EU CONSUMER CYCLICALS: Consumer & Transport: Week in Review

Sep-26 15:01

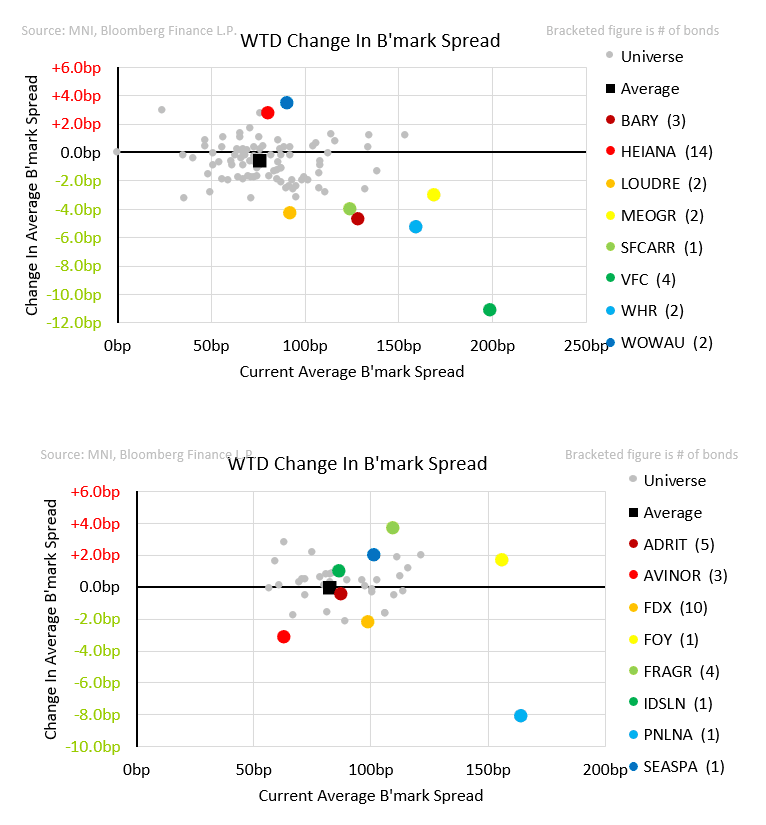

Index compression persisted with IG 2bps tighter and BBs -6bps. The real action was postal primary, where €1.7bn of BBB- step-protected bonds came with double-digit NICs. But in a change of theme, break performance to trade away the concessions hasn’t materialised for IDS. We will revisit the curve next week.

- Kering’s 30% stake in Valentino could be facing woes after it reportedly tripped debt covenants on “significant deterioration in 1H earnings” (bbg). We see limited read-through for Kering, where the credit story still hinges on fixing its own brand underperformance.

- PostNL refinanced its 2026 bond but with a 1.25% coupon step. The addition seemed to have helped - books went over 12x. But relative pricing vs. the 2031s still pointed to weak investor appreciation of the step. We flagged some asides on Kretinsky stake during pricing.

- IDS brought refinancing for Kretinsky takeover, again with 1.25% steps. While pricing suggested steps were partly reflected, secondary has since widened back (unch to +5bps vs. 13–23bp NICs).

- Heineken announced a €2.7b acquisition focused on beer and Pepsi bottling in Central America. Two days later it brough €2b/3-part supply that prices in-line with secondary. We saw no rating action on the +0.4x acquisition.

- Carrefour is rumoured to consider sale of Argentina (following rumours of Poland last week). We see it as a small, but performing, contributor to group earnings. The recently bought out Brazil operations were a much larger and strong performer.

- H&M reported firm 3Q results. Guidance for 4Q was more measured.

- Aeroporti di Roma was upgraded by Fitch to BBB flat, following Mundys’ move. Standalone remains A–.

- Rentokil was affirmed BBB flat by Fitch. Leverage sits at the top of tolerance but expected to trend lower on improving earnings.

- Primary (NIC in brackets): PostNL 5y (+20), IDS 4y (+13), 7y (+23), Heineken 3y (-2), 8.6y (+1), 12y (0)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ESM ISSUANCE: USD2bln WNG New 5-Year: Priced

Aug-27 14:58

- USD2bln WNG of the new 3.75% 5-year Sep-30 ESM-Bond

- Spread set earlier at SOFR MS+39 (SA 30/360) (guidance was SOFR+40 Area, IPT was MS+42 area, that was equiv. to CT5 + ~7.3bp)

- Books closed in excess of $13.3bn excl. JLM interest

- Reoffer 99.855 to yield 3.782%

- Issuer: European Stability Mechanism (TICKER: ESM)

- Issuer Ratings: Aaa (stable) (Moody's) / AAA (stable) (S&P) / AAA (stable) (Fitch)/ AAA (stable) (Scope)

- Format: Registered Notes, Reg S (NSS) / 144A

- Ranking: Senior, Unsecured, Unsubordinated

- Listing: Luxembourg

- Settlement: 4 September 2025 (T+6 (TARGET) / T+5 (NY))

- Maturity Date: 4 September 2030 (5Y)

- HR 101% vs CT5 (T 3 ⅞ 07/31/30 )

- ISIN: Reg S: XS3171756128 / 144A: US29881WAG78

- Coupon: 3.75%, Fixed, Semi-annual, 30/360, Following, Unadjusted

- Bookrunners: CACIB(DM/B&D) / DB / JPM

From market source and Bloomberg.

The transaction comes ahead of a USD3bln redemption for the ESM in September. That line also had a 5-year maturity initially.

STIR: BLOCK: SOFR White Pack

Aug-27 14:41

- 4,000 SOFR White packs (SFRU5-SFRM6) +0.000 at 1037:12ET - likely swap-tied sale with spds running wider in the short end

FED: September Rate Cut Base Case For Most, Though Some Holdouts Remain (2/2)

Aug-27 14:39

Elsewhere, multiple analysts now see a cut in September whereas previously they'd seen one later in 2025.

- Deutsche pulled forward their next-cut call from December to September (but still see a December cut).

- Barclays also pulled forward their view for the next cut to September.

- Natixis appears to have shifted its view for the next cut in October to be pulled to September "from this early juncture we think a September hawkish ease is more likely than not (assuming a 25bp cut), but there is still a great deal of time, and data, between now and the September FOMC meeting".

- SocGen likewise ("Previously, our base case was just one 25bp cut, and late this year (October or December). However, a rate cut at the next FOMC in September now looks an above 50% probability.")

- RBC isn't yet convinced of a cut before December: "While the odds of a rate cut next month are high, we aren’t yet convinced it is a slam dunk."