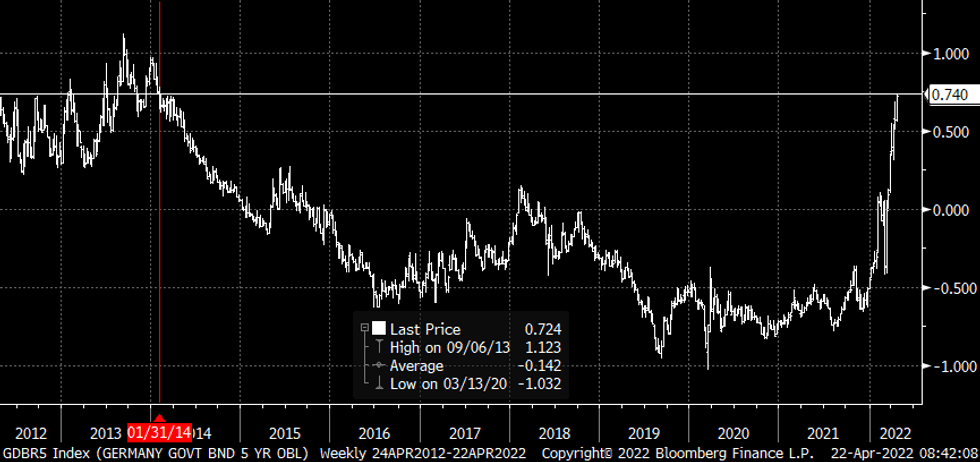

BUNDS: German 5yr Yield highest since January 2014

Apr-22 07:48

Another beat for German services PMIs, following on the decent French PMI beat.

- Short term rate (Euribor), Sep 22 and the whole strip is through support and test session lows across the board.

- Short end Govies 2yr (Schatz) and 5yr (Bobl) test new multi year yield highs at 0.75% for Bobl.

- German 5yr Yield is now highest since 31/01/14.

- Looking further out, reference 126.85:

- 0.75% = 126.74

- 0.80% = 126.45

- 1.00% = 125.27

Chart source: MNI/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

What to watch

Mar-23 07:48

It was a fairly benign overnight session with core fixed income continuing to drift lower and hitting new cycle highs in terms of yields.

- The main focus today will be on the UK with Chancellor Sunak due to deliver the Spring Statement (mini-budget) and the DMO due to announce the gilt remit for the 22/23 fiscal year. From reading through 12 GEMM previews, we see the median expectation of gilt sales at GBP153.5bln with estimates ranging from GBP124.5bln to GBP211.2bln. For our full preview see here. The Chancellor's speech is due to begin around 12:30GMT with the full OBR forecasts and gilt remit released shortly after his speech concludes (normally about an hour later). The DMO will then release the agenda of its FQ1 GEMM / investor consultation at 15:30GMT.

- Elsewhere we have a number of central bankers speaking. At the BIS Innovation Summit we have a panel consisting of Fed's Powell, BOE's Bailey and ECB's Nagel at midday GMT (monpol probably won't be discused) while we also have ECB's Visco and Fed's Daly and Bullard due.

- We have already had UK CPI data this morning which was higher than economists expected, but the 0.2ppt increase was largely in line with market expectations, marking the 5th consecutive upside surprise to consensus. US new home sales are the only other notable data release of the day.

USD: USDJPY fades off the overnight high

Mar-23 07:34

- Another painful session for the Yen, albeit off its worst level against the USD, with selling going through in Equity futures since the Bund cash open.

- Next decent area of interest for the USDJPY is at 121.49/121.69, the February and January 2016 peaks respectively.

- USD remains on the front foot, up against all G10s besides the Pound.

- But on the margin, the USD is circa flat, versus the GBP, NOK, EUR, CAD, and the SEK in early European trade

UK DATA: Feb Inflation Numbers Above Analyst Consensus

Mar-23 07:34

UK FEB CPI +0.8% M/M (forecast: +0.6%), +6.2% Y/Y (forecast: +6.0%)

CORE CPI +0.8% M/M, +5.2% Y/Y (forecast: +5.0%)

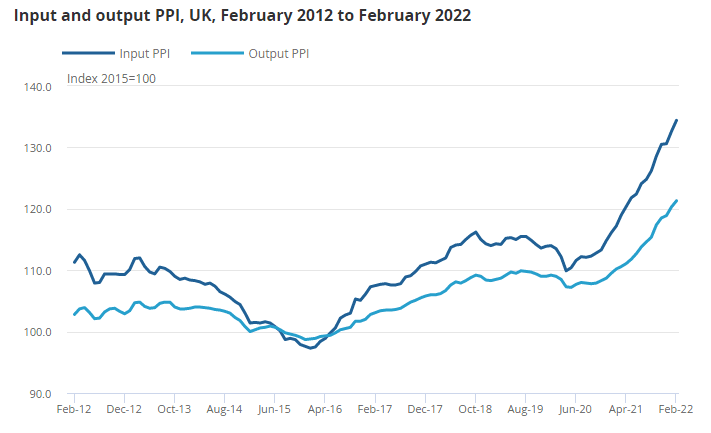

OUTPUT PPI +0.8% M/M (forecast: +0.9%), +10.1% Y/Y

INPUT PPI +1.4% M/M (forecast: +1.2%), +14.7% Y/Y (forecast: +13.9%)

- UK consumer price inflation rose to 6.2% year-on-year in February, the highest level since the latest series began in 1997 and the highest since March 1992 in a historically modelled series, when it stood at 7.1%.according to the ONS.

- Feb was up from 5.5% in February and above Bank of England expectations.

- In February, CPI rose by 0.8% m/m, compared with a rise of 0.1% in the same month last year. This was the largest monthly CPI increase between January and February since 2009.

- Factory gate inflation also rose sharply, underlining just how embedded inflation is becoming in the supply chain, with the headline rate of output prices showed positive growth of 10.1% on the year to February 2022, up from 9.9% in January 2022.

- The headline rate of input prices showed positive growth of 14.7% on the year to February 2022, up from 14.2% in January 2022. Food products and metals and non-metallic minerals provided the largest upward contributions to the annual rates of output and input inflation, respectively.

Source: ONS