LNG: Alexandroupolis FSRU to Reach 75% Capacity by October: Platts

Sep-17 17:04

Greece’s floating LNG terminal at Alexandroupolis is set to reach 75% operating capacity by early October, operator Gastrade said on Sep. 17, cited by Platts.

- The 5.5 Bcm/y FSRU is currently running at 90.8 GWh/day, or around 50% of capacity. Gastrade expects this to rise to 136 GWh/day within weeks.

- The terminal, which began commercial operations in October 2024, has faced early setbacks. It was taken fully offline in January due to a technical fault and, after restarting in August, initially operated at just 25% of capacity.

- Gastrade said all remaining constraints should be resolved “within the next few months”.

- Alexandroupolis is Greece’s second LNG terminal, alongside the onshore Revithoussa facility.

- So far in 2025, Greece has imported 1.52m mt of LNG, up nearly 70% year on year. The US has supplied the majority, at 1.33m mt.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

PIPELINE: Corporate Bond Update: Starting to Launch, Eli Lilly Guidance Updated

Aug-18 17:01

- Date $MM Issuer (Priced *, Launch #)

- 08/18 $2B #Charter Communications $1.25B 10Y +152, $750M 30Y +177

- 08/18 $1.5B #Marriott Intl $400M 2Y +47, $500M 6Y +85, $600M 10Y +105

- 08/18 $1B #Corebridge Global $500M 3Y +58, $500M 7Y +88

- 08/18 $800M #Northwestern Mutual $500M 3Y +40, $300M 3Y SOFR+66

- 08/18 $500M #Ecolab WNG 10Y +67

- 08/18 $Benchmark DBJ 3Y SOFR+52

- 08/18 $Benchmark RGA Global 3Y +90a, 7Y +120a

- 08/18 $Benchmark McDonald's +5Y +80a, +10Y +100a

- 08/18 $Benchmark Eli Lilly 3Y +28, 3Y SOFR+53, +5Y +40, 7Y +48, 10Y +57, 30Y +65, 40Y +73

EURUSD TECHS: Trading At Its Latest Highs

Aug-18 17:00

- RES 4: 1.1851 High Sep 10 2021

- RES 3: 1.1829 High Jul 01 and the bull trigger

- RES 2: 1.1789 High Jul 24

- RES 1: 1.1730 High Aug 13

- PRICE: 1.1669 @ 16:32 BST Aug 18

- SUP 1: 1.1583 50-day EMA

- SUP 2: 1.1392 Low Aug 1 and bear trigger

- SUP 3: 1.1373 Low Jun 10

- SUP 4: 1.1313 Low May 30

EURUSD is trading at its latest highs and a short-term bullish outlook remains intact. Note that moving average studies are in a bull-mode position, highlighting a dominant medium-term uptrend. A continuation higher would expose key resistance and the bull trigger at 1.1829, the Jul 1 high. Clearance of this level would resume the uptrend. Support to watch is 1.1583, the 50-day EMA. Major support below rests at 1.1392, the Aug 1 low.

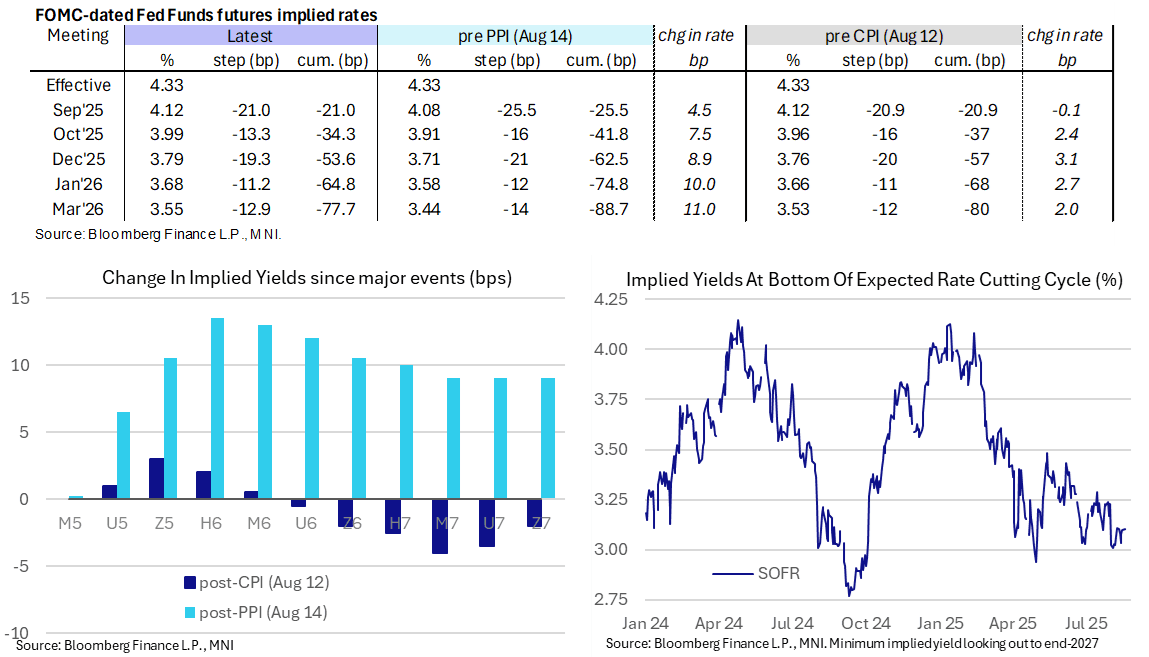

STIR: Fed Rate Path Edges Off Most Hawkish Levels Since After July NFP Report

Aug-18 16:58

- Fed Funds implied rates have given back some of their modest intraday rise but remain higher on the day after what’s been a quiet session awaiting Trump, Zelenskyy and EU leader meetings.

- Cumulative cuts from 4.33% effective rate: 21bp Sep, 34.5bp Oct, 53.5bp Dec, 65bp Jan and 77.5bp Mar.

- Sticking to that very near-term path, the 21bp of cuts for next month has now fully reversed the shift closer to 26-27bp of cuts seen after Tuesday’s CPI report, whilst subsequent meetings are more clearly 2-3bp higher than pre-CPI levels (see table).

- The SOFR implied terminal yield of 3.105% (SFRH7) is near unchanged from Friday’s close, holding the +/-5bp of 125bp range of cuts priced from current levels seen since the Aug 1 payrolls report.

- Powell’s Jackson Hole address on Friday is in focus but will be followed by another round of August payrolls and CPI releases plus QCEW details (for preliminary payroll benchmark revision estimates) all before the next FOMC decision on Sep 17.

- Note that Fed VC Supervision Bowman's (permanent voter, dove) Bloomberg TV appearance appears to have been shifted from today to tomorrow.