EU FINANCIALS: AT1 - 2025 Calls in EUR, USD, GBP

Dec-13 08:59

Around this time of year we look ahead at 2025…

…following a quick look back

We start with the AT1 market, which has had a truly exceptional year

YTD Performance

Bloomberg CoCo Eur Hedged : 14.4%

Bloomberg EUR banking subordinated index : 7.0%

Bloomberg EUR banking snr index : 5.8%

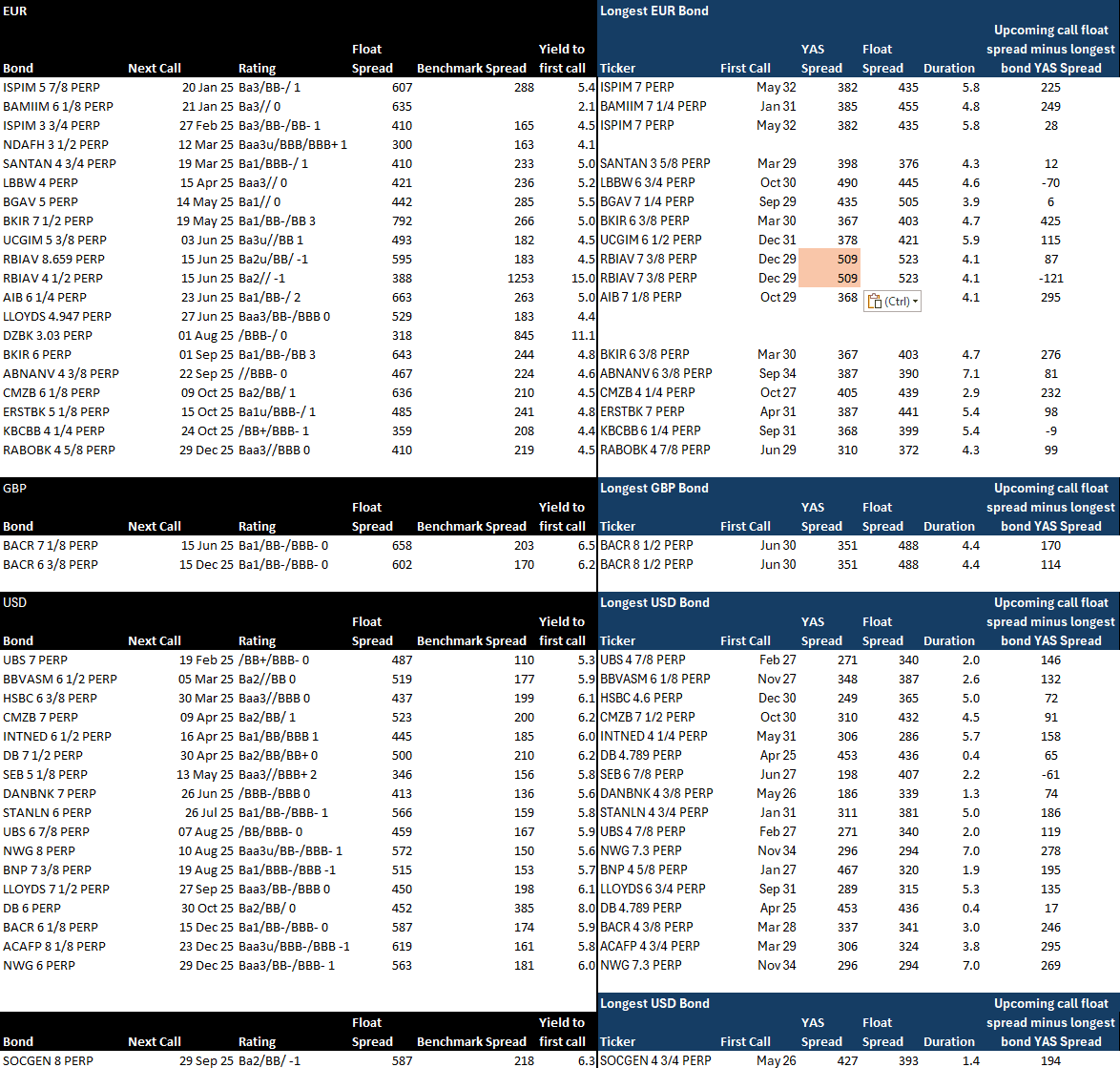

2025 Calls

- Below we look at the list of AT1's that become callable in 2025 in EUR (€9.6bn), GBP (£2bn) and USD ($23bn)

- Given where markets are priced, all but one of the names below ( DZBK 3.03% Perp ) are pricing to call

- Because of the spike in spreads in 2020 due to COVID, first calls in 2025 have relatively few bonds issued in 2020, and therefore issued under the PerpNC5 structure, which is the most common

- While calls in AT1's are supposed to be economic, we think, banks have shown a fair amount of wiggle room where issuers are often happy to call and reset floating spreads 50-100bps wider than they have been previously / i.e. higher than they would have paid if they didn’t call and let the bonds move to a floating rate

- If one were to just look at current benchmark spreads, most AT1's are pricing firmly to call - however, comparing float spreads to the highest spread outstanding AT1 bond by that issuer (and in that currency) is arguably a better proxy for refinancing risk. Especially if that bond was recently issued. For RBIAV we have used the most recently issued bond instead.

- In the very right hand column we subtract the longest bond YAS spread from the float spread of the bonds with upcoming calls - as a proxy for 'economic-ness' of call

- If we take for example the SANTAN 4.75% Perp with a first call on 19 Mar 2025. Its floating spread is 421bps, versus the SANTAN 3.625% perp trading at 402bps over. This implies rather little widening on the latter bond would be required to push the former bond into uneconomic call territory

- We can Juxtapose the SANTAN example with the BKIR 7.5% Perp , its float spread of 792bps is >400bps wider than its longer EUR AT1. The yield to call difference on the mentioned SANTAN and BKIR bonds is 0.1%.

- RBIA still trades with significant risk premium, but the new AT1

- Another thing, that likely won't surprise many, is just how tight US AT1's trade, when compared with the EUR counterparts, especially at the long end.

- GBP AT1 supply from refinancing should be limited next year

- Finally we would like to highlight the SOCGEN 8% Perp - it is a LIBOR exposed instrument and the fallback language within the documentation - based on our interpretation - notes that the coupon would reset to the initial coupon plus the floating spread - i.e. 13.87% if not called. Making a call overwhelmingly likely.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY OPTIONS: Large 10yr put spread

Nov-13 08:58

TYG5 108.50/107.50, bought for 20 in 19.2k.

JPY: USD/JPY Clears Tuesday High With Little Difficulty

Nov-13 08:56

USD/JPY has cleared yesterday's highs with little difficulty, putting price at the best levels since late July. US rates markets remain the key trigger here, with the 2yr US yield well within range of 4.4076%, the 200-dma.

- BoJ policy and the FX approach of the Japanese authorities becomes key here, with markets re-entering levels at which the Japanese authorities intervened in currency markets via JPY buying, however given the sharp gyrations in short-end US rates markets, it's unlikely recent price action meets the criteria for intervention - although comments from the Japanese finance minister last week upgraded their FX language: adding the word "extremely" to the phrasing "We are watching developments [...] with an extremely high sense of urgency".

- MNI's interview with former BoJ Chief Econ last week flagged that USD/JPY above Y155 and toward Y160 could prompt a rate hike at the December meeting, however a January hike is, for now, the more likely scenario.

- Levels of note on further strength include Y156.67, the 76.4% retracement for the downleg posted off the July high.

BONDS: CROSS ASSET: Tnotes and Bund are bouncing of the lows

Nov-13 08:51

- Bund and Tnotes are still finding better demand in early trades, volumes are still on the lower side, and moves are mostly order flow related as Investors await the US CPI later today.

- Resistance in Bund moves down to 132.33, followed by 132.73, did print a 132.74 high Yesterday.

- The small bounce in Tnotes is quite tiny overall, resistance moves down to 109.25+, followed by 110.04+.

- The move in Govies is helping the EURUSD off the low, and USDJPY of the high.