US TSYS: 10-Yr Yields Eye 4.30% as Data Releases Ignored

A familiar theme played out each day this week for USTs trading in Asia. Modest decline in yields during the morning session - as investors took profit on overnight positions and locked in the rise in yields - followed by a resumption of higher yields in the afternoon.

The momentum for higher yields is strong. The US 10-Yr is higher on the week by +12.2bps - easily trading through 4.20%. Barring a sea change in the Iran war - there appears no barrier to the 10-Yr reaching 4.30% in the short term as the inflationary pressures intensify.

- The 2-Yr is down Friday by -1.1bps at 3.736% (+17.2bps for the week)

- The 5-Yr is down -0.5bps at 3.863% (+13.6bps for the week)

- The 10-Yr is flat at 4.263% (+12.2bps for the week)

- The 30-Yr is up +0.7bps at 4.893% (+13.2bps for the week)

US treasury futures are up modestly Friday with the 10-Yr at 111-16+ for gains of +03+ (-0-29+ for the week)

Looking ahead to Friday: Decent amount of data though investors focus will likely remain on Oil

- Personal Income (0.3%, 0.5%), Spending (0.4%, 0.3%)

- PCE Price Index MoM (0.4%, 0.3%), YoY (2.9%, 2.9%)

- Core PCE Price Index MoM (0.4%, 0.4%), YoY (3.0%, 3.1%)

- Personal Consumption (2.4%, 2.4%)

- Durable Goods Orders (-1.4%, 1.1%)

- Cap Goods Orders Non def Ex Air (0.8%, 0.5%), Ship (1.0%, 0.5%)

- GDP Annualized QoQ (1.4%, 1.4%), GDP Price Index (3.6%, 3.6%)

- U. of Mich. Sentiment (56.6, 54.6)

- U. of Mich. 1 Yr Inflation (3.4%, 3.7%), 5-10 Yr Inflation (3.3%, 3.4%)

- JOLTS Job Openings (6.542M, 6.750M), Quits Level (3.204M, 3.109M)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Cash Closed, Risks of Better NFP Not Priced

With Japan closed, it was only futures that traded today with volumes low. The 10-Yr traded in a range of 112-15+ to 112-19, finishing at the top end of the range for a gain of +02 today.

Its a big day Wednesday for data given the delayed Non Farm Payrolls and various Fed Speakers.

US Data/Speaker Calendar (prior, estimate). All times ET

02/11 0700 MBA Mortgage Applications (-8.9%, --)

02/11 0830 Change in Nonfarm Payrolls (50k, 67k)

02/11 1000 KC Fed Schmid moderated discussion on economy, mon-pol

02/11 1015 Fed VC Bowman moderated discussion

02/11 1130 US Tsy $69B 17W bill auction

02/11 1300 US Tsy $42B 10Y Note auction (91282CPZ8)

02/11 1400 Federal Budget Balance (-$144.7B, -$94.4B)

02/11 1600 Cleveland Fed Hammack on leadership (no text, Q&A)

Source: Bloomberg Finance L.P. / MNI

- There is a US$69bn 17-week and a US$42bn 10-Yr auction tonight

Yields have fallen more than expected in recent days, taking them back below the mid point of the 1 m range. The data suggests the economy is slowing (as evidenced by the recent peak in GDPNow) and yields should be lower. However the risks are now (given recent moves) that NFP in line or marginally stronger could see a modest unwind of the recent rally.

ASIA STOCKS: Positive Bias Continues on JN / AI Optimism; Eyes on NFP

- Despite Japanese markets closed today, optimism from the PM's recent landslide victory continued to provide a supportive regional backdrop. The day’s primary driver was cooling U.S. retail sales. This raised expectations for Federal Reserve rate cuts later this year, boosting risk appetite across the region. Markets look ahead tonight to non farm payrolls for further indications for rates with Trump talking up NFP prospects, whilst FED officials suggest rates are on hold for some time.

- China's CPI for January missed expectations whilst the PPI remained in contraction, though base effects were strong. While this underscored weak domestic demand, it also increased expectations for further stimulus from Beijing to hit its 2026 growth target. Moves in China's major bourses were muted today with HSI up +0.4% whilst CSI 300 was down -0.15%

- The KOSPI and TAIEX - both considered tech heavy - were higher today with the TAIEX up +1.6% on TSMC gains of +2.4% and the KOSPI up +1.2% despite a mixed day for AI stocks. Despite recent global volatility in tech valuations, Asian tech hubs like South Korea and Taiwan remain well supported by global investors with recent days seeing in a surge of inflows into Taiwan stocks.

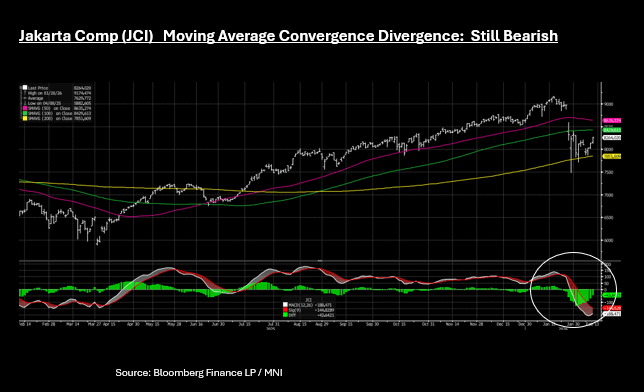

- The JCI has delivered three consecutive days of strong gains, up +1.6% today at 8,270; near to the upside resistance via the 100-day EMA at 8,359. Momentum indicators remain bearish for the JCI with the MACD line below the signal. A negative MACD value means the 12-day Exponential Moving Average (EMA) is significantly below the 26-day EMA.

FOREX: USD - BBDXY Testing 1175-1180 Into Employment Data

The BBDXY has had a range today of 1179.42 - 1183.25 in the Asia-Pac session; it is currently trading around 1179, -0.25%. The USD has fallen below most short-term supports and is looking to the lows seen in January now. It does not take a lot for the sellers to come back to market as nobody wants to miss out on this trade. The break lower in US yields is just adding to the USD headwinds and the market will be bracing for more bad news from the employment data tonight. On the day, the first resistance is toward the 1185-1187 area and then 1195 where I suspect we could see sellers return. A sustained break below 1175-1180 could potentially signal the start of another leg lower targeting 1150 first and then potentially 1115.

- EUR/USD - Asian range 1.1886-1.1915, Asia is currently trading 1.1915. The pair is consolidating around 1.1900 as the USD comes back under pressure and we await US employment data tonight. Price action has been pretty constructive after the initial sell-off and the support just below 1.1800 proved to be solid, can it now build some momentum from that base ? On the day, the first support is back toward the 1.1860-1.1890 area and then 1.1770-1.1800.

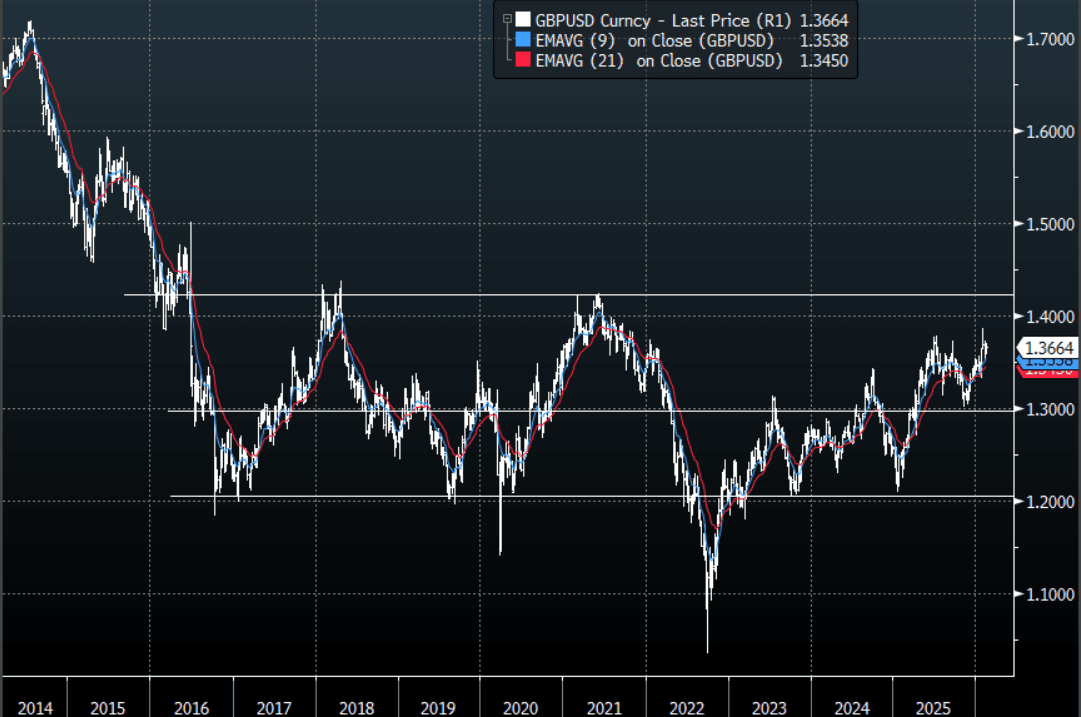

- GBP/USD - Asian range 1.3632-1.3670, Asia is currently dealing around 1.3665. The pair like everything is trying to bounce as the USD struggles. GBP looks like 1.3580-1.3730 to me for now as we wait to see if the big USD could potentially break lower. Should this play out then a move back above 1.4000 is back on the cards.

- Cross asset : SPX +0.30%, Gold $5057, US 10-Year 4.14%, BBDXY 1179, Crude Oil $64.48

- Data/Events : Italy Industrial Production

Fig 1: GBP/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P