NZD: Asia Wrap - NZD/USD Bounces On a Better Employment Print & Positive Risk

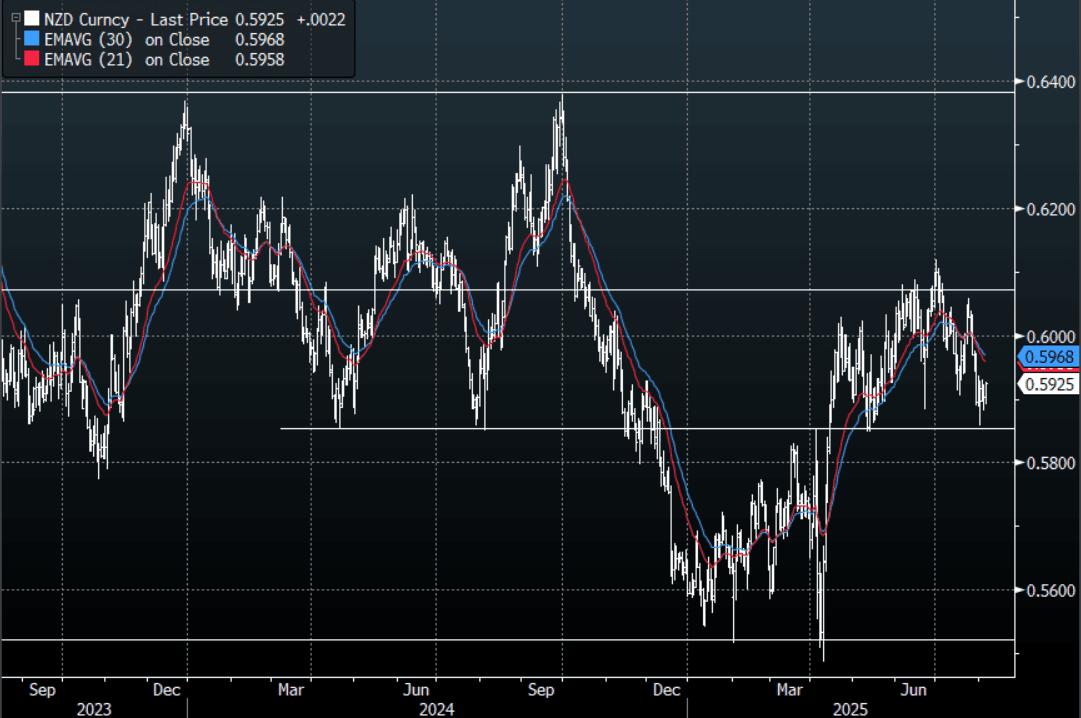

The NZD/USD had a range of 0.5891 - 0.5926 in the Asia-Pac session, going into the London open trading around 0.5925, +0.37%. The NZD has bounced in our session in response to a better than expected unemployment print and Asian equities trading positively ignoring the wobble seen in the US in response to the ISM Services data. NZD/USD bounced nicely off its 0.5850 support but I would suspect sellers could return on any bounce back toward 0.6000. With the seasonality for risk looking poor there is a chance it tests the pivotal 0.5800/50 area, a break of which would open up a move back to the 0.5500 lows.

- NEW ZEALAND: Q2 Sees Increased Labour Market Capacity. NZ employment was weaker in Q2 than the RBNZ projected in May declining 0.1% q/q and 0.9% y/y, in line with consensus, after a downwardly-revised 0.0% q/q & -0.7% y/y in Q1. The unemployment rate rose 0.1pp to 5.2%, highest since Covid-impacted Q3 2020, but as the RBNZ forecast. The next rate decision is on August 20 and will include an updated outlook. With job shedding continuing and activity indicators remaining lacklustre and inflation in the band, another 25bp rate cut is likely.

- “NZ FINANCE MINISTER WILLIS: EXPECT UNEMPLOYMENT TO FALL LATER THIS YEAR, EXPECT EXPORTS TO CONTINUE TO BOOM. INCREASED US TARIFF RATE ON NZ WON'T HAVE BIG IMPACT" - BBG

- Kelly Eckhold(Westpac NZ) on LinkedIn: “Today's labour market reports came in a touch stronger than our forecasts but more or less in line with the RBNZ's thinking. The Unemployment rate rise to 5.2% instead of our 5.3% forecast. While jobs growth remains weak, the under 20's are moving out of the workforce and heading into training. The NEET rate was unchanged this quarter in seasonally adjusted terms. I think this is a return to normality for this younger cohort and bodes well for their future.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5970(NZD496m Aug 7), 0.5920(NZD483m Aug 11), 0.5930(NZD646m Aug 11). - BBG

AUD/NZD range for the session has been 1.0949 - 1.0982, currently trading 1.0955. The Cross moved lower in response to the better employment print but continues to consolidate on a 1.09 handle as the pair tries to build some momentum to move higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

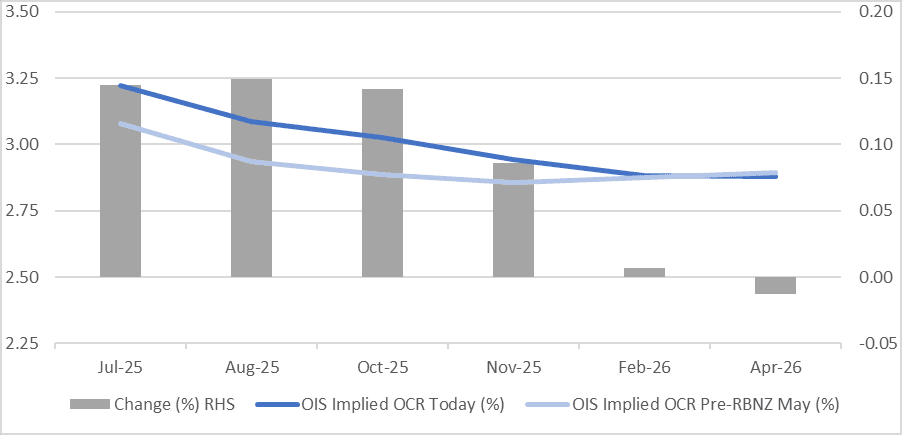

STIR: RBNZ-Dated OIS Firmer Than Pre-RBNZ Decision Levels (May)

RBNZ dated OIS pricing is little changed across meetings today. 3bps of easing is priced for this week's meeting, with a cumulative 31bps by November 2025.

- Notably, pricing is 9-15bps firmer across 2025 meetings compared to pre-RBNZ decision levels on May 28.

- (Bloomberg) -- A majority of members in the NZIER Monetary Policy Shadow Board recommend that the Reserve Bank of New Zealand keep the cash rate on hold at 3.25% at the July 9 review. While activity remains soft in the New Zealand economy, there are both upside and downside risks to inflation in the near term, given the recent pick-up in annual CPI inflation and heightened global risks.

Figure 1: RBNZ Dated OIS Today vs. Pre-May RBNZ Decision Levels (%)

Source: MNI - Market News / Bloomberg

CHINA: Bond Futures Drift Lower in the Morning Session

- China's bond futures have drifted marginally lower in a lackluster trading session this morning despite a sizeable liquidity withdrawal from the OMO.

- The 10yr is down -0.01 to 109.10 to maintain its position above all major moving averages. The nearest being the 20-day EMA of 109.02

- The 2yr is down -0.01 at 102.50 and is between the 50-day EMA of 102.50 and the 20-day EMA of 102.49

- The CGB 10yr is at 1.64%.

- Wednesday sees the release of June PPI and CPI, which have both struggled to post positive outcomes in recent months.

RBA: MNI RBA Preview-July 2025: 25bps Cut Likely

- The RBA is widely expected to cut by 25bps at tomorrow’s policy meeting. This is the sell-side consensus, albeit with a small number of economists expecting rates to be left on hold. Financial market pricing is also consistent with a 25bps cut. Our bias is also for a 25bps cut, which would take the RBA cash rate to 3.60% (still above neutral rates). If realized this would be 75bps worth of easing delivered so far in this cycle.

- Data towards the end of June, for May monthly CPI, should give the RBA confidence to cut. Headline inflation was close to the bottom end of the RBA’s 2-3% target band, whilst the trimmed mean eased to 2.4%y/y. Services inflation is still running at a stronger pace, but we continue to move off recent highs for this sub-sector of inflation.

- Some focus will be on the language the RBA uses and whether it considers a 50bps cut or not (assuming a 25bps cut is delivered). We feel the most likely scenario for the RBA board will be to consider holding steady or a 25bps cut. International risks are now arguably lower compared to the first part of Q2. This outlook can change quite quickly, but at the current juncture there are likely to be less fears around the global outlook.

- See this link for the full preview.