US TSYS/SUPPLY: Analysts Eye Distant Upsizings, Bill Sales To Rise (3/3)

Analysts' outlooks for Wednesday's refunding reflect almost no expectations for any major changes, but there is increasing attention being paid to the likelihood of increased bill issuance ahead as coupon sizes aren't increased until well into 2026 at least. Some selected views in alphabetical order of institution:

- Citi: Next coupon upsizing in Nov 2026 “but there is a growing risk that Treasury can avoid increasing coupons until 2027”. "“Treasury has not given strong guidance on the ‘optimal’ T-bill level, but we think there is scope for this to increase to 25%.”

- Danske: Next upsizing in 1H 2026. "“the Treasury could align with the TBAC recommendation that T-Bills should constitute 20% of net issuance. This would require increasing the size of coupon auctions by approximately USD250bn per year starting in FY26.”

- Deutsche: Next upsizing in August 2026 "with larger adjustments in the 2Y to 5Y sector". When coupons are eventually upsized, “increases would extend over many quarters, keeping net coupon issuance at around 75% of projected borrowing and stabilizing the bill share of total debt around 25% over the longer run.”

- Jefferies: Next upsizing not until after FY 2026.

- Morgan Stanley: Next upsizing in February 2027.

- NatWest: No changes to nominal coupon sizes in 2026, risks leaning to even further delays.

- TD Securities: Next upsizing in Nov 2026. Notes re this week's refunding “we see a risk that the Treasury market reacts positively if Treasury spends a significant amount of time focused on the Fed's balance sheet runoff ending and the resumption of reserve management purchases next year. This could hint to investors that Treasury intends to delay auction size increases (which we expect to occur late next year) or even decrease long-end auction sizes to help bring yields lower.”

- Wells Fargo: Next upsizing in early 2027. “There are some risks of additional federal budget deficit widening next year if the Supreme Court strikes down the President's IEEPA authority for imposing tariffs, but the end of quantitative tightening and the eventual resumption of balance sheet growth by the Federal Reserve should help soak up a big chunk of the bill supply that's coming in the year ahead.”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Fresh Cycle High

- RES 4: 1.4111 High Apr 10

- RES 3: 1.4045 3.0% Upper Bollinger Band

- RES 2: 1.4019 38.2% retracement of the Feb 3 - Jun 16 bear leg

- RES 1: 1.3989 200-dma

- PRICE: 1.3953 @ 16:02 BST Oct 3

- SUP 1: 1.3897/3825 Low Sep 30 / 50-day EMA

- SUP 2: 1.3727 Low Aug 29 and a bear trigger

- SUP 3: 1.3689 Low Jul 28

- SUP 4: 1.3637 Low Jul 25

A bull cycle in USDCAD remains intact and yesterday’s break above the late September’s high, firms the bullish theme. This move higher also maintains the bullish price sequence of higher highs and higher lows. Note too that moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on 1.4019, a Fibonacci retracement point. On the downside, first key support lies at 1.3825, the 50-day EMA.

AUDUSD TECHS: Support Remains Intact For Now

- RES 4: 0.6763 1.382 proj of the Jun 23 - Jul 24 - Aug 21 price swing

- RES 3: 0.6726 1.236 proj of the Jun 23 - Jul 24 - Aug 21 price swing

- RES 2: 0.6660/6707 High Sep 18 / 17 and key resistance

- RES 1: 0.6629 High Sep 30 & Oct 01

- PRICE: 0.6603 @ 16:01 BST Oct 3

- SUP 1: 0.6527/21 61.8% of the Aug 21 - Sep 17 bull leg / Low Sep 26

- SUP 2: 0.6484 76.4% retracement of the Aug 21 - Sep 17 bull leg

- SUP 3: 0.6463/6415 Low Aug 27 / Low Aug 21 / 22 and a bear trigger

- SUP 4: 0.6373 Low Jun 23

The AUDUSD uptrend remains intact and recent weakness appears to have been a correction. Support to watch lies at the 50-day EMA, at 0.6558. A clear break of this average would signal scope for a deeper retracement and expose 0.6527 once again, a Fibonacci retracement. For bulls, a stronger reversal higher would refocus attention on 0.6707, the Sep 17 high. Initial resistance to watch is 0.6629, the Sep 30 and Oct 1 high.

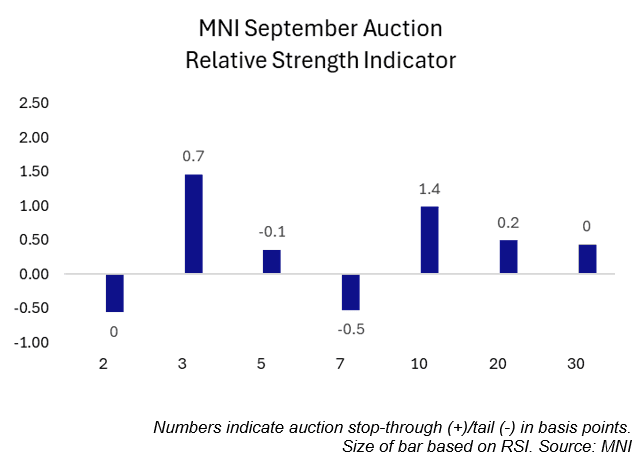

US TSYS/SUPPLY: September's Coupon Auctions Were Generally Solid (2/2)

September’s coupon auctions were generally solid, with three lines trading through, two coming out on the screws and two tailing slightly.

- Looking through the lens of MNI’s Relative Strength Indicator (RSI), five lines saw positive readings while two saw negative readings.

- The 3-year sale was the strongest auction of the month according to MNI’s RSI. The 3-year line traded through 0.7bps, the largest stop through in seven months. Meanwhile, the primary dealer take-up was just 8.4%, the lowest on record (data going back to 2003).

- The weakest sale of the month was the last – the 7-year line. This line saw the second consecutive 0.5bp tail, with the 12.0% primary dealer take-up above August’s 9.8% and July’s record low 4.1%.

September Auction Review:

- 2Y Note on-the-screws: 3.571% vs. 3.571% WI.

- 2Y FRN: 0.200% high margin vs. 0.195% prior

- 3Y Note trade-through: 3.485% vs. 3.492% WI.

- 5Y Note tail: 3.710% vs 3.709% WI.

- 7Y Note tail: 3.953% vs. 3.948% WI.

- 10Y Note trade-through: 4.033% vs. 4.047% WI.

- 10Y TIPS: 1.734% high yield vs. 1.985% prior

- 20Y Bond trade-through: 4.613% vs 4.615% WI.

- 30Y Bond on-the-screws: 4.651% vs. 4.651% WI.