EU CREDIT UPDATE: ZKB €500m WNG 6NC5 Bail-in - Final Terms

Sep-04 11:23

- FT: MS+83

- Books > €2.4bn up from €2bn at guidance

- Guidance: MS+85 (+/-2bps WPIR)

- IPT: MS+105

- FV: MS+73

- Exp Rating: Aa2

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

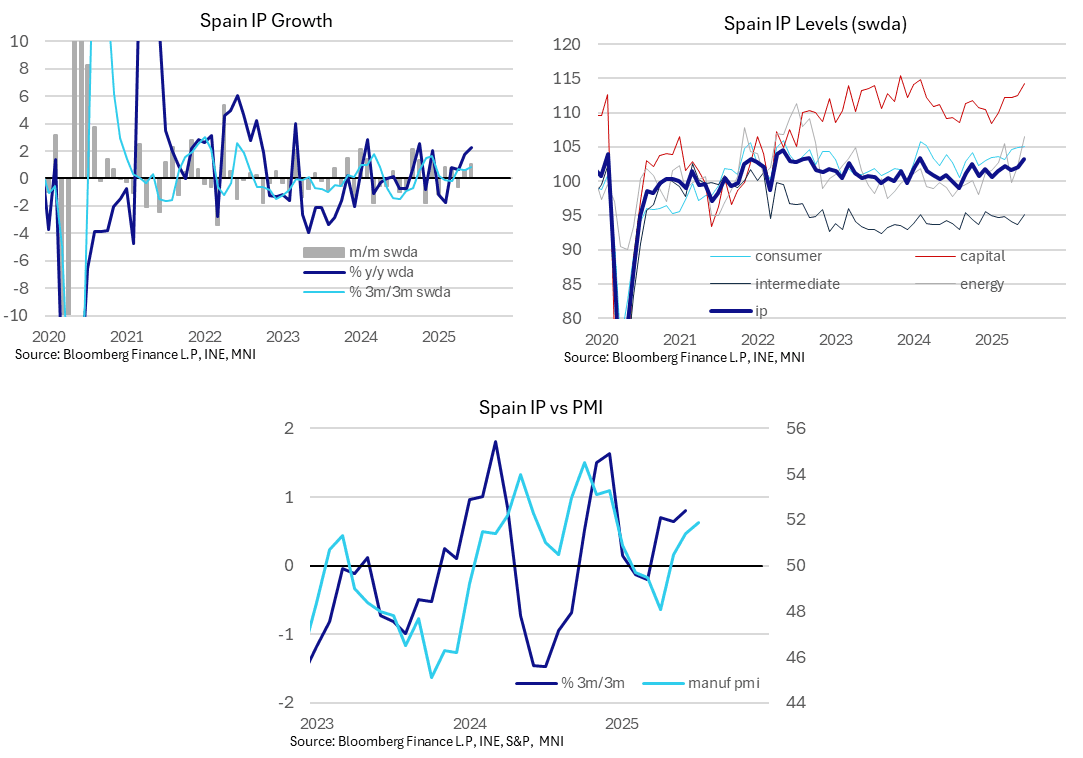

SPAIN DATA: Strong Headline IP Growth In June

Aug-05 11:16

Spanish headline IP rose 1.0% M/M in June, above the four-analyst strong consensus of -0.1% (range: -0.8% to +0.5%) and +0.5% prior (from 0.6% initial).

- 3m/3m IP growth was 0.8%, the highest rate since December 2024 and above May's 0.6% and April's 0.7%.

- While recent IP strength is consistent with expansionary PMI data, the July manufacturing PMI report did note a softening in confidence amongst Spanish producers due to "uncertainty in global markets and the hard to predict outlook for the world economy, especially in relation to trade".

- In June, there was a 1.5% M/M rise in capital goods production, with intermediate goods rising 1.4%. Energy posted a 4.3% M/M increase (vs 2.2% prior), while consumer goods production was softer at 0.1% M/M.

BUNDS: BTP/Bund spread extends below 80.00bps

Aug-05 10:50

- BTP/Bund is just 0.6bp tighter, but it is clearing the Psychological 80.00bps Mark, now trading at 79.4bps.

- Technically, noted multiple times of late, that looking at that longer term chart, aside from the April 2010 low situated at ~75.4bps, the next big support resides at 65.37bps, the 2009 low.

US TSYS: Modestly Lower But Rangebound, ISM Services And 3Y Supply In Focus

Aug-05 10:47

- Treasuries are modestly lower across the curve but continue to hold a relatively narrow range seen since Friday’s nonfarm payrolls and less so ISM manufacturing reports were digested.

- Moves have been aided by equity futures consolidating yesterday's strong gains.

- Today’s focus should be on ISM services with sensitivity to further downside surprises whilst 3Y supply will be watched closely. There’s little scheduled for President Trump today, signing an executive order at 1600ET, but markets will be on watch for any potential contenders for Fed Governor Kugler’s position and the new BLS commissioner.

- Cash yields are 1.5-2.5bp higher on the day, with increases led by the front end.

- 2Y yields, currently at 3.6996%, appear to have found some support at 3.65% in the post-payrolls period, with a low of 3.655% with Monday’s Asia open. They last traded below this level in late April/very early May.

- TYU5 trades at 112-09 (-03), easing back from an overnight high for a second day running albeit at a slower pace today. Cumulative volumes are low at 230k.

- The latest high of 112-15+ more comfortably cleared resistance at a bull trigger of 112-12+ (Jul 1 high) and briefly 112-15 (61.8% retrace of Apr 7-11 sell-off). A firmer break could open 112-23 (May 1 high).

- Data: Trade balance Jun (0830ET), S&P Global US serv/comp PMI Jul final (0945ET), ISM services Jul (1000ET)

- Fedspeak: None scheduled

- Coupon issuance: US Tsy $58B 3Y Note auction - 91282CNU1 (1300ET)

- Bill issuance: US Tsy $85B 6W & $50B 52W bill auctions (1130ET)