ASIA STOCKS: Asian Equities Saw Strong Inflows Thursday

Sep-12 23:22

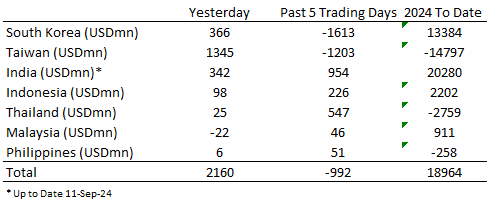

There were strong inflows into recently heavily sold Asian tech stocks on Thursday with Taiwan seeing the largest inflow since Mid August. We also the largest outflow in a month for Malaysian equities on Wednesday.

- South Korea: Saw $366m of inflows yesterday, with the past 5 sessions totaling -$1.61b, while YTD stands at +$13.38b. The 5-day average is -$323m, below both the 20-day average of -$184m and the 100-day average of - $9m.

- Taiwan: Saw $1.35b of inflows yesterday, with the past 5 sessions reaching -$1.20b, while YTD is -$14.80b. The 5-day average is -$241m, below the 20-day average of -$253m and the 100-day average of -$131m.

- India: Saw inflows of $342m Wednesday, with the past 5 sessions now totaling +$954m, while YTD is +$20.28b. The 5-day average is +$265m, below the 20-day average of +$304m but above the 100-day average of +$64m.

- Indonesia: Saw inflows of $98m yesterday, with the past 5 sessions netting +$226m, while YTD flows are +$2.20b. The 5-day average is +$45m, below the 20-day average of +$96m but above the 100-day average of +$13m.

- Thailand: Saw inflows of $25m yesterday, with the past 5 sessions now totaling +$547m, while YTD flows are -$2.76b. The 5-day average is +$109m, significantly above the 20-day average of +$28m and the 100-day average of -$11m.

- Malaysia: Saw outflows of $22m yesterday, with the past 5 sessions netting +$46m, while YTD flows are +$911m. The 5-day average is +$9m, below the 20-day average of +$47m but above the 100-day average of +$15m.

- Philippines: Saw inflows of $6m yesterday, with the past 5 sessions totaling +$51m, while YTD flows are -$258m. The 5-day average is +$10m, slightly below the 20-day average of +$12m but above the 100-day average of -$3m.

Table 1: EM Asia Equity Flows

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Richer With US Tsys After Benign US PPI Data

Aug-13 23:17

ACGBs (YM +4.0 & XM +4.0) are richer after US tsys rallied strongly on lower-than-expected PPI data. The front end paced the gains in a bull-steepener, with the 2-year yield declining 9bps to 3.93%, the lowest since last Monday. The 10-year yield fell 6bps to 3.84%.

- PPI final demand was softer than expected in July at 0.10% m/m (cons 0.2%). Within the components that feed into PCE calculations, hospital inpatient services offer the greatest moderation on the month as inflation slowed from 0.41% to 0.16% m/m. It was however partly offset by portfolio management fees rising 2.3% m/m after 0.6% in June.

- Fed Bostic said interest rates will fall by the end of the year if the economy performs as he expects.

- US CPI is due for release later today. (See MNI CPI Preview here)

- Cash ACGBs are 4bps richer, with the AU-US 10-year yield differential at +12bps.

- Swap rates are 4-5bps lower.

- The bills strip has bull-flattened, with pricing flat to +5.

- RBA-dated OIS pricing is 3-6bps softer for 2025 meetings. A cumulative 22bps of easing is priced by year-end.

- Today, the local calendar is empty apart from the AOFM’s planned sale of A$800mn of the 3.50% 21 December 2034 bond.

- The RBNZ Policy Meeting is today.

BONDS: NZGBS: Little Changed Ahead Of RBNZ Policy Decision, US Tsys Rally On PPI Data

Aug-13 22:56

In local morning trade, NZGBs are slightly richer ahead of today’s RBNZ Policy Decision.

- Overnight, US tsys finished richer, with the 2-year yield 9bps lower and the 10-year down 6bps, after a benign PPI print.

- PPI final demand was softer than expected in July at 0.10% m/m (cons 0.2%). It came with a net upward revision of 0.09pps but that was mainly in March and May, whilst June was revised down from 0.22% to 0.18%.

- We expect the RBNZ to discuss a rate cut at the today's meeting but opt to keep monetary policy unchanged. Nevertheless, we expect the bank to communicate its intention to ease before year-end through its statement, press conference and updated staff forecasts. It is a close call today with 9 of 23 forecasters on Bloomberg expecting a cut. See here for the full preview.

- Swap rates closed 2bps lower.

- RBNZ dated OIS pricing is little changed across meetings today. The market attaches a 58% chance of a 25bp cut today versus 69% on Friday and 43% before RBNZ inflation expectations data last week. A cumulative 47bps of easing is priced for the October meeting, with 87bps of cuts by year-end.

US TSYS: Tsys Futures Rally On Soft PPI Data, CPI Later Today

Aug-13 22:46

- Treasury futures closed at session highs, after initial trading higher on lower-than-expected PPI data with final demand was softer than expected in July at 0.10% M/M (cons 0.2). It’s after a net upward revision of 0.09pps but that was mainly in Mar and May, whilst June was revised down from 0.22% to 0.18%.

- Middle East tension continued to lend to safe haven support for rates, although stocks ignored risks and have traded back to early August levels.

- TUU4 was + 04⅜ at 103-12¾, while TYU4 was + 13+ at 113-21 we still sit comfortably below initial resistance of 114-03 (Aug 6 highs), while support rests at 112-15 (20-day EMA)

- A bullish theme in Treasuries remains intact following recent gains. Moving average studies are in a bull-mode position and the recent breach of 111-01, the Jun 14 high, confirmed a resumption of the uptrend

- Cash treasury curves bull-steepened, with yields falling 4-9bps. The 2yr yields was -8.8bps to 3.929%, while the 10yr yield was -6.1bps at 3.843% with the 2s10s +2.499 to -9.0810.

- MNI US CPI Preview: Large Miss Needed For Fed To Guide 50bp Cuts - (See link)

- The Fed's Bostic stated he's waiting for more data before supporting interest rate cuts, emphasizing the need for certainty to avoid reversing course. He remains optimistic about cutting rates by year-end, despite concerns over rising unemployment and recent labor market data.

- Focus will be all on CPI data later today while we also have MBA Mortgage Applications & $75B 42D CMB Tsy bill auction.