SINGAPORE: 2026 GDP Forecast Upgrade Adds To MAS Tightening Risks

The final Q4 GDP print for Singapore saw y/y upward revisions to 6.9% (initial estimate was 5.7%, while the market forecast was 6.5%). In q/q terms we printed 2.1%, against an initial 1.9% outcome, but this was below the 2.6% market consensus. Full year growth was 5.0%, after a 4.4% outcome for 2024. The authorities have raised the 2026 growth forecast to 2-4% from 1-3%. Today's outcomes will likely add, at the margin, to market tightening expectations for the MAS in H1 2026.

- The consensus expectation is for growth to be 2.7% in 2026. The past decade has seen annual growth average just over 3.3%.

- The detail for the Q4 print showed very strong conditions in manufacturing, 18.8%y/y, while all sub-industry categories saw positive y/y growth. In q/q terms, retail and transport saw modest falls (after gains in Q3). Manufacturing rose 8.4% in q/q terms, while finance gained 5.4%.

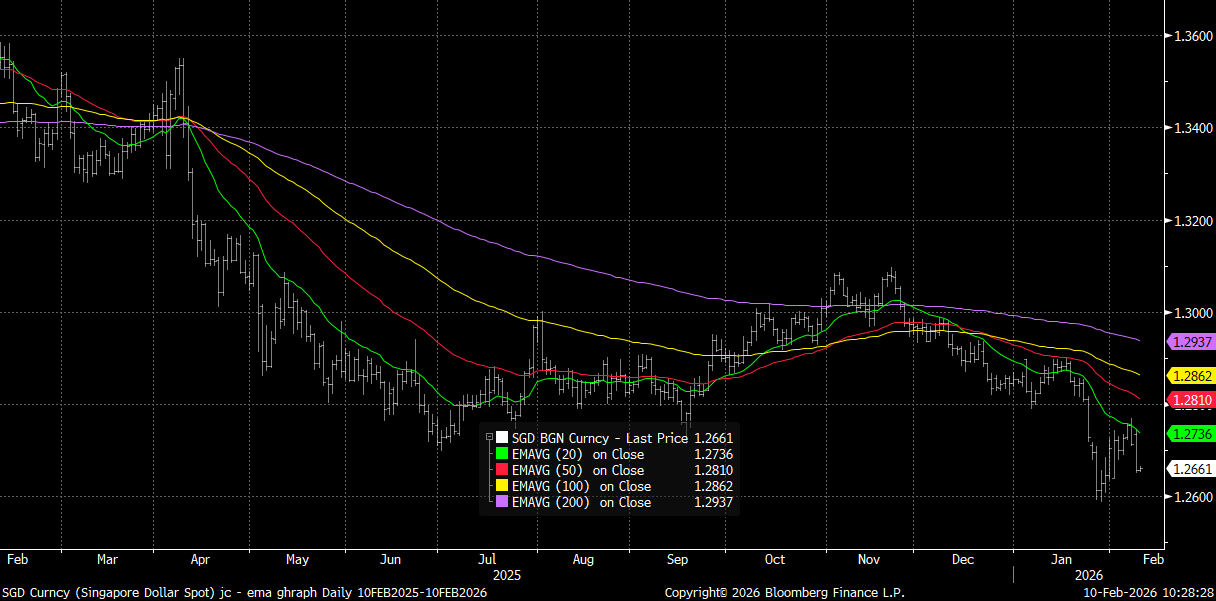

- For USD/SGD (currently near 1.2660), broader downside risks prevail, with moves towards the 20-day EMA capping the upside for now (around 1.2735/40), see the chart below. Downside focus will be on retest under 1.2600, which marked late Jan lows. Broader risk trends look more stable, albeit with a slightly softer start in Tuesday trade.

- The SGD NEER is around -0.38% from the top end of the band, per Goldman Sachs estimates. Given MAS tightening risks, dips are likely to remain supported for this index.

Fig 1: USD/SGD Versus Key EMAs

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 3-YEAR TECHS: (H6) Recovery Mode

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 95.890 @ 16:40 GMT Jan 9

- SUP 1: 95.740 - Low Dec 22

- SUP 2: 95.480 - Low 1st Nov ‘23

- SUP 3: 94.932 - 1.0% 10-dma envelope

Prices bounced again Thursday, supported by strength in global bond markets and a smoother inflation picture at the December CPI print. As such, prices edged further away from recent lows. Nonetheless, slower pricing for additional RBA easing - and partial pricing for a return to rate hikes in 2026 - should keep the front-end of the curve under pressure. This keeps prices well below prior resistance at 96.615, the Sep 12 high, and refocuses attention on 95.480 as the next major support.

MNI: MNI TEST 02, Please Ignore

Test Test TEST

MNI: MNI Test, Please Ignore

Test, ignore