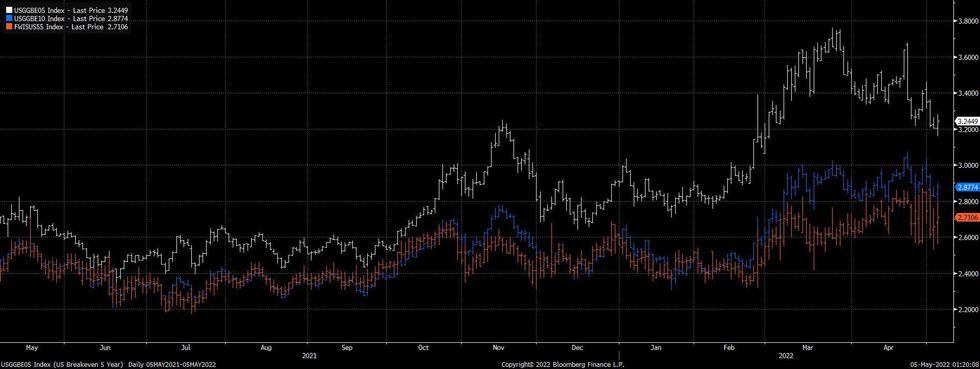

US TSYS/TIPS: A Quick Look At Market-Based Inflation Expectations

U.S. real yields moderated a touch vs. pre-FOMC levels in the wake of the latest Fed decision, after Chair Powell pushed back against the idea of 75bp rate hikes. Still, the 10-Year real yield metric remained in positive territory after its first meaningful break above 0% in the current cycle, which took place earlier in the week. The market has shown signs of some faith in the Fed being able to tame inflation (although the transitory nature of inflation over along enough horizon debate is of course a factor there). 5- & 10-Year breakeven rates operate away from their cycle highs, but still remain elevated when compared to the Fed’s inflation target, sitting at ~3.25% & ~2.85%, respectively, late in the NY session. Meanwhile, 5-Year/5-Year inflation swaps sit at ~2.70%.

Fig. 1: U.S. 5-Year & 10-Year Real Yields & 5-Year/5-Year Inflation Swaps (%)

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

KRW: Won Tad Firmer After CPI Beat

South Korea's CPI rose 4.1% Y/Y in March, printing slightly above the consensus forecast of +4.0%, reaching the fastest pace since 2011. FinMin Hong attributed the acceleration in price growth to the war in Ukraine and announced the expansion of oil tax cuts to provide some relief to citizens facing rising costs of living. Headline inflation has now stayed above the BoK's target of +2.0% Y/Y for 12 months in a row, ramping up pressure on policymakers to withdraw more stimulus. Note that the BoK is due to hold a monetary policy meeting on April 14 even as the Bank remains in a state of interregnum, with parliamentary hearings of Governor-nominee Rhee yet to conclude.

- The sister of North Korean Supreme Leader, who also sits on the Central Committee of the Workers' Party of Korea, said South Korea is not her country's "principal enemy" and Pyongyang will never deliver the first strike. At the same time, she rattled the nuclear sabre and warned that North Korea would not hesitate to use its unconventional arsenal if attacked.

- Spot USD/KRW trades at KRW1,213.75, just shy of neutral levels, with bears looking for losses past the 50-DMA at KRW1,208.63, followed by the 100-DMA at KRW1,197.52. Bulls would be pleased by a rebound above Mar 28 high of KRW1,227.30.

- USD/KRW 1-month NDF last seen at KRW1,214.15, a tad lower on the day. The 50-DMA at KRW1,210.80 provides the initial layer of support, with topside focus falling on Mar 28 high of KRW1,228.45.

- Looking ahead, South Korea's BoP current account data will be released on Friday.

AUSSIE BONDS: IRM3/U3 Flattener Flow

IRM3/U3 ~1.0K given at 21 in recent dealing.

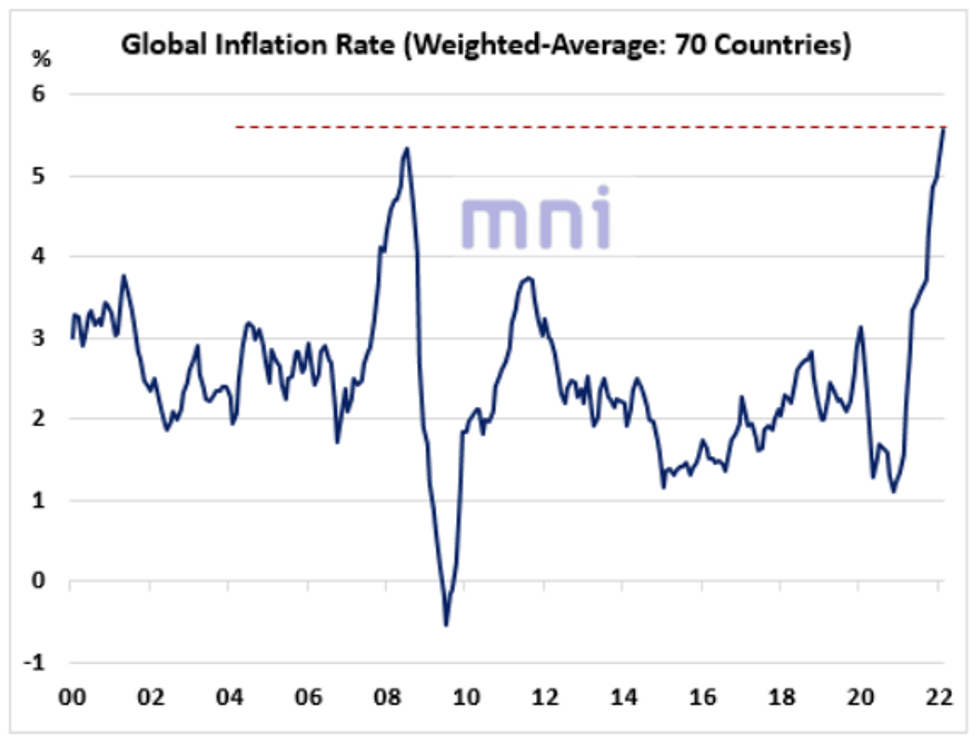

GLOBAL: Global Inflation Surges Above Pre-GFC High

Executive Summary:

- Inflationary pressures continue to remain elevated in most of the developed and emerging market economies, mostly driven by the surge in energy and food prices.

- Some EM central banks have hinted that the surge in inflation risks will prolong the tightening cycle in order to ease the selling pressure on the currency, especially in the CEE region.

- Our global inflation gauge surged to 5.6% in February (based on the inflation rate of 70 DM and EM countries), exceeding its pre-GFC high of 5.3%.

Link to full publication:

Source: Bloomberg/MNI.