EU AUTOMOTIVE: Week in Review

OEMs still provide no guidance on tariff impact and their strategies remain undecided. They are cyclically exposed, and the Liberation Day debacle has brought yet another indirect headwind. Vehicle tariffs seem entrenched; we await possible concessions on parts.

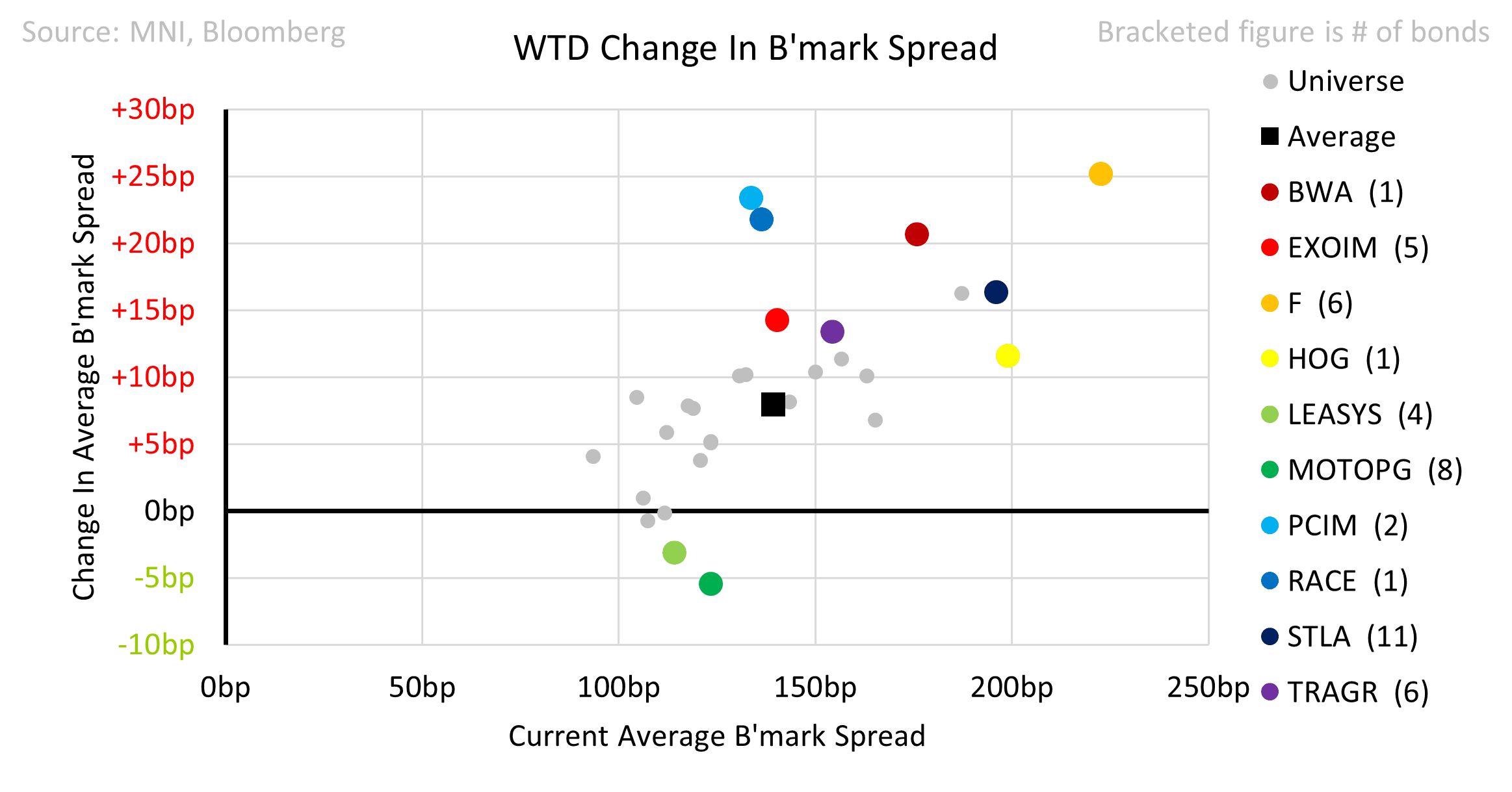

- Spreads underperformed at +8bp for the week. EXOIM (+15) almost kept pace with STLA which we find surprising.

- Continental is preparing for a sale of ContiTech. With Automotive already slated for a spinoff, this would improve margins further and potentially reduce proforma leverage.

- Volkswagen reported 1Q preliminaries, with adj. EBIT in line but higher-than-expected one-offs.

- Jaguar Land Rover flagged that it had met its net cash target when reporting its 4Q25 deliveries.

- BMW 1Q deliveries were marginally soft, with no signs of any improvement in Chinese demand. It flagged green shoots elsewhere.

- Traton 1Q preliminaries showed a weak start with a big adj. EBIT miss. It confirmed guidance, but tariffs remain an unquantified headwind.

- Stellantis 1Q deliveries disappointed, as it continues to try and put last year’s inventory problems behind it, signalling optimism from here. It reportedly hired McKinsey to look at options for the Maserati and Alfa Romeo brands.

- Harley-Davidson will part ways with its CEO and is reported to be looking at a sale of HDFS – the EUR issuing entity. The bonds have a 101 CoC which should cushion against adverse outcomes.

- Volkswagen was put on outlook negative by Fitch. It looks behind the curve following Moody’s downgrade last month which took it in line with S&P at high triple B.

Potential events we’re watching for: Autoliv and Forvia results; Nissan actions under its new CEO; Moody’s on Stellantis; UK benefits reform affecting Motability.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US DATA: Energy Services Pickup Offsets Sequential Food Disinflation

On the headline side of CPI, the pullback to 0.22% M/M from 0.47% in Jan came with lower than expected food price inflation (0.2% M/M vs 0.3% expected, 0.4% prior) offset by slightly less of a pullback in energy prices than expected (0.2% vs 0.0% expected, 1.1% prior).

- Within food, it was "food at home" (ie groceries) that was the main decelerator, rising 0.0% after 0.5% prior, with dairy and fruit/vegetables in sequential deflation (-1.0% and -0.5% respectively), and meats/poultry/fish/eggs decelerating to a still-high 1.6% (1.9% prior). Food away from home ticked up however to 0.4% after 0.2% prior.

- The closely-watched eggs category saw a 10.5% increase, a slight deceleration from 15.2% in January ( though it's now up 58.8% Y/Y).

- Within energy, motor fuel's 0.9% decline matched expectations, but a strong pickup in energy services (1.4% after 0.3%) led by acceleration in both electricity and gas led to the above-expected aggregate figure.

US DATA: Broadening In Inflation Depth In February

- MNI calculations suggest that 34% of the overall CPI basket increased at 3% Y/Y or higher in February, compared to 30% in January for the highest share since May 2024.

- It pushes it away from the 24% averaged in 2019 and 19% through 2015-19, with that historical wedge still firmly driven by services.

- Details suggest February’s uptick is a reasonably broad move. The same share specifically for core goods increased from 13% to 19% (highest since Apr 2024), whilst core services increased from 55% to 63% (highest since Nov 2024).

- These are volatile metrics, especially for core services recently, but they’re reasonable increases ahead of tariff implementation. Closer to 35% of the core services basket was running at or faster than 3% Y/Y in the years leading up to the pandemic.

- See the below charts for clearer context:

US DATA: Mixed Contributions Across Categories

The outsized downside contribution to the "miss" in core PCE was largely due to airfares - that alone shaved 0.05pp from core CPI (eg if it had been slightly positive as expected rather than -4.0%, core CPI would have come in roughly in line with expectations).

- We noted the pullback in shelter prices elsewhere, but housing and lodging combined resulted in "only" a -0.04pp swing in core CPI in Feb vs Jan, whereas car insurance and airfares contributed -0.12pp to the swing.

- In the table below, the swing higher in "other goods" was largely accounted for by apparel (2.5% of the CPI basket) flipping from -1.4% M/M in January to +0.6%; vehicle prices were relatively in line in terms of deceleration from January's outsized gains.

- One services category that didn't slow much from January was communications (3.1% of the CPI basket), rising 0.3% after 0.4%; we also note that medical care services (6.7% of CPI) accelerated to 0.3% M/M after 0.0% in January, led by professional services (+0.3% after -0.2%).