ASIA: AI/Tech Lead Continues, Nifty 50 Below Key Level

With the exception of the Hang Seng and NIFTY 50, Asian markets have had a strong week this week taking leads from Wall Street whilst the AI / tech thematic remains. Key names in Taiwan and Korea continue to deliver weekly gains, with TSMC up over 6% and SK Hynix 9% for the week As we approach the NFP Friday, markets will get its next guide on monetary policy with little expectations priced in for the FED's January meeting. Chinese stocks saw one of their strongest starts in some time with the CSI 300 Index reaching a four-year high.

- The NIKKEI at 51,838 is up +1.3% Friday and +2.9% for the week, having hit a new high of 52,518 Tuesday.

- The KOSPI is up only +0.40% on profit taking on tech names, but +6% for the week.

- China's bourses onshore all up between +2.5% - 4.3% with Shenzhen the outperformer whilst offshore the Hang Seng is down -0.65% for the week.

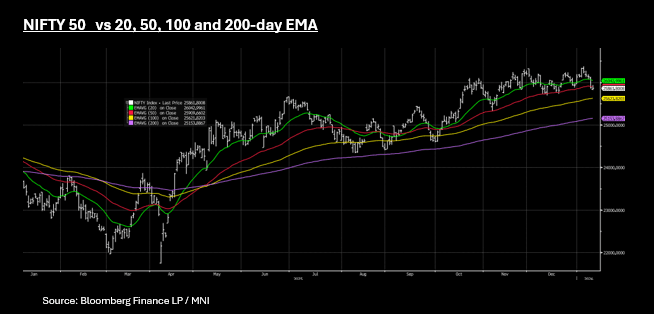

- The NIFTY 50 hit new highs last week and has fallen gradually each day since to lose -1.7% for the week, and through the 50-day EMA.

- SE Asia's major bourses are up for the week with SE Thai and FTSE Malay's gains modest, whilst the JCI delivered almost +2.5% gains

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: Pricing Pressures Weigh on China as Markets Wait for FOMC

Caution is evident in equity markets today ahead of the FOMC with the focus now on the forward pricing as rate cut expectations begin to diminish. In Japan, markets are agonizing over a potential Bank of Japan (BoJ) rate hike this month, following stronger-than-expected producer price data. This has influenced the Japanese yen and market dynamics, though rising yields are expected as a part of the normalization process. Whilst in China inflation remains weak even though it has hit near term highs. CPI at +0.7% was the strongest print in more than a year and a step towards easing deflationary fears but remain well below the 2% target. Producer pricing remained was negative again, having last printed positive in late 2022. The push pull of deflationary pressures is obvious, weighing heavy on China's stocks today.

- The NIKKEI couldn't shrug off the concerns on rates and is down -0.25% eating into modest gains for the first few days of trading.

- China's bourses are all down with onshore down marginally more than the HSI. HSI is lower by -0.43% and CSI 300 is down -0.85%

- The KOSPI seems to refuse to fall at the moment and is up over 5% in December alone. It is doing very little today hardly moving from where it started the day.

- The NIFTY 50 had two consecutive days of falls to start the week but has bounced back Wednesday morning to rise +0.35% after a strong IPO for an e-commerce stock

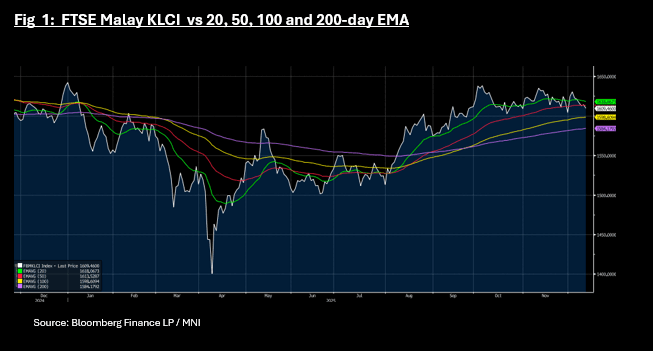

- Malaysia and Jakarta are moving in opposite directions with the FTSE Malay KLCI down -0.29% whilst the JCI is up +0.42%. The FTSE Malay KLCI has now traded below the 50-day EMA and at 1,609 has the 100-day EMA resistance below at 1,598.

OIL: A Hawkish Fed Would Be Seen As Negative For Oil Demand, EIA Data Out Later

Crude has held onto most of Tuesday’s losses during today’s APAC session as it range trades ahead of the Fed decision later. A rate cut is widely expected, which is positive for US energy demand, but a hawkish tone regarding the policy outlook would likely weigh on oil prices. The EIA data release today could also be a market mover.

- WTI is up 0.2% to $58.35/bbl off the intraday low of $58.27, while Brent is also 0.2% higher at $62.05/bbl after falling to $61.96. The USD index is little changed.

- The market focus has returned to demand/supply fundamentals and it will be monitoring Thursday’s IEA and OPEC reports closely after today’s Fed and EIA data.

- A record market surplus in 2026 has been forecast for some time and upward revisions will be watched closely, especially given increased OPEC and non-OPEC output and elevated levels of seaborne crude.

- Bloomberg reported that US oil inventories fell 4.8mn barrels last week, according to those familiar with the API data. Product stocks were higher with gasoline stocks up 7.0mn and distillate 1.0mn.

- Not only is the FOMC decision announced later on Wednesday but Q3 US employment costs and November budget data also print. The BoC also decides rates. ECB President Lagarde gives an interview on the future of the euro and dollar. The ECB’s Donnery and Machado also appear.

FOREX: USD - BBDXY Well Supported Heading Into FOMC

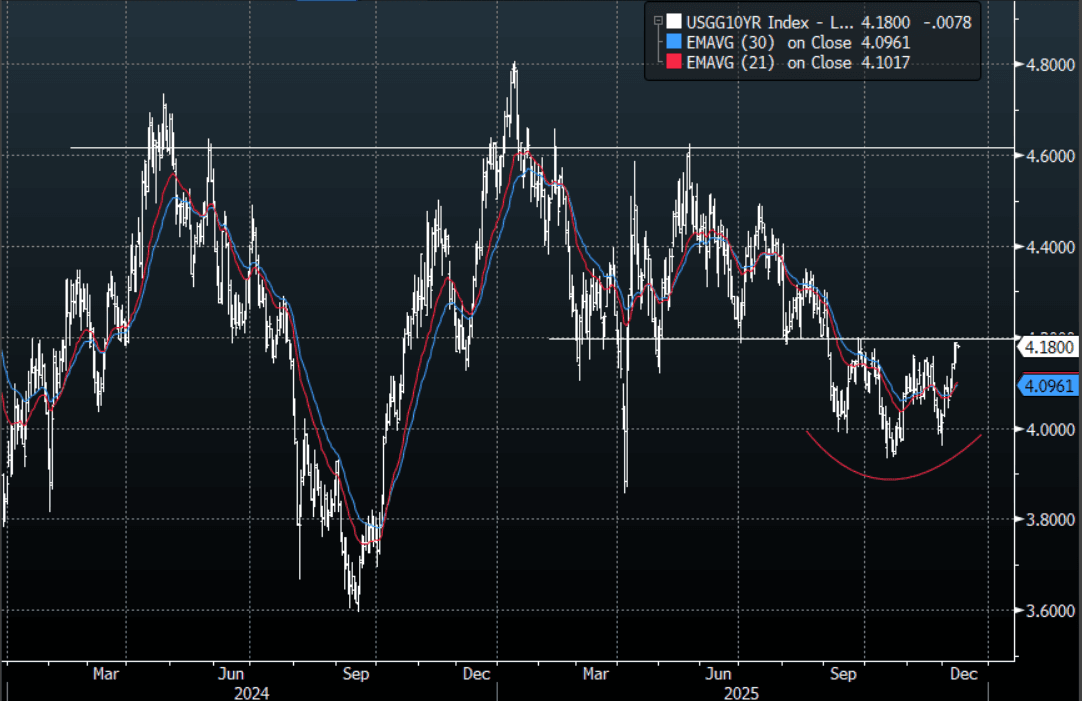

The BBDXY has had a range today of 1214.46 - 1215.08 in the Asia-Pac session; it is currently trading around 1214, -0.05%. The USD has traded sideways in a quiet Asian session. US yields continue to extend higher as we approach the FOMC, and both risk and the USD have begun to take notice. The USD continues to see decent demand back toward the 1210-1211 area and it looks like the range 1210-1230 could be here for the moment, or at least until the FOMC. On the day look for resistance again back towards the 1216-1218 area where sellers should remerge initially, a break above here would imply a test of the pivot around 1221-1223. The US 10-year yield is approaching the pivotal 4.20% area so the FOMC will have a big say in whether this area breaks or caps yields going into the end of year. Which has direct implications for the fortunes of the USD.

- EUR/USD - Asian range 1.1622-1.1629, Asia is currently trading 1.1625. The pair continues to consolidate above the 1.1600 area. On the day, all eyes will be focused on the FOMC tomorrow morning, dips toward 1.1580-1600 should be supported initially, looking to retest the 1.1660-1680 area again eventually.

- GBP/USD - Asian range 1.3296-1.3305, Asia is currently dealing around 1.3305. The pair is consolidating around the 1.33 area. I remain skewed toward shorts but patience is required and we are now approaching levels where I will be watching for any signs of potentially topping out. On the day GBP should see support back toward the 1.3250-1.3280 area, while above here look for the market to test the 1.3350-80 area again at some point. FOMC will dictate which side is tested.

- Cross asset : SPX +0.02%, Gold $4205, US 10-Year 4.18%, BBDXY 1214, Crude Oil $58.35

- Data/Events : Italy Industrial Production MoM

Fig 1: US 10-Year Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P