AUSSIE BONDS: ACGB Nov-32 Supply Faces Higher Yield But Flat Curve

The Australian Office of Financial Management (AOFM) will today sell A$900mn of 1.75% 21 November 20...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

NATGAS: European Gas Follows Oil Higher As Hormuz Reopening Looks More Distant

European gas followed oil lower on Tuesday as Israel and Iran agreed to stop attacking each other and US President Trump reiterated that there is still likely to be a US-Iran deal to reopen the Strait of Hormuz, which is necessary for Qatar to ship LNG out of the Gulf. However, the latest US attacks on military sites in southern Iran in retaliation for the downing of a US helicopter is driving energy prices cautiously higher.

- Uncertainty over a permanent peace remains extremely elevated as there are reports of further explosions in southern Iran and the foreign minister said the US is testing Iran’s determination. Trump said Tuesday that they’re “in the final throes of what will be a very, very good deal” but it remains to be seen if that remains the case.

- Dutch TTF fell 1.5% to EUR 49.065 on Tuesday after a low of EUR 48.335 but is currently up to EUR 49.605. It reached EUR 51.485 on Monday following tit-for-tat attacks between Israel and Iran.

- Europe needs global flows to rise again since Asian gas demand for cooling has increased adding to Europe’s difficulties building inventories. European storage is 42.8% full, around 10pp below the same time last year.

- Demand in India is increasing with the onset of summer but with the conflict in the Middle East, the US became its largest LNG supplier in May. Import volumes rose 227% m/m, according to ITN.

- US gas is down 4.6% in June driven by ample supply due to a pickup in production, lower domestic and LNG export demand. It fell 0.3% on Tuesday to $3.138 and is currently around that level. Although it seems that flows to LNG export facilities are picking up again with them rising 7.1% w/w on Tuesday.

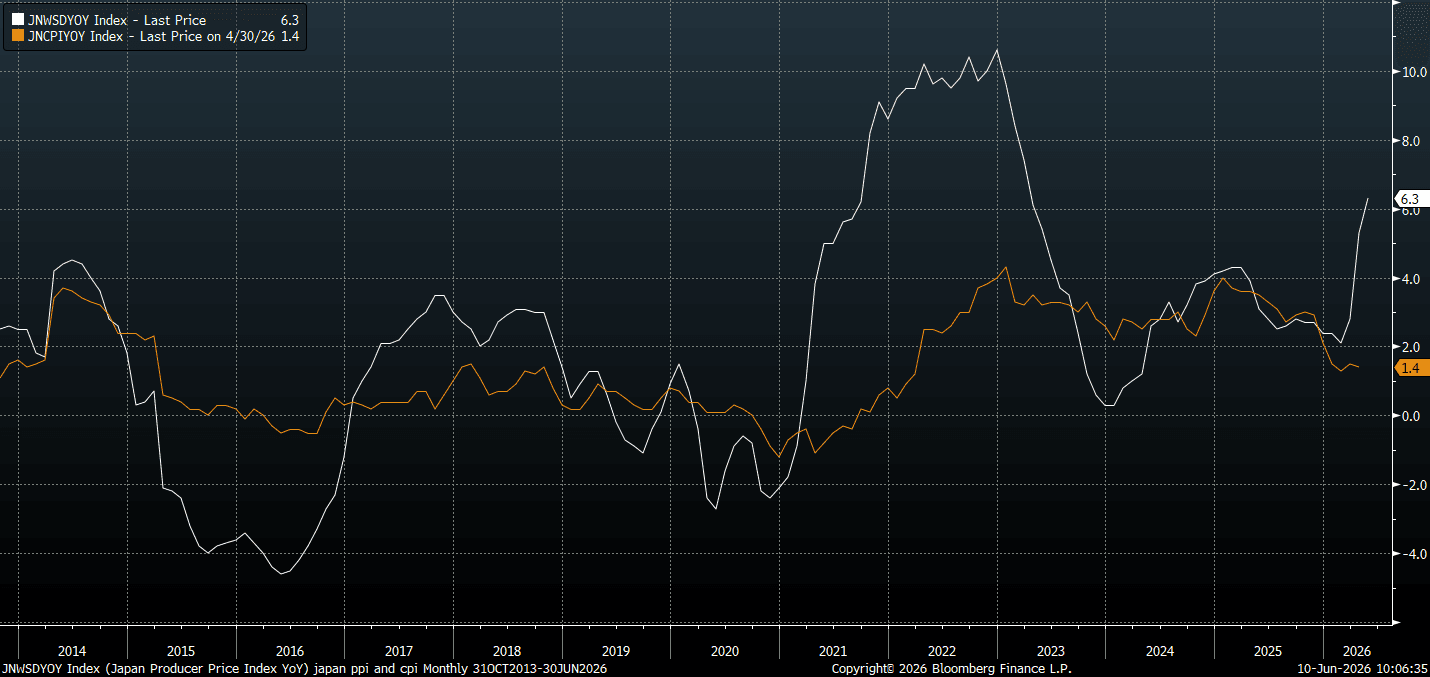

JAPAN DATA: PPI Stronger Than Forecast, Import Prices Surge To +25%y/y

Japan's May PPI rose 0.9%m/m, versus a 0.8% consensus forecast, while the Apr gain was revised up to a 2.8% gain (originally reported as 2.3%). In y/y terms the PPI rose 6.3%, against a 5.6% forecast (5.3% was the Apr outcome, also revised up). The chart below plots the headline PPI y/y (the white line), versus headline CPI y/y. PPI momentum is back to 2023 levels and is pointing to a rebound in CPI y/y as we progress through 2026. This should support the case for continued BoJ policy normalization, although it remains to be seen if the market can price in more than around 2 hikes this year.

- Our Tokyo based policy team noted yesterday: Strong corporate goods price index data are likely to support a rebound in consumer price inflation in the coming months, reinforcing the case for a near-term policy rate hike, while the recent slowdown in CPI growth has likely not altered the Bank of Japan's inflation outlook, MNI understands.

- For today's print, the acceleration was driven by petroleum and coal products, where prices rose 13.8% y/y in May from 5.3% in April, and by nonferrous metals, which climbed 42.2% following a 37.9% increase the previous month.

- Import prices were up strongly, now +25.5%y/y, from +21% in Apr. We were close to flat on this metric at the start of the year. The weaker yen, higher commodity prices are clearly impacting.

Fig 1: Japan PPI (White Line) & Headline CPI Y/Y

Source: Bloomberg Finance L.P./MNI

CNH: Holding Recent Ranges, May Inflation Data On Tap

Spot USD/CNH tracks near 6.7770/75 in early Wednesday dealings. Tuesday dips in the pair sub 6.7700 were supported. The currency finished slightly stronger for Tuesday's session. The 20-day EMA resistance point rests near 6.7870. Broader USD sentiment was supported as Tuesday trade unfolded, as oil recovered from lows amid hawkish US/Iran rhetoric. This has been followed up by fresh US strikes on Iran (in response to the US helicopter being downed). Oil futures are higher, but only modestly. Spot USD/CNY finished up at 6.7746 yesterday, while the CNY CFETS basket tracker lost a little ground to 101.62. This is the first decline for the index since the end of May.

- In the cross asset space, US-CH yield differentials edged off recent highs, likely providing some modest impetus for USD/CNH, while the USD/CNY fixing trend has also drifted lower in recent sessions.

- Today we have May inflation data. The market expects a further improvement in y/y PPI momentum to 3.9% (from 2.8% prior). CPI y/y is forecast at 1.3% (versus 1.2% prior). Core CPI is seen steady at 1.2%y/y.

- Yesterday we had stronger than expected trade figures for May, with higher exports supporting higher CNY basket levels all else equal. A firmer than expected PPI today would also support this backdrop.

- Our policy team noted late yesterday: The yuan is likely to strengthen further against the dollar in the second half of 2026, with forex experts and advisors pointing to 6.60 as a level with which the People’s Bank of China would be comfortable and with the currency supported by robust exports and the willingness of Chinese companies to settle foreign exchange.

- May FX settlement data is due on June 15.