AUSSIE BONDS: AOFM Weekly Issuance Slate

The AOFM has released its weekly issuance slate:

- On Monday 6 March it plans to sell A$500mn of the 0.50% 21 September 2026 Bond.

- On Wednesday 8 March it plans to sell A$500mn of the 2.75% 21 June 2035 Bond.

- On Thursday 9 March it plans to sell A$1.0bn of the 26 May 2023 Note, A$1.0bn of the 21 July 2023 Note & A$1.0bn of the 8 September 2023 Note.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

RBA: Inflation Likely Peaked At End 2022 At Around 8%

RBA’s Kohler, Head of Economic Analysis, appeared before the Senate Select Committee on the Cost of Living. It is worth noting that she was limited in her answers given that the RBA is currently reviewing its forecasts which will be published on February 10 in the Statement on Monetary Policy. She said that the central bank thinks that inflation peaked at the end of last year at around 8%.

- Kohler reiterated that “inflation is too high” and price pressures have broadened to domestic areas. She also noted that Australia is lagging other countries due to the later reopening and had some Australia-specific problems, such as floods and domestic energy markets. Kohler commented that higher rates were necessary to bring supply and demand into balance and inflation down.

- She noted that the labour market remains very tight and are putting upward pressure on wages but that real wages have been falling. More employment income has helped through more jobs and increased hours and higher rates have increased the incomes of self-funded retirees.

- Kohler’s opening remarks can be read here.

- Woolworths spoke after Kohlerand the supermarket chain believes that the worst of inflation is over as key global food and shipping costs have eased. But suppliers continue to say that costs and staff shortages are a constraint.

AUSSIE BONDS: Twist Steepening Creeps In

ACGBs have twist steepened at the margin, with the major benchmarks sitting 1bp richer to 1bp cheaper, as the space shakes off any trans-Tasman impetus in the wake of the Q4 labour market data out of NZ. YM sits +1.5, while XM is flat. EFPs are essentially unchanged. Bills run flat to +3 through the reds, with the strip steeper at the margin. Very near-term RBA dated OIS is little changed on the day, with 23bp of tightening showing for next week’s meeting. Macro headline flow remains modest, with focus on Chinese Caixin manufacturing PMI data and the latest Fed monetary policy decision noted.

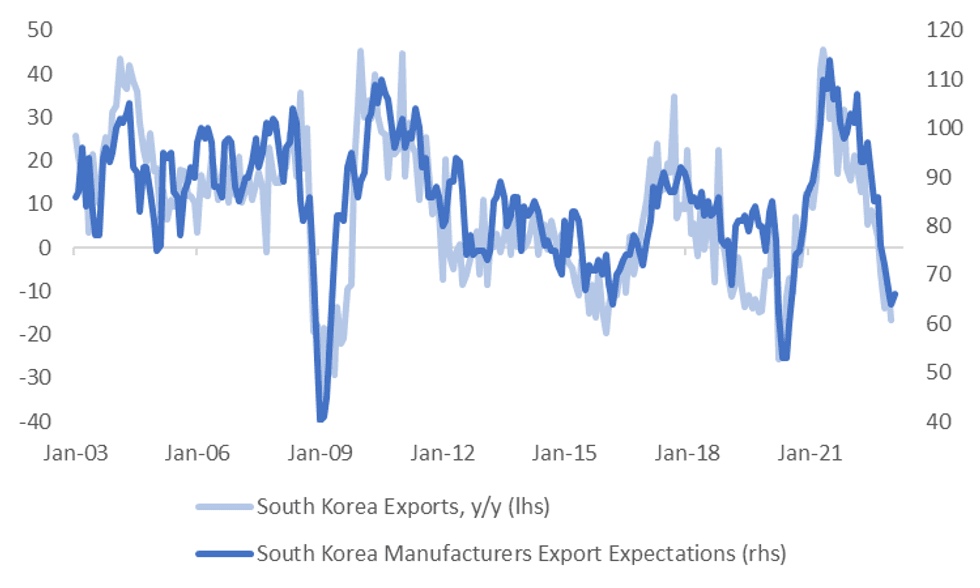

SOUTH KOREA: Trade Figures Disappoint, Recovery Likely To Be Gradual

January trade figures were disappointing, with export growth coming in at -16.6% y/y (-11.1% forecast, -9.6% prior), while imports printed as expected -2.6% y/y (prior -2.5%). The trade deficit ballooned out to -$12.69bn, versus -$9.27bn expected and -$4.69bn prior.

- Export growth continues to trend lower, now at levels last seen in early 2020 (we troughed around -26% in April 2020).

- There is some hope of improved conditions going forward, the first chart below overlays export growth against export expectations from South Korean manufacturers (sourced from the BoK).

- The most recent survey showed a slight uptick after a sharp downturn through the latter stages of 2023. We remain at depressed levels though and while China's exit from CZS should aid demand, the recovery is not expected to be V shaped.

- The consensus looks for real export growth to be back at 3.0% y/y by end of this year (we were at -4.4% in Q4 of last year).

Fig 1: South Korean Exports Versus Manufacturers' Expectations

Source: MNI - Market News/Bloomberg/BoK

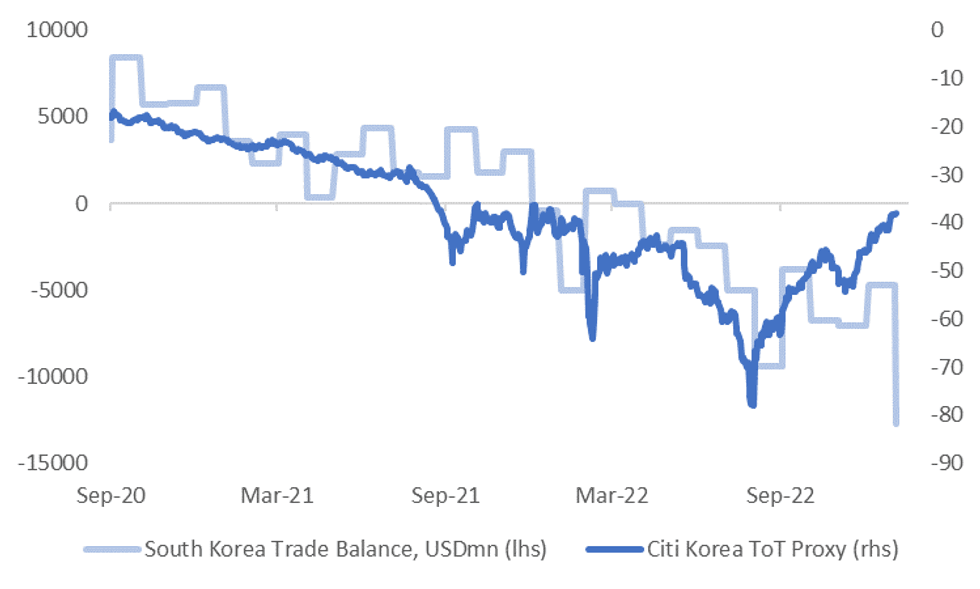

- The relationship between the trade deficit and the Citi South Korean terms of trade (ToT) proxy has weakened, see the second chart below. The trade deficit hit a fresh record wide near -$12.7bn in January. The authorities cited weakness in chip prices and still elevated energy costs as drivers of this result.

Fig 2: South Korea Trade Deficit Hits Fresh Wides Despite Citi ToT Proxy Improving

Source: Citi/MNI - Market News/Bloomberg