GLOBAL: Worsening Outlook Leaves EM Cyclical Stocks Vulnerable

Executive summary

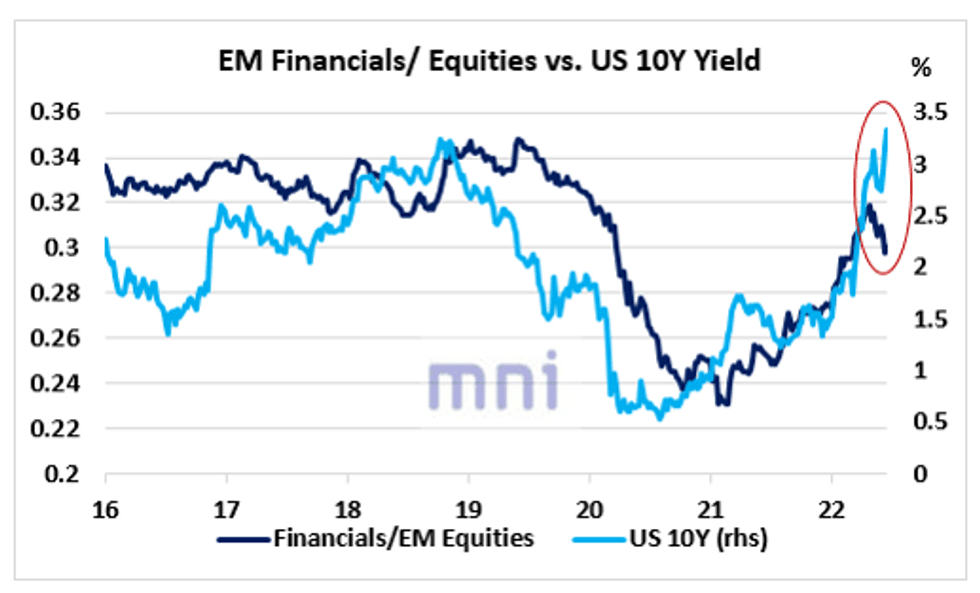

- Even though selling pressure on LT government bonds remain elevated (i.e. LT bond yields are surging), EM financials have been underperforming the market in recent weeks as global outlook worsens.

- In addition, the fall in China real M1 (in 2021) has been pricing in ‘cheaper’ financials for months.

- Hence, as the global outlook is not about to change anytime soon, the ‘cheap’ EM cyclical sectors may continue to underperform in the near term and defensive allocation should continue to be investors key allocation in the coming months.

EM Financials Underperform As Economic Slowdown Accelerates

The significant liquidity injections following the Covid shock combined with the surge in ST and LT bond yields had been a strong driver of EM financial stocks until the Ukraine invasion.

However, we mentioned after the start of the war in the end of February that the momentum on cyclical stocks was clearly unsustainable as the economic outlook was set to worsen considerably. The chart below shows that even though selling pressure on LT government bonds remain elevated (i.e. LT bond yields continue to surge), EM financials have been underperforming the market in recent weeks.

Source: Bloomberg/MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JPY: Yen Weakness Persists Amid Reduced Demand For Havens

USD/JPY managed to trim its weekly decline on Friday amid a rebound in U.S. equity markets. Positive sentiment has carried over into the first Asia-Pac session of this week, reinforced by a mortgage rate cut in China (to a new low of 4.40%, for first home buyers) and partial relaxation of COVID-19 countermeasures.

- In the wake of Friday's upswing, USD/JPY 3-month 25 delta risk reversals sits around 0.46 vol, though puts are still favoured over calls. Other tenors moved in similar fashion.

- Spot USD/JPY trades at Y129.49, up 27 pips on the day, with bulls looking for further gains towards May 9 high of Y131.35. Bears would be pleased by a dip through May 12 low of Y127.52, which would expose Apr 27 low of Y126.95.

- Note that the weekend saw Nikkei sources report that the Japanese government will use deficit-financing bonds to cover Y2.7tn of extra spending under a supplementary budget, as it looks to shield consumers and businesses from the well-documented global inflationary pressures.

- Worth noting that BoJ Gov Kuroda will speak in parliament later today.

- Japan's flash GDP figures headline the local data docket this week and will hit the wires on Wednesday, with final industrial output due on the same day. Looking further afield, trade balance & national CPI will be published on Thursday and Friday respectively.

EQUITIES: E-Minis Bid On China +ves, Follow Through Above Friday’s Peak Limited

The previously outlined risk-friendly China-centric headlines, namely the latest measures to support the country’s property market and confirmation that Shanghai’s gradual re-opening will get underway today, have dominated price action in early Asia-Pac trade. This has allowed S&P 500 e-minis to have a look above Friday’s highs, last dealing +0.5%, although follow through has been rather limited thus far, with the spectre of the recent stagflation worry-driven sell off and wider geopolitical worry still looming large. Technically, the next level of interest on the upside is located at the May 9 high (4,099.00). Meanwhile, key resistance is some way away, defined at the Apr 26/28 highs (4303.50).

JGBS: Futures Little Changed Overnight, Plenty To Weigh Up At Tokyo Re-open

JGB futures recovered from worst levels of post-Tokyo trade during last week’s final session of overnight dealing, finishing -1 vs. Tokyo settlement, although some modest early weakness in U.S. Tsys this week, coupled with reaction to Friday’s bear steepening of the U.S. curve, may provide some pressure.

- Conversely, Friday’s JGB trade saw the curve bull flatten, with some flagging potential re: lifers deploying capital in the super long end.

- Note that the weekend saw Nikkei sources report that the Japanese government will use deficit-financing bonds to cover Y2.7tn of extra spending under a supplementary budget, as it looks to shield consumers and businesses from the well-documented global inflationary pressures. The article suggested that the government plans to formally decide on the spending decision on Monday, with a view to the stimulus being passed in the current parliamentary session.

- PPI & machine tool orders headline the domestic data docket on Monday, with 10-Year JGBi due on the supply side.