AUSSIE BONDS: A Little Firmer

Aussie bond futures have ticked higher over the last couple of hours or so, registering fresh session highs, perhaps aided by the AOFM announcing a step down in the DV01 on offer at next week’s ACGB auctions (to A$916K across 2 auctions vs. A$1.539mn across 3 auctions this week), with no issuance beyond the 10-Year bucket. YM +7.5 & XM +9.5 at typing, with the 10- to 12-Year zone still outperforming on the curve.

- Little has changed on the EFP front vs. was outlined earlier, i.e. narrowing driven by 3s, with the 3-/10-Year box steepening, while Bills run 1-7bp richer through the reds.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY OPTIONS: TYU2 120.50 Calls Blocked

Latest block trade lodged at 03:28:45 London/22:28:45 NY:

- TYU2C 120.50 calls 2,500 lots blocked at 0-49, look like a buyer. Delta +39%.

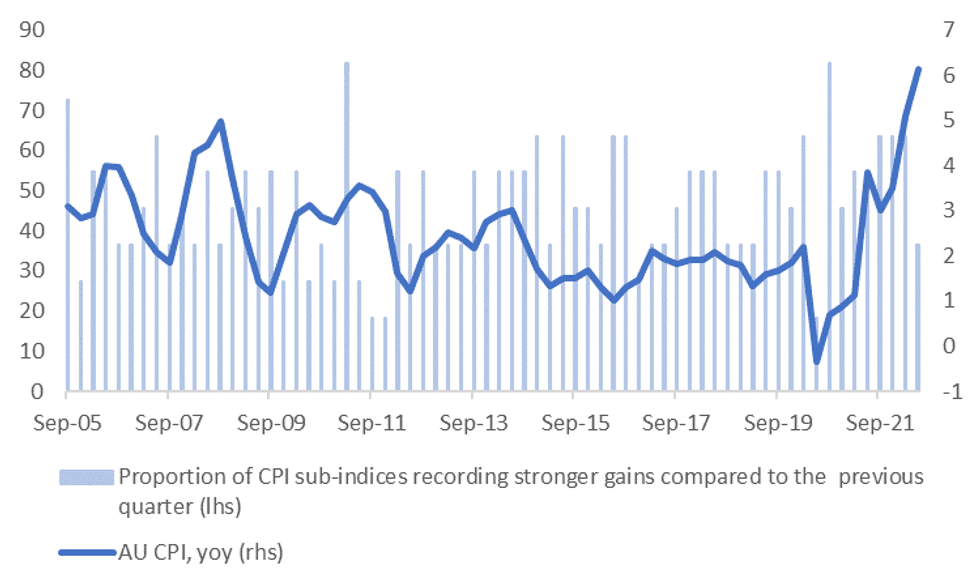

AUSTRALIA: CPI Momentum Eases A Touch

Looking at the breakdown of the Australian Q2 CPI shows that 10 out of the 11 major sub-indices recorded rises in Q2. This was the same as Q1 and Q4 from last year. However, the number of sub-indices that recorded faster quarterly changes compared to Q1 was down to 4 out of 11. This compares with 7 out of 11 for the previous 2 quarters, see the first chart below.

Fig 1: Australian CPI Momentum

Source: MNI/Market News/Bloomberg

Source: MNI/Market News/Bloomberg

- Looking at momentum on a YoY basis, 10 out of 11 of the sub-indices were positive in YoY terms, a fresh high for this upturn in inflation.

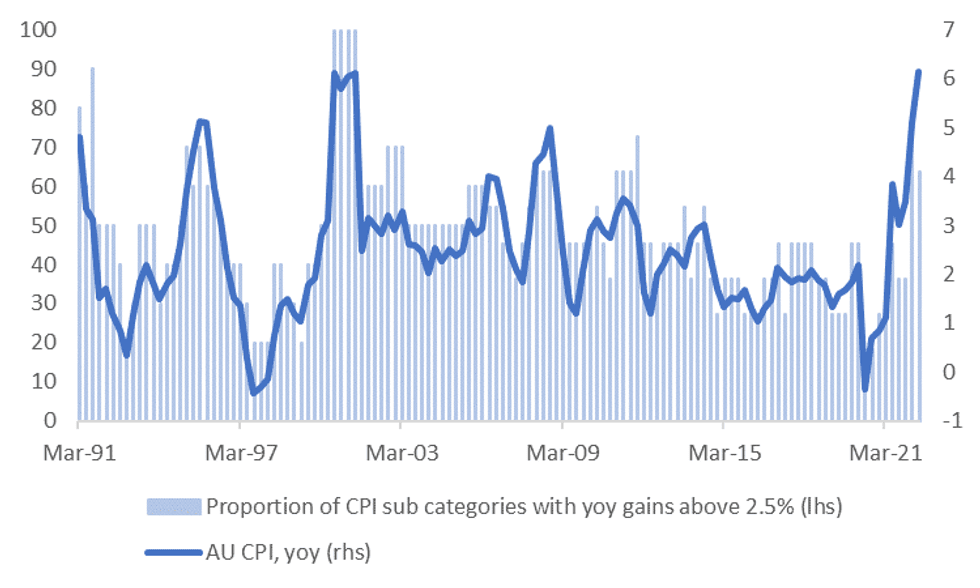

- However, it's interesting to note the proportion of sub-indices recording YoY gains above 2.5% (the mid-point of the RBA's inflation target) fell back slightly to 7 out of 11 from 8 out of 11 in the previous quarter, see the second chart below.

- Of course, inflation pressures can still pick up further from here, particularly if we see underlying wage gains build further momentum. Actual inflation is also still very strong, given the RBA's preferred core measure is highest on record at just under 5% yoy, while the ABS noted goods inflation is at the strongest pace since the late 1980s.

- Still, the RBA may take some comfort from today's print around the need to get even more aggressive than it already has in terms of the pace of rate hikes (i.e. needing to move beyond the 50bps rate hike pace).

Fig 2: Proportion of Major Australian CPI Sub-Indices Running Above 2.5% YoY Pace

Source: MNI/Market News/Bloomberg

Source: MNI/Market News/Bloomberg

STIR: Cover Of Hawkish RBA Bets Post-CPI

OIS covering the RBA’s August meeting now sit at ~1.80% (vs. the current effective cash rate of 1.31%), ~8bp lower on the day, with some covering of hawkish RBA bets evident in the space post-CPI. Further out, post-CPI peak to trough we saw RBA dated Dec OIS unwind ~30bp of tightening premium before recovering from lows of the session to last sit at ~3.25%, a touch over 15bp lower on the day and still ~195bp above current effective cash rate levels, equating to 39bp of tightening being priced in across the remaining 5 RBA meetings of ’22 (on a simple average basis).