US CREDIT SUPPLY: Airbnb (ABNB):$Bmark; 3Y +100a, 5Y +115a, 10Y +135a-Fair Value

Airbnb: NEW DEAL - Airbnb $Bmark; 3Y +100a, 5Y +115a, 10Y +135a - Fair Value (ABNB; Baa1/A-/NR) * U...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

PIPELINE: Corporate Bond Update: Cencora 5Pt, Walt Disney 4Pt on Tap

Walt Disney returns to credit market after near 6 year absence. For reference, Disney issued $11B over 6 tranches on May 11 '20 ($1.5B 5Y +145, $1B 7Y +170, $2.5B 10Y +195, $1.75B 20Y +210, $2.75B 30Y +220 and $1.5B 40Y +240) after issuing $7B in September 2019. Rate locks and speculative selling helping keep lid on this morning's bid in rates, today's Disney issuance estimated at $7.5B:

- Date $MM Issuer (Priced *, Launch #)

- 02/10 $2.5B Bank of England 3Y +5

- 02/10 $750M #IADB 5Y SOFR+28

- 02/10 $Benchmark Cencora 3Y +80a, -5Y +90a, 7Y +100a, 10Y +105a, 30Y +115a

- 02/10 $Benchmark Walt Disney* 3Y +55a, 3Y SOFR, 5Y +65a, 10Y +85a

- 02/10 $Benchmark Alexandria Real Estate 10Y +140a

- 02/10 $Benchmark Pulte Group 5Y +90a, 10Y +115a

- 02/10 $Benchmark Sysco +5Y +95a, 10Y +110a

- 02/10 $500M Loews Corp 10Y +105a

- 02/10 $Benchmark Tyson 10Y +115a

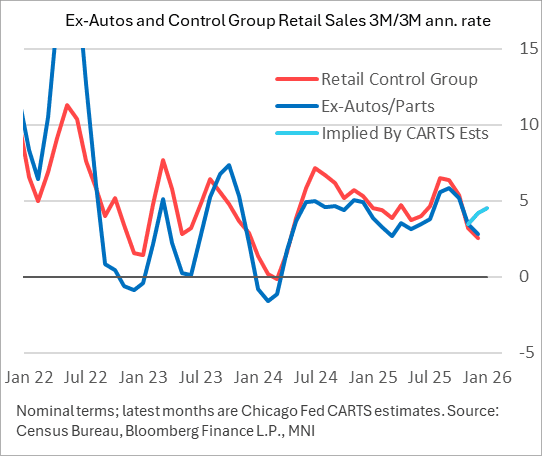

US DATA: Retail Revisions And Control Group Miss Confirm Q4 PCE Slowdown

December's advance retail sales data was roundly weaker than expected, which in addition to lower revisions in prior months will likely mean a pullback in Q4 personal consumption expenditures estimates in the GDP accounts. Even prior to this report, January had been expected to be a weak month for retail sales given incoming indicators, so there will be concerns about the momentum of consumption going into 2025. And the report is in nominal terms, so in volume terms Q4 2025 suddenly looks to have been closer to flat instead of robust for core goods sales.

- The big surprise is that Control Group sales contracted 0.1% M/M in December vs expectations of a 0.4% expansion, for the first drop in 3 months alternate series including Chicago Fed CARTS had pointed to a decent rise. This was compounded by a downward revision to prior (0.2% from 0.4%) and a second consecutive downward revision to October, which originally printed 0.85%, then was revised down to 0.6%, and now to 0.4%.

- The latter will pull down the base effect for core retail sales growth in Q4 and looks likely to be met with a downgrade in Atlanta Fed GDPNow tracking of PCE of 3.07% Q/Q SAAR for overall consumption which would represent a slowdown from 3.5% prior. The first read of Q4 GDP is out February 20.

- The 3M/3M annualized rate of Control Group sales is now down to 2.6% in December, vs 6.4% at the end of Q3 (September). If you look at it on a Y/Y basis, sales growth is now just 3.4%, slowest in 19 months. The CARTS estimates in the chart below (which will be revised of course after this release) show how divergent the "actual" data were in December vs expectations.

- Indeed the report brought downgrades across the major aggregates, all of which also missed expectations in December: headline of 0.0% (actually slightly contractionary at -0.02% vs 0.4% survey, 0.4% prior rev from 0.5%) and ex-auto/gas of 0.0% (0.4% survey, 0.3% prior rev from 0.4%).

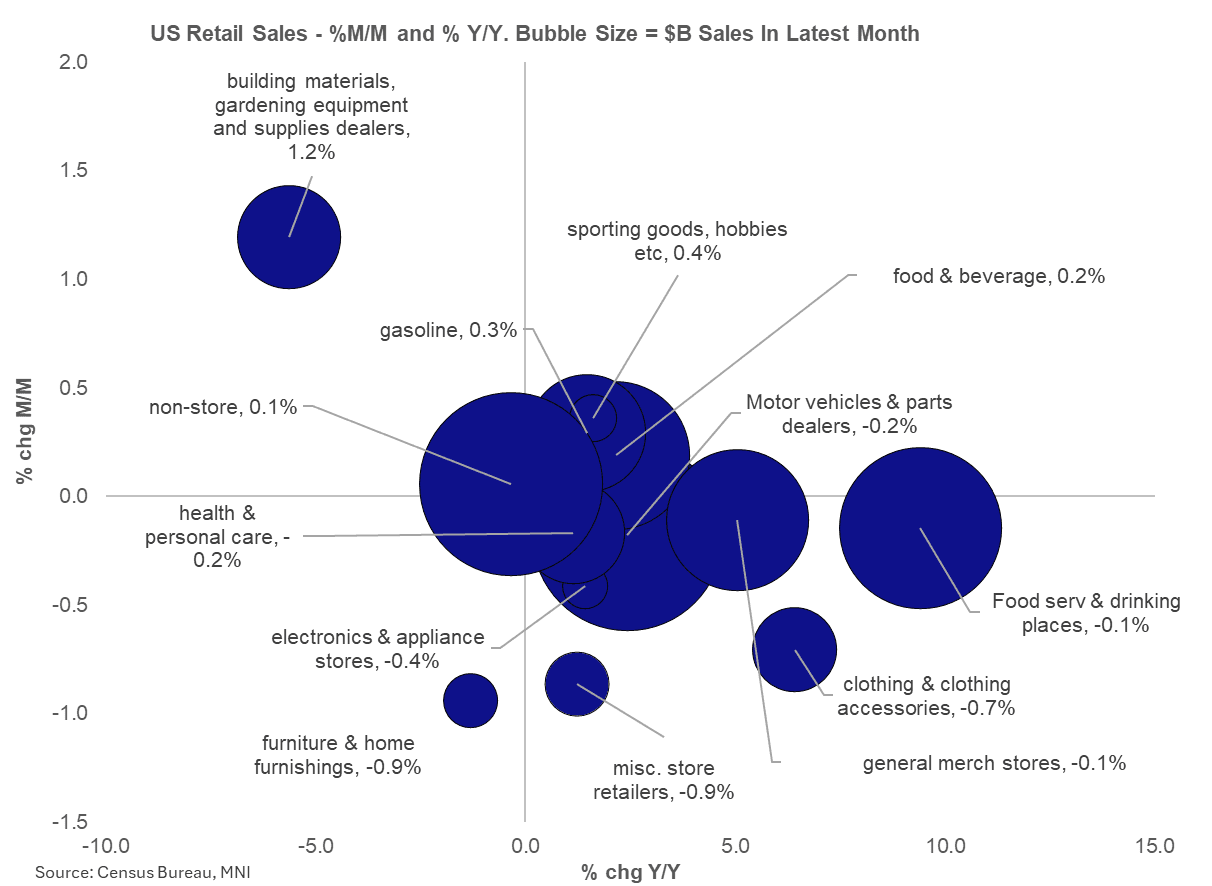

- Looking at the individual categories, December saw an unexpected contraction in vehicle sales (-0.2% M/M, the largest category of retail sales) and food services/dining places (-0.1% after +0.6%), each for the 2nd fall in 3 months (October too).

- Neither of these are in the control group, however: what we did see is broad weakness across major retailer categories, notably non-store (ie internet retailers) flatlining the last 2 months at 0.1% after 0.0% in November; this is the 2nd largest retail sales category and we can't help but note that revisions have been substantial the last couple of months. October was originally reported at +1.8% and November at +0.4%, those readings are now +0.7% and +0.0%, a major component in the overall downward revisions.

- Also general merchandise and miscellaneous stores saw a December contraction, not to mention clothing, furniture, electronics, and health/personal care. We saw a 2nd consecutive strong performance in building materials (1.2% in Nov and Dec) but this isn't in the Control Group.

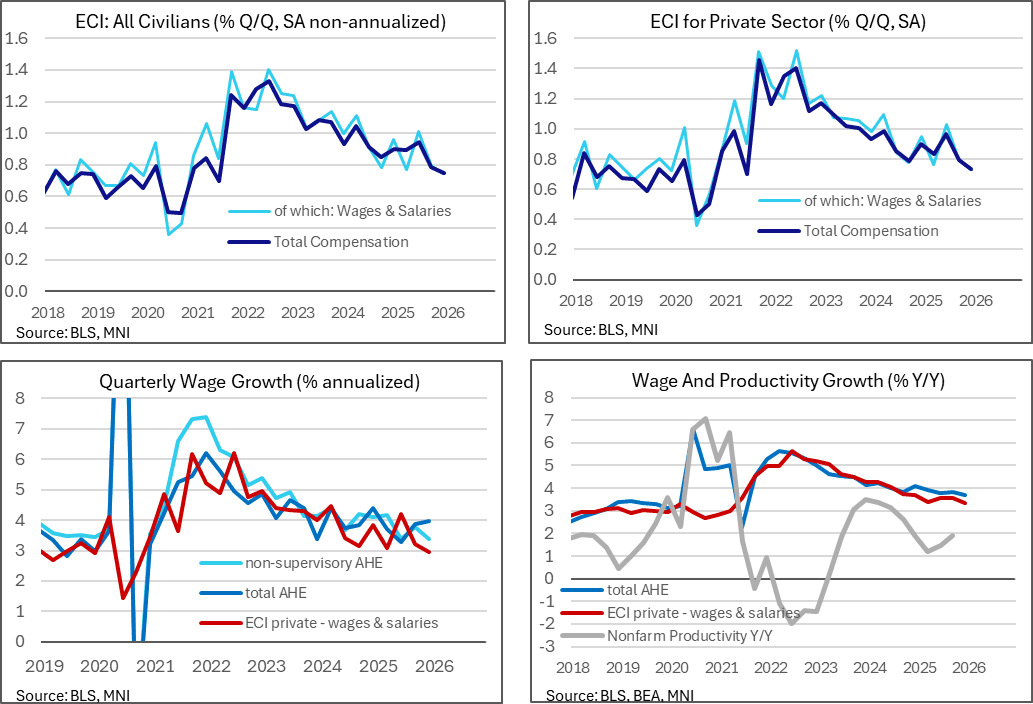

US DATA: Wage Growth Moderation Continued In Q4 ECI Report

The Q4 ECI update continued a trend moderation in wage growth. This more comprehensive wage growth metric, which the Fed puts much more weight on when it comes to assessing wage dynamics, offers a softer take than hourly earnings data in recent monthly payrolls reports.

- The employment cost index was on the soft side of expectations in Q4 as it increased 0.75% Q/Q non-annualized (cons 0.8) after 0.79%.

- It left annualized growth of 3.0% annualized in Q4 for its softest since 2Q21 after 3.2% in Q3, 3.8% in Q2 and 3.6% in Q1.

- The wages & salaries component told the same story, easing to 3.0% annualized in Q4 after 3.2% in Q3, with the private sector-only version also at 3.0% after 3.2%.

- These comprehensive wage growth metrics show a more modest backdrop than the average hourly earnings data from the monthly payrolls report, with its 4.0% annualized in Q4 after 3.9% in Q3 in the latest vintage before Wednesday’s update for January. The non-supervisory component, accounting for approximately 80% of employees is a little closer to ECI metrics but still stronger at 3.4% in Q4 after 3.8% in Q3.

- Coupled with still robust productivity growth (4.9% annualized or 1.9% Y/Y in Q3) and nominal wage growth closer to 3% in 2H25 has started to point to disinflationary pressures stemming from the labor market.

- The return to nominal wage growth rates closer to the pre-pandemic period follows quit rates easily falling back into pre-pandemic ranges for some time now.