EU UTILITIES: Week in Review

May-23 09:38

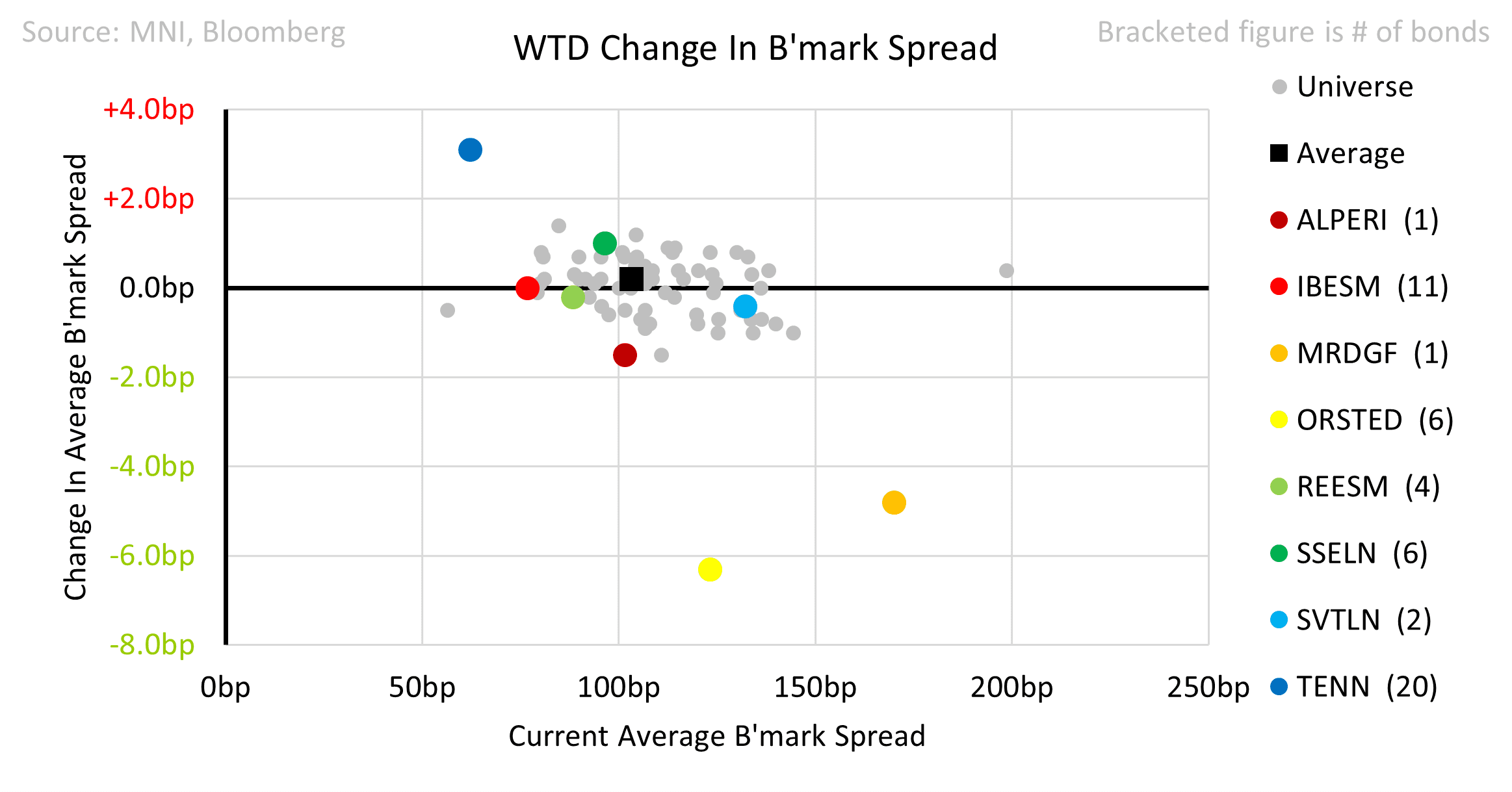

- Spreads were little changed on average this week, in-line with the market overall.

- Orsted received a sentiment boost as Equinor’s NY offshore wind project had its halt order lifted.

- SSE had in-line results and reduced its five-year investment plan by £3bn.

- Severn Trent reported a small beat.

- Iberdrola’s planned €5bn US farm down is reportedly in doubt.

- Red Electrica was out on outlook negative by Moody’s. It sees potential for increasing investments to strengthen the transmission network.

- Eurogrid priced a 12Y in-line with our FV.

Fluxys issued a 5.5Y 20bp wide to our FV and rallied 13bp on the break, albeit we expected a meaningful concession. Our credit overview noted strong credit metrics but a complex asset ownership structure.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GERMAN AUCTION RESULTS: Very soft 10-year Bund auction; still no futures impact

Apr-23 09:37

- Another German auction with soft demand - this time for a 10-year Bund.

- That was the smallest volume of bids for a 10-year Bund auction since October 2022.

- Some of this is expected as it is a smaller auction size (E4.0bln rather than the recent E4.5bln) but the bid-to-offer of 1.06x compares to 1.64x earlier this month and the bid-to-cover of 1.38x compares to 2.16x - so those metrics are weak too.

- Still not a big impact on Bund futures.

GILTS: Twist Flattening Holds, BoE Comments Eyed

Apr-23 09:33

Twist flattening has dominated on the gilt curve this morning, with 3 factors defining this morning’s price action:

- Spillover from Tsys after U.S. President Trump pushed back against the idea that he was looking to fire Fed Chair Powell, as well as some comments pointing to the potential for a moderation in the Sino-U.S. trade war.

- The DMO’s revised gilt remit surprising most by coming in marginally lower than the prior estimate, skewing issuance further away from the long end in the process (T-bill, short-dated and unallocated bucket issuance was revised higher, while long-end issuance was revised lower).

- Softer-than expected flash PMIs.

- Gilt futures broke through initial resistance at the open, with bulls now looking to pierce 93.00 before shifting focus to a Fibonacci retracement at 93.44. The contract last prints 92.80 vs. session highs of 92.95.

- Yields 3.5bp higher to 9bp lower.

- 2s10s ~13bp off cycle closing highs, last ~65.6bp.

- 5s30s ~11bp off yesterday’s cycle closing high, last 127.8bp.

- BoE-dated OIS covering ’25 meetings back to little changed on the day, showing 92bp of cuts through year-end, with the next 25bp step still fully discounted through the May meeting. Recent range extremes of ~97bp of cuts through year-end remains untested/intact.

- Comments from BoE’s Pill (11:30 BST), Bailey (18:15 BST) & Breeden (19:00 BST) due throughout the day.

GERMAN AUCTION RESULTS: 2.50% Feb-35 Bund

Apr-23 09:31

| 2.50% Feb-35 Bund | Previous | |

| ISIN | DE000BU2Z049 | |

| Total sold | E4bln | E4.5bln |

| Allotted | E3.049bln | E3.42bln |

| Avg yield | 2.47% | 2.68% |

| Bid-to-offer | 1.06x | 1.64x |

| Bid-to-cover | 1.38x | 2.16x |

| Avg Price | 100.25 | 98.45 |

| Low Price | 100.23 | 98.43 |

| Pre-auction mid | 100.230 | 98.434 |

| Previous date | 02-Apr-25 |