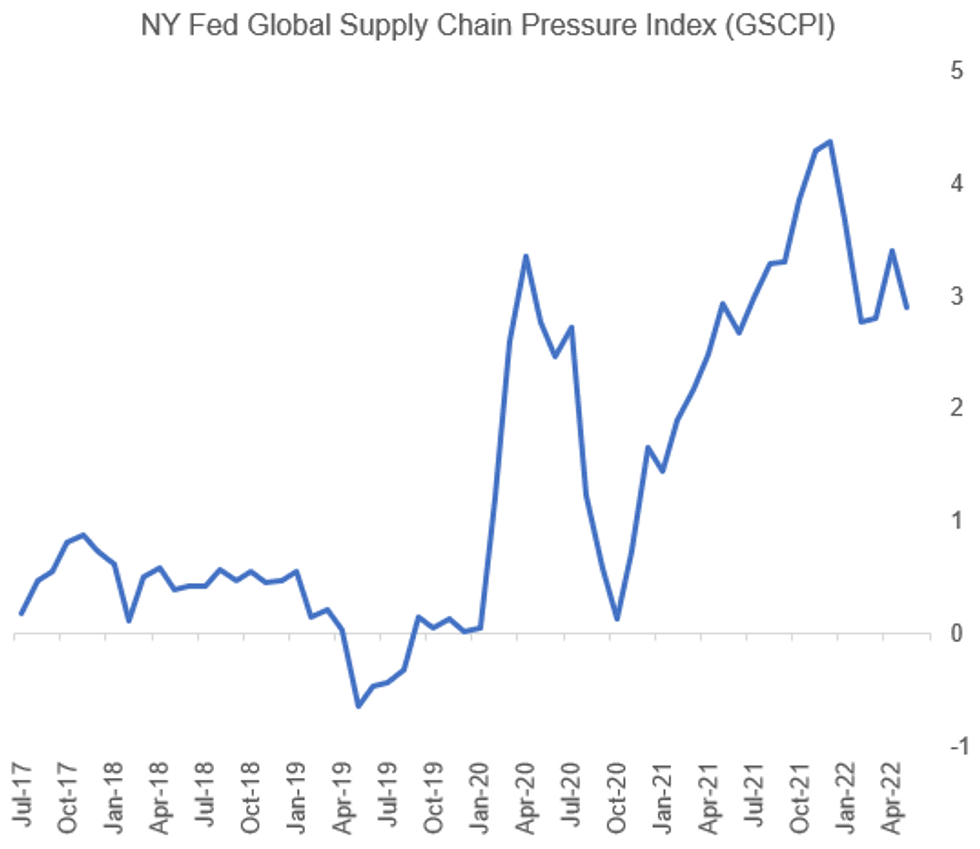

GLOBAL: Supply Chain Pressures Stabilizing At Problematic Levels

The NY Fed's Global Supply Chain Pressure Index (GSCPI) suggests global bottlenecks eased slightly in May to 2.90, reversing most of the tightening seen in April (3.40, which was up from 2.80 in both Feb and Mar).

- The majority of the components in the GSCPI eased in May.

- The NY Fed's overall view is that global supply chain pressures have stabilized "at historically high levels" over the past 3 months.

- The reading suggests little relief for inflation-boosting/growth-suppressing supply chain issues, with Chinese lockdowns a major factor.

Source: NY Fed, MNI

Source: NY Fed, MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Yield Curves Bear Steepen, Focus on Fed over Jobs Data

Yield curves continued to bear steepen Friday, 2s10s session high of 43.067 back to early March levels as bond yields climbed to 3.2338% high -- last seen early December 2018. Relative calm end to the week for a NFP session.

- Tsy futures bounced higher briefly, scaled back amid steady selling after Apr NFP jobs gained more than estimated +428k vs. +380k est, avg hourly earning little weaker than exp at 0.3% vs. 0.4% est. Total down-revisions to Feb-Mar -39k.

- Fed out of blackout: limited react to essay published by Minneapolis Fed Pres Kashkari: Long-Term Real Rates Are Already Back To Neutral. ""If the economy is in fact in a higher-pressure equilibrium, that might indicate the neutral long-term real rate has increased, which would then require even higher rates to reach a contractionary stance that would bring the economy into balance."

- MNI interview w/ Richmond Fed Barkin: interest rate increases are not on a preset course and he would like to see interest rates on a path to normal that is as fast as feasible, backing this week's historic FOMC decision to raise the fed funds rate 50bps, while not ruling out the potential for a supersized 75bp increase if needed.

US: Late Corporate Credit Update: Back Near 2Y Highs Late

Investment-grade corporate credit risk has see-sawed back near new 2Y highs tapped early Friday, closing levels well off midday lows as stocks traded modestly weaker: S&P E-Mini Future down 30.25 points (-0.73%) at 4113.75

- Investment grade risk measured by Markit's CDXIG5 index currently +3.464 at 86.919 vs. new 2Y high of 87.321 around midmorning; CDXHY5 high yield index at 100.813 (-0.837).

- Outperforming credit sectors (tighter or least wide): Financials - subordinated (-0.2) followed by Energy (+0.4).

- Lagging sectors (wider or least narrow): Utilities (+1.4) followed by Technology and Consumer Discretionary (+1.3).

US STOCKS: Late Equity Roundup: Mildly Lower on Week

Equity indexes weaker into the close are off session lows, upper half of range SPX emini futures, ESM2 currently -30.25 points (-0.73%) at 4113.75 -- near week opener of 4146.25.

- Earnings cycle past the halfway mark, resumes Monday w/ Duke Energy (DUK), Tyson (TSN) before the open, Trex (TREX), Int Flavor/Fragrances (IFF), Cargurus (CARG) after the close.

- SPX leading/lagging sectors: Energy sector extends earlier gains (+2.91%) O&G consumables outpacing energy and equipment serving names. Utilities sector follows (+0.81%). Laggers: Materials sector holding near lows (-1.40%) w/ construction materials shares lagging; Communications sector (-1.30%).

- Meanwhile, Dow Industrials currently trades -97.15 points (-0.29%) at 32901.08, Nasdaq -173 points (-1.4%) at 12144.66.

- Dow Industrials Leaders/Laggers: United Health outperforms (UNH) +5.10 at 499.82, Chevron (CVX) +4.00 at 170.26. Laggers: Home Depot (HD) continues to sag -4.47 at 294.64, Nike (NKE) -3.62 at 115.01.