EUR: Adding to the EUR Downside Option

Jun-05 13:44

Adding to the CME EUR Option downside: * EURUSD (2nd July) 1.1500p, bought for 0.0023 and now 0.002...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

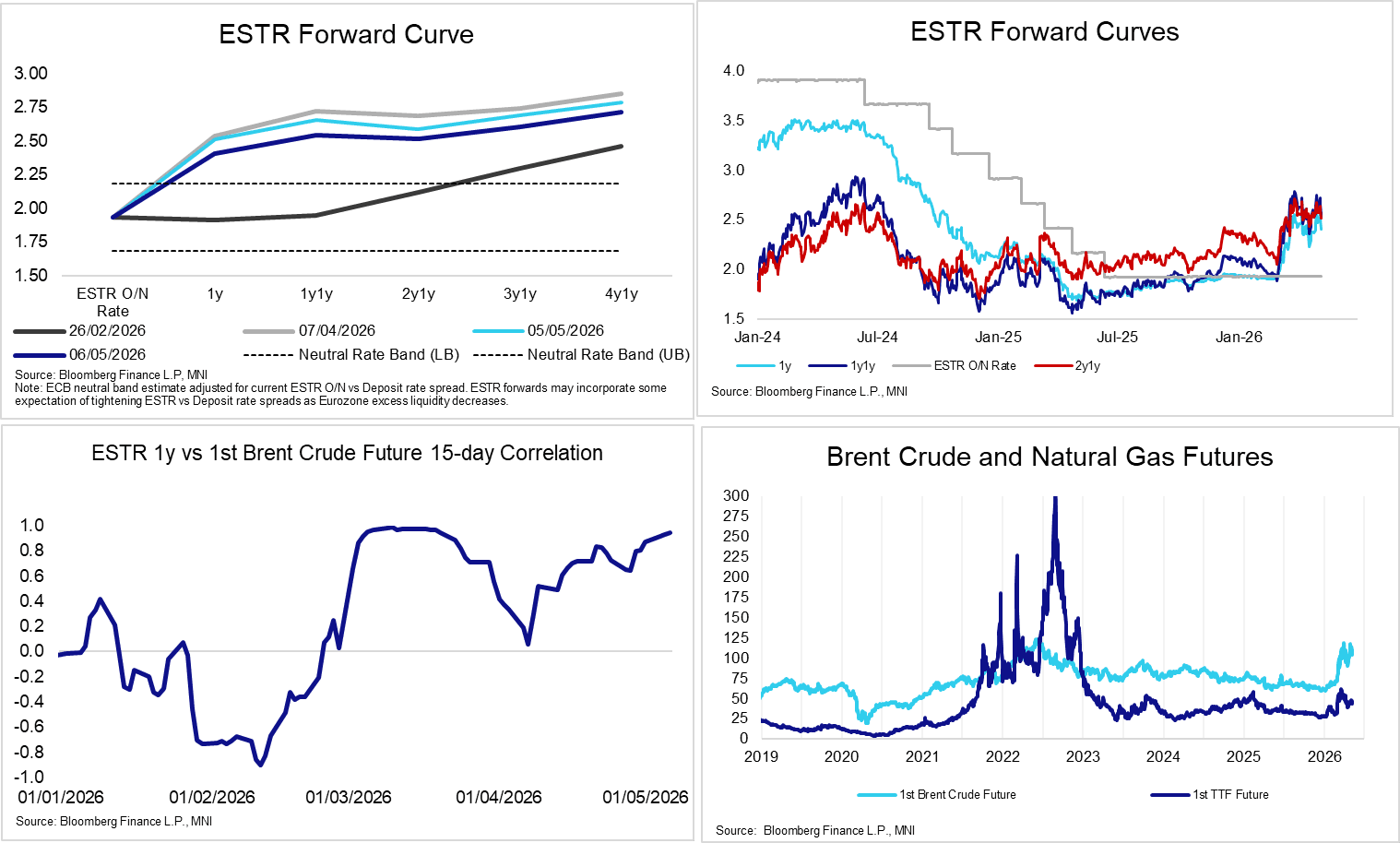

STIR: Front-ECB Rates Off Earlier Extremes, Near-Perfect Correlation With Oil

May-06 13:41

Front-end EUR implied rates have moved away from earlier session lows amid more tempered optimism around a US-Iran ceasefire agreement. That said, the ESTR 1y and 1y1y rates remain 10 and 12bps lower on the session respectively, with ECB-dated OIS now pricing 62bps of hikes through December (vs 75bps at yesterday’s close).

- It’s clearly too early to draw any strong conclusions for the ECB at this stage, given incoming headline flow remains heavy and the next rate decision (which includes updated projections) is still 5 weeks away - a very long time in the context of this war. The chart below highlights that front-end rates are essentially moving in lockstep with crude oil at present.

- That said, if a ceasefire agreement is reached and the Strait of Hormuz is re-opened soon, there is scope for 2026 ECB hike pricing to unwind further.

- We think a one-and-done ECB reaction is more plausible than a complete look-through (i.e. no hikes) in a re-opening scenario because:

- The March baseline projections were conditioned on a rate path with 40bps of hikes, and energy prices may still settle well above pre-war levels.

- ECB President Lagarde has previously highlighted that “to leave such an [inflation] overshoot entirely unaddressed could pose a communication risk: the public may find it difficult to understand a reaction function that does not react”. The April press conference tone also hinted strongly at a June hike.

- Our Policy Team’s latest sources piece has highlighted that there is a high bar to not hike in June, with one source noting that a hike would be appropriate even if there was a quick end to the Iran conflict.

US TSY OPTIONS: Large Jun'26 10Y Put Buyer

May-06 13:38

- +30,000 TYM6 110 puts, 12 ref 110-25.5/0.10%

US TSYS/SUPPLY: TBAC Debated Treasury Investing Excess Liquidity In Repo Markets

May-06 13:30

One interesting section of TBAC’s report was on discussions around Treasury being able to invest excess liquidity in the overnight repo market. Relevant excerpts reproduced below, with the full report here

- “By virtue of its cash management policy, Treasury holds a level of cash generally sufficient to cover one week of outflows in the TGA. Volatility in Treasury’s cash needs generates intramonth excess in the TGA, and the Committee welcomed the opportunity to explore the potential benefits of investing that excess liquidity in the overnight repo market”

- “The presenting member found there was scope for Treasury to invest excess cash in repo markets to the extent that positive net returns can be generated without creating market disruption. However, ultimately the return generated for Treasury was not expected to be positive in all environments, and was likely to be only modestly positive when positive at all. The presenting member found that lending out excess cash would be likely to have a small positive return (0-2bps) in an ample reserve regime, a 5-10bp return in a scarce reserve regime, and likely no positive economic value in an abundant reserve regime.”

- “Ultimately, while the Committee felt that there would likely be a marginal benefit to Treasury to engage in overnight repo trading with excess cash from the TGA, the scale of the economic benefit was not overly compelling relative to the perceived challenges of roll out. That said, further study, especially of possible program design, could help to inform a more refined recommendation, including a gradual and measured roll out, should there be one.”

Trending Top

Jun-05 14:48

Jun-05 14:47