AUSSIE 10-YEAR TECHS: (Z5) Bull Cycle Remains Intact

- RES 3: 95.995 - 1.618 proj of the Sep 3 - 9 - 10 price swing

- RES 2: 95.865 - 1.000 proj of the Sep 3 - 9 - 10 price swing

- RES 1: 95.780 - High Sep 12, 18 and 19

- PRICE: 95.705 @ 20:03 BST Sep 19

- SUP 1: 95.510 - Low Sep 3

- SUP 2: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 3: 95.275 - Low Nov 14 (cont) and a key support

A short-term bull cycle in Aussie 10-yr futures remains in play. Near-term resistance to watch is 95.780 high, the Sep 12 high. A clear break of this level would signal scope for a continuation higher and pave the way for a climb towards 95.865, a Fibonacci projection. On the downside, key short-term support has been defined at 95.510, the Sep 3 low. Clearance of this level would instead be bearish.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

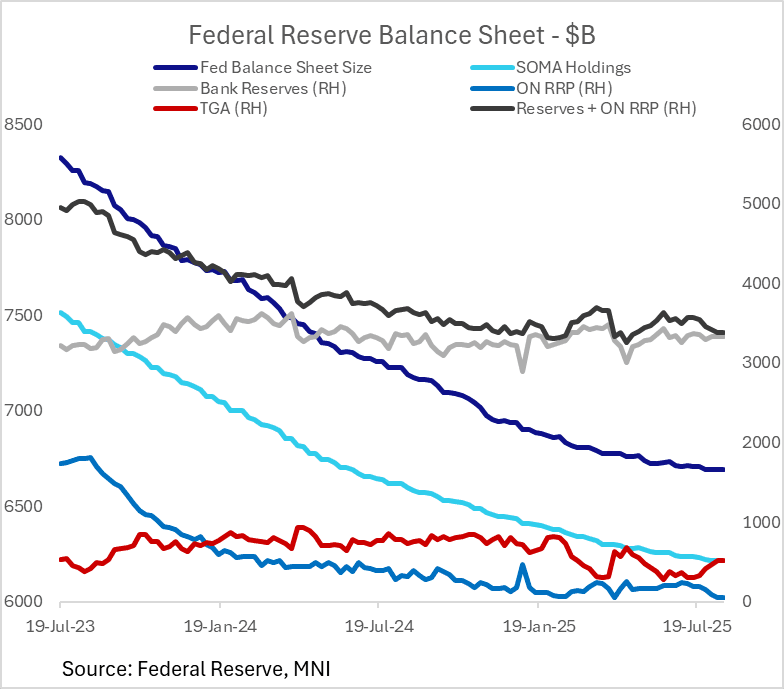

FED: July FOMC Minutes: Reserves "Abundant", Quarter-End SRF Takeup Eyed (3/3)

The July meeting devoted some discussion to the ongoing drawdown in reserves amid the Treasury cash rebuild. Overall, the Committee seem to be comfortable with the trajectory of reserves, despite some caution that reserves could be headed into "ample" from the current "abundant" territory.

- With regard to near-term funding pressures, namely potential for the mid-September tax date and Q3 quarter-end posing risks, the minutes suggest that while there may be some temporary acute liquidity issues, they can be resolved by takeup of the standing repo facility.

- As such, there was no real discussion of a shift in balance sheet management policy, particularly with QT proceeding "smoothly" and rerserves remaining "abundant", though vigilance of money market conditions would continue to be important.

- SOMA Manager Perli: "Market indicators continued to suggest that reserves remained abundant; however, ongoing System Open Market Account (SOMA) portfolio runoff, a substantial expected increase in the TGA balance, and the depletion of the ON RRP facility were together likely to bring about a sustained decline in reserves for the first time since portfolio runoff started in June 2022. Against this backdrop, the staff would continue to monitor indicators of reserve conditions closely. The manager also noted that there would be times—such as quarter-ends, tax dates, and days associated with large settlements of Treasury securities—when reserves were likely to dip temporarily to even lower levels. At those times, utilization of the SRF would likely support the smooth functioning of money markets and the implementation of monetary policy."

- And the broader FOMC: "Several participants remarked on issues related to the Federal Reserve's balance sheet. Of those who commented, participants observed that balance sheet reduction had been proceeding smoothly thus far and that various indicators pointed to reserves being abundant. They agreed that, with reserves projected to decline amid the rebuilding of the TGA balance following the resolution of the debt limit situation, it was important to monitor money market conditions closely and to continue to evaluate how close reserves were to their ample level. A few participants also assessed that, in this environment, abrupt further declines in reserves could occur on key reporting and payment flow days. They noted that, if such events created pressures in money markets, the Federal Reserve's existing tools would help supply additional reserves and keep the effective federal funds rate within the target range. A couple of participants highlighted the role of the SRF in monetary policy implementation—as reflected in increased usage at the June quarter-end—and expressed support for further study of the possibility of central clearing of the SRF to enhance its effectiveness."

SOFR OPTIONS: BLOCK: Mar'26 SOFR Call Spread

- 5,000 SFRH6 96.25/97.25 call spds, 26.5 at 1504:25ET

- This after scale buyer over 50,000 SFRH6 97.25 calls, from 6.0-6.5 covered

FED: July FOMC Minutes: Little Concern Over Labor Market; Rates (2/3)

At the same time, the July minutes suggested labor market concerns were relatively muted for most on the FOMC: "participants observed that the unemployment rate remained low and that employment was at or near estimates of maximum employment".

- To be sure, "regarding the outlook for the labor market, some participants mentioned indicators that could suggest a softening in labor demand" and "a number of participants noted that softness in aggregate demand and economic activity may translate into weaker labor market conditions, as could a potential inability of some importers to withstand higher tariffs."

- But there was no panic evident in the minutes, and "some participants" noted (in line with comments by Powell and others) "that slower output or employment growth was not necessarily indicative of emerging economic slack because a decline in immigration was lowering both actual and potential output growth as well as reducing both actual payroll growth and the number of new jobs needed to keep the unemployment rate stable."

- The weak July employment data released 2 days after this meeting are seen as a key reason to expect a September cut, so that's an important line of reasoning that - if repeated by Chair Powell on Friday - could signal that it will take more conclusive evidence of labor market deterioration for a majority to decide on a rate cut.

- On that front, the minutes repeated the June minutes' line that "several participants commented that the current target range for the federal funds rate may not be far above its neutral level", and noted that "almost all participants agreed that, with the labor market still solid and current monetary policy moderately or modestly restrictive, the Committee was well positioned to respond in a timely way to potential economic developments."

- We had wondered whether the minutes would include any insight at all on rate cut timing, though here the language was as vague as expected, pointing to potential for an informed assessment of the tariff situation to be made in the coming months. Participants "noted that it would take time to have more clarity on the magnitude and persistence of higher tariffs' effects on inflation. Even so, some participants emphasized that a great deal could be learned in coming months from incoming data, helping to inform their assessment of the balance of risks and the appropriate setting of the federal funds rate; at the same time, some noted that it would not be feasible or appropriate to wait for complete clarity on the tariffs' effects on inflation before adjusting the stance of monetary policy."

- Echoing what Chair Powell has said, participants saw policy as well-positioned, allowing the Committee in the case of tariff-related inflation / expectation pressures to "maintain a more restrictive stance of monetary policy than would otherwise be the case, especially if labor market conditions remained solid". Though they could also "establish a less restrictive stance" "if labor market conditions were to weaken materially or if inflation were to come down further and inflation expectations remained well anchored". And as previously stated, were both sides of the dual mandate to be at risk simultaneously, participants would assess the distance of each from target and act accordingly.