receiving modest support from higher commodity prices, with gold and iron ore up (the latter supported by firmer China steel production).

- NZD/USD is down a little, last near 0.5860. We had second tier data outcomes earlier, with the services PMI remaining in contraction territory.

- Later the Fed’s Goolsbee speaks and November NY Fed services and NAHB housing indices print. We also hear from the RBA's Kent. The ECB’s Lagarde, de Guindos, Lane and Buch also appear and euro area September trade data are out. BoE’s Greene speaks.

THAILAND: Private Spending Supported Despite Forecasts for Slowdown

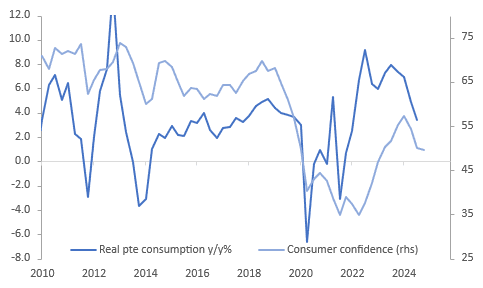

Q3 real private consumption slowed to 3.4% y/y from 4.9%, the lowest since Q1 2022. The NESDC is forecasting it to grow 4.8% this year, revised up 0.3pp, and then slow to 3.0% in 2025. This is despite the Digital Wallet Scheme which the government expects to boost growth significantly. Slowing consumption though has prompted it to meet on Tuesday to discuss further stimulus measures. Strength in other areas of the economy, including public spending and exports, is likely to keep the Bank of Thailand on hold in December.

- The first phase of the Digital Wallet Scheme started at the end of September and further payments are scheduled to be made through Q4. Currently the programme is worth THB 45bn or 0.25% of 2023 GDP and is expected to impact Q4 2024 and Q1 2025 spending. The government estimates it will increase GDP growth by 1.2-1.8pp, but many believe this is too high.

- Consumer confidence has been trending lower since it peaked in February but improved slightly in October rising to 56 from 55.3, below the average Q3 level, and the economic assessment to 49.6 from 48.8. The start of Q4 is suggesting that real consumption growth is likely to slow further.

Thailand real consumption y/y% vs consumer confidence

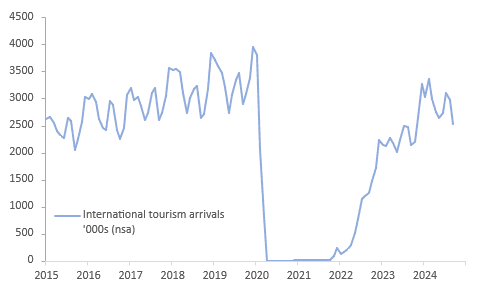

- Tourism is not only an important driver of services exports, which rose 21.9% y/y in Q3, but also private consumption. August/September are soft months but Q3 still grew 21% y/y on average.

- On the labour market front, employment growth is beginning to recover rising 1% y/y in September with private wage growth up 3.2% y/y and public +1.4% y/y.

Thailand tourist arrivals '000s

AUSSIE BONDS: Richer, Narrow Ranges, RBA Minutes Tomorrow

ACGBs (YM +5.0 & XM +3.0) are richer after dealing in narrow ranges in today’s data-light Sydney session.

- "Australia and other countries in the Asia-Pacific bloc must raise revenue and cut spending to ensure their budgets are prepared for the next global shock, and they need to embrace “ambitious” reform to lift growth and productivity, the International Monetary Fund says." (per AFR)

- "Goldman Sachs is urging investors to choose copper and aluminium over iron ore in 2025 as weak demand from China collides with an excess supply of Australia’s key export, keeping prices below $US100 a tonne." (per AFR)

- Cash US tsys are little changed across benchmarks in today’s Asia-Pac session after Friday’s bull-steepening.

- Cash ACGBs are 3-5bps richer with the AU-US 10-year yield differential at +17bps.

- Swap rates are 3-5bps lower, with the 3s10s curve steeper.

- The bills strip has bull-flattened, with pricing +1 to +6.

- RBA-dated OIS pricing is 1-6bps softer across meetings for 2025. No easing is priced by year-end, with a 25bp rate cut not fully priced until July.

- RBA Minutes for the November meeting are to be released tomorrow.