FOREX: A$ & NZ$ Outperform As Greenback Moderates

After underperforming on Tuesday, Aussie and Kiwi are outperforming the rest of the G10 against the greenback during today’s APAC trading. The BBDXY USD index is close to its intraday low to be down 0.2% after it finished 2024 strongly.

- AUDUSD rose back above 62c to be up 0.5% at 0.6217 after a high of 0.6223. It is trading back above resistance at 0.6199. A notional A$620mn of options expired today with a strike of 0.6175. The S&P Global December manufacturing PMI was revised down to 47.8 and CoreLogic December home values fell 0.2% m/m.

- NZDUSD is 0.4% higher at 0.5618, close to the intraday high, leaving AUDNZD little changed at 1.1065. NZ markets have been closed today.

- USDJPY is 0.1% lower at 157.08, close to the intraday low, after a high of 157.78 early in the session. AUDJPY has trended lower after reaching 97.93 and is currently up 0.3% to 97.66. Japan has also been shut today.

- European currencies are stronger against the greenback with EURUSD up 0.2% to 1.0373, GBPUSD +0.2% to 1.2539 and USDNOK -0.2% to 11.36. EURGBP is down slightly to 0.8273.

- Later US jobless claims, November construction spending and S&P Global final December manufacturing PMI, European December manufacturing PMIs and euro area November M3 data print.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

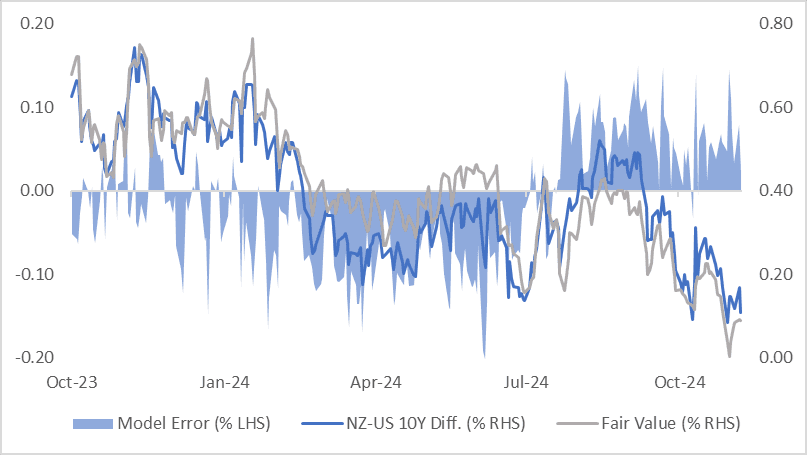

BONDS: NZ-US 10Y Differential Lowest Since Mid-2021

NZGBs closed the day in a bull-flattening pattern, with benchmark yields ending flat to 4bps lower.

- The 10-year NZGB slightly outperformed, with the NZ-US and NZ-AU 10-year yield differentials tightening by 1-2bps.

- The NZ-US 10-year differential, now at +10bps, is hovering near its tightest levels since mid-2021.

- A simple regression analysis of the 3-month forward swap rate spread (1Y3M) over the past year indicates the 10-year yield differential is close to its estimated fair value of +9bps.

- Notably, the regression error has fluctuated within a range of ±20bps over the past year, highlighting some variability in the relationship.

- The 1Y3M differential continues to be a key driver of market expectations for long-term yield convergence.

Figure 1: NZ-US 10-Year Yield Differential

Source: MNI – Market News / Bloomberg

OIL: Crude Range Trading Pressured By Stronger US Dollar

Oil prices have been trading in a narrow range and are off their intraday lows to be down slightly on the day. WTI is down 0.1% to $68.18/bbl after a low of $67.91 and Brent is 0.1% lower at $71.93/bbl after falling to $71.68. The stronger US dollar continued to pressure crude (USD BBDXY +0.1%) offsetting mild optimism from China’s manufacturing PMI.

- Cold weather in Europe has increased heating demand boosting natural gas prices, but also distillate which includes heating oil.

- US industry-based inventory data is out later today. Crude stocks have been declining but products rising. The official EIA figures are on Wednesday.

- The focus of the week will be Thursday’s OPEC+ meeting, where it seems likely that supply increases will be pushed out into Q1, and Friday’s US payrolls report.

- Later the Fed’s Daly, Kugler & Goolsbee and ECB’s Cipollone speak. In terms of data, US October job openings and Spanish November unemployment print.

BONDS: NZGBS: Bull-Flattener, NZ-US 10Y Diff. Near Lowest Since Mid-2021

NZGBs closed showing a bull-flattener, with benchmark yields flat to 4bps lower.

- The NZGB 10-year slightly outperformed on the day, with the NZ-US and NZ-AU 10-year differentials 1-2bps tighter. At +10bps, the NZ-US differential sits near its tightest levels since mid-2021.

- NZ export volumes fell for a second straight quarter, adding to signs of a mid-year recession. Exports of goods dropped 1.8% in the third quarter from the previous three months, Statistics New Zealand said. Imports rose 3%, meaning net exports — which are comparable to measures used in the gross domestic product report — fell 4.8% from the second quarter, when they dropped 7.9%. (per BBG)

- Swap rates closed 3-7bps lower.

- RBNZ dated OIS pricing closed flat to 2bps softer, with late-2025 leading. 42bps of easing is priced for February, with a cumulative 94bps by November 2025.

- Tomorrow, the local calendar will see ANZ Commodity Prices. The RBNZ also appears before a Select Committee for its Annual Review.

- On Thursday, the NZ Treasury plans to sell NZ$200mn of the 3.00% Apr-29 bond, NZ$250mn of the 4.25% May-34 bond and NZ$50mn of the 2.75% Apr-37 bond.