EU BASIC INDUSTRIES: Week in Review

Hoped-for infrastructure spending in Europe continues to support parts of the sector, particularly Defence names. Chemicals have mostly had a disappointing earnings season.

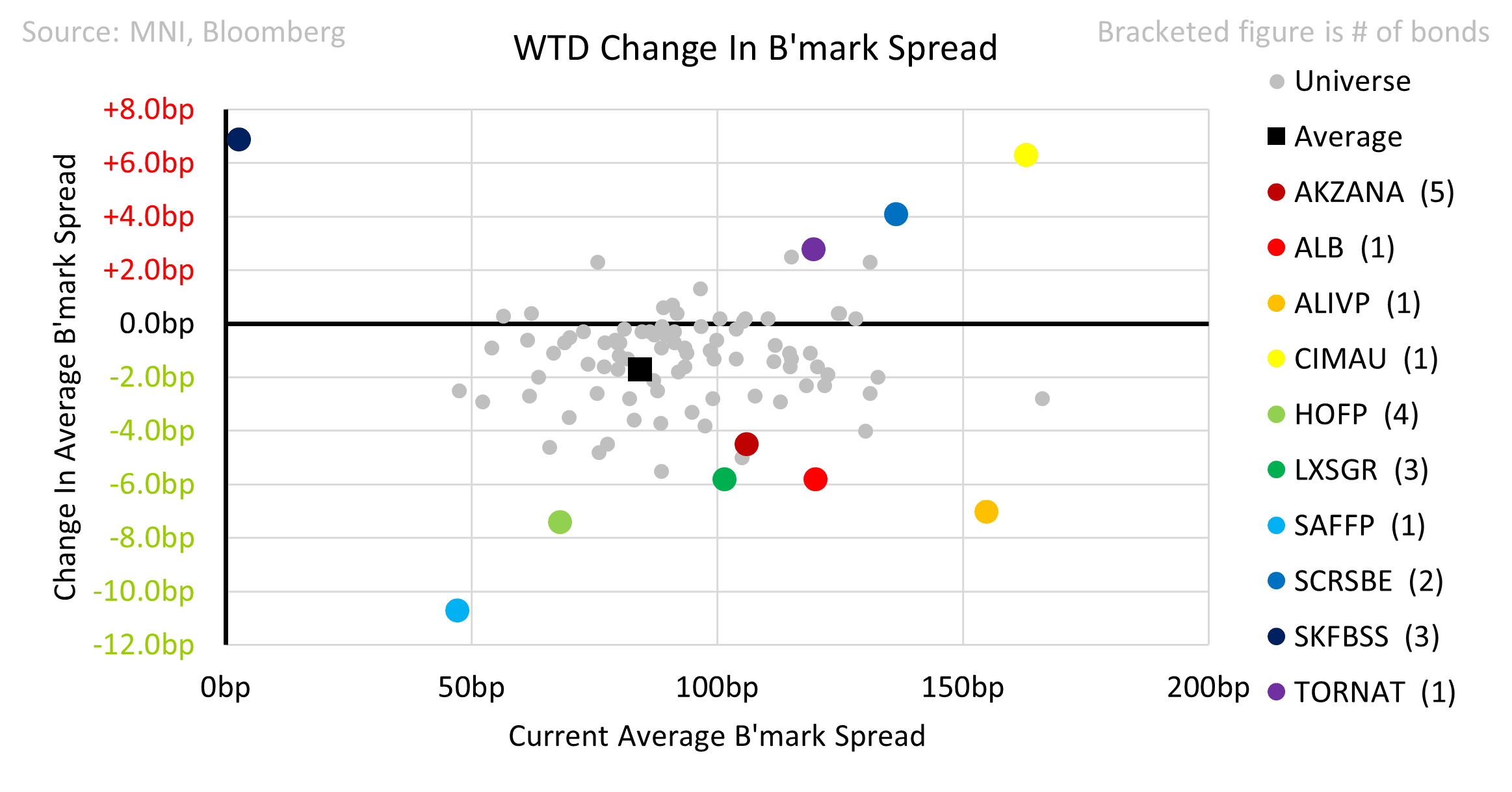

- Spreads outperformed marginally at -1.7bp on the week. Defence names SAFFP (-11) and HOFP (-7) did well.

- Lanxess reported 4Q24 results following a preliminary release in January. EBITDA guidance was soft. We have viewed credit metrics as stretched for some time; margins are well below threshold and even with a possible asset sale the required deleveraging could be out of reach.

- Following last week’s refinancing, Celanese gave a capital structure update. Leverage targets and IG ambitions were confirmed. As per the FY24 earnings call, it is actively pursuing divestments, a firming up of language since the downgrades. That may have motivated a change from a previously opportunistic approach and should be credit supportive.

Names to watch: Smiths Group 1H25 (25th); SKF next steps following failed consent solicitation aimed at avoiding an event of default; Stora Enso forest sales; Verallia takeover (CoC); BASF Agri IPO; Moody’s on Lanxess; Celanese asset sales.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB SYNDICATION: 15-year SlovGB: Final terms

- Size: E3bln (MNI expected E2.5-3.5bln)

- Books closed (pre-rec) in excess of E9bln (incl. E460mln JLM interest)

- Spread set earlier at MS+130bps (guidance was MS + 140bps area)

- Maturity: 27 February 2040

- Settlement: 27 February 2025 (T+6)

- ISIN: SK4000026845

- Bookrunners: HSBC (DM/B&D) / JPM / Slovenska sporitelna (Erste Group) / Tatra banka (RBI Group)

- Timing: Books closed at 12:00GMT / 13:00CET, allocations and pricing to follow

BUNDS: Looking at the German 10yr Yield

- With the Bund still under pressure today, the German supply initially weighted, followed by a Hawkish Schnabel, although nothing was too surprising from her, plus some short term long likely caught offside, the next key support is at the 131.00.

- BUT, Cash and Swap desks might also start looking at Yield levels, and if they could be on the toppish side around the 2.55%.

Nonetheless, looking further out, Today reference 131.50:

- 2.60% = 130.94.

- 2.65% = 130.42 (the 2025 high is at 2.653%).

- 2.70% = 129.89 (the 2024 high is at 2.706%).

ECB: Schnabel's Comments On Q4 BLS Ignore Tightening In Standards

Schnabel highlighted signals of increasing loan demand from the latest Bank Lending Survey (BLS) as evidence that ECB easing is being transmitted to the real economy. Meanwhile, she did not make reference to the tightening of lending standards reported in the same survey.

- Even if rate cuts are feeding through into increased loan demand, tighter standards amongst banks will limit the pass through of that demand into the real economy. All else equal, this suggests a more restrictive policy stance than implied by loan demand alone.

- Relevant excerpts from Schnabel’s interview: “For corporate loans, 90% of banks said in the most recent round that the general level of interest rates has no impact on loan demand, while 8% said it has lifted credit demand”….”It’s even clearer when you look at mortgages. Almost half of banks said in the most recent round that the general level of interest rates is supporting loan demand.”

- ECB Chief Economist Lane noted on Feb 5 that this tightening of standards was “driven by the fact that banks see higher risks to the economic outlook and have lower tolerance for taking on credit risk”.