EU AUTOMOTIVE: Week in Review

After much lobbying the EU finally relaxed emissions rules on OEMs. It will now allow shortfalls on EV targets this year to be made up in the following two. Trump announced he would press ahead with Canada and Mexico tariffs, in a blow to OEMs. The market reaction was limited, viewing it as a temporary bargaining position. By Wednesday the sector had won one month exemption for USMCA compliant firms.

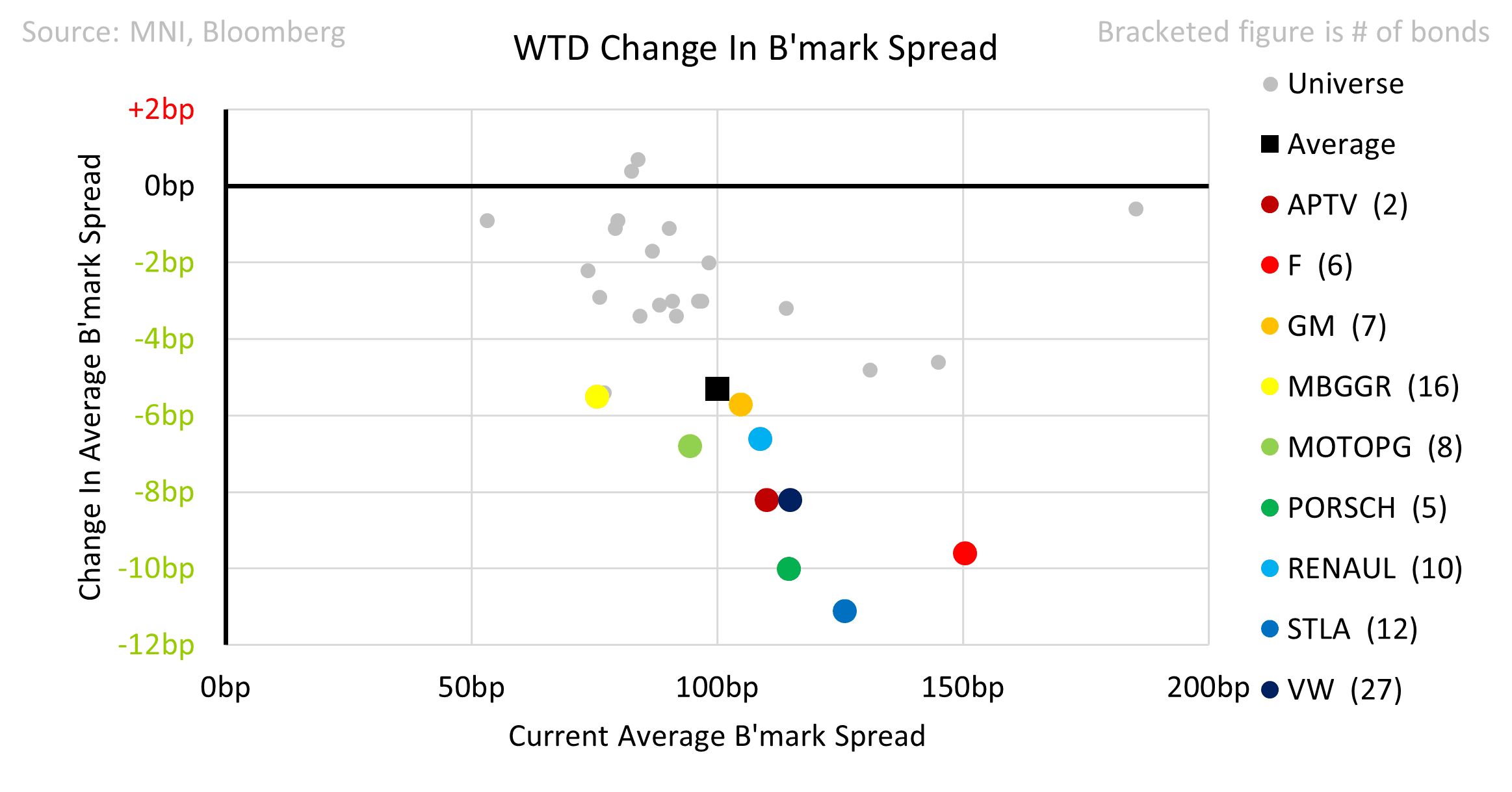

- Spreads finished the week 5bp tighter, boosted by the latest tariff twist. That left STLA (-11) the top performer despite the downgrade.

- Schaeffler guided for soft FY25 margins and FCF. Leverage is stuck well above target.

- Continental reported a small 4Q beat on margin improvement but gave soft outlook. Note: our post contained a typo; FCF guidance was 18%, not 80%, below expectations.

- Stellantis was downgraded one notch to BBB by S&P, which always seemed likely. The agency continues to take a relatively optimistic view on margin recovery, which could expose the name to further downside risk.

- Nissan was cut by one notch to BB by S&P, with outlook remaining negative. Ratings reflect deteriorating fundamentals, while a potential rescue remains the credit focus.

Rare Harley-Davidson EUR issuance received a lot of attention. It priced 15bp wide to our FV and currently trades 10bp inside reoffer. It could be exposed to downgrade risk if margins fail to recover this year.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Early SFOR/Treasury Option Roundup: 5Y, 10Y Puts

Trading desks report varied SOFR & Treasury options overnight, better volumes in Mar'25 10Y puts, 5- and 10Y midcurve puts as well. Reminder, March options expire on Feb 21, March futures roll to June at the end of the month. Underlying futures drift higher, at/near overnight highs w/ TYH5 highest since December 18. Projected rate cuts through mid-2025 gain slightly vs. late Tuesday levels (*) as follows: Mar'25 at -4.2bp (-3.7bp), May'25 at -11.2bp (-11bp), Jun'25 at -22.1bp (-21bp), Jul'25 at -28.1bp (-26.9bp).

- Treasury Options:

- over 15,400 USH5 110 puts, 3 last

- over 7,500 USH5 112 puts, 12 last

- over 4,000 TYH5 107.75/108.25/108.5/109 put condors ref 109-16

- over 17,000 TYH5 109 puts, 26 last ref 109-15.5

- 3,000 TYJ5 109.5 calls, 57 ref 109-14

- 2,000 TYJ5 114/116 call spds

- 1,800 TYH5 110.5/112.5 1x2 call spds ref 109-13.5

- 5,000 TYH5 106/107 put spds, 2 ref 109-13.5

- 3,000 TYH5 110.5 calls, 14 last ref 109-12.5

- 1,500 FVH5 105/105.5/106 put trees ref 106-22.75

- over 10,000 wk1 FV 106/106.25 put spds ref 106-22.75 (exp Friday)

- 4,500 wk2 FV 107/107.75 call spds ref 106-20.75 (exp Feb 14)

- over 5,300 Wednesday weekly 10Y 109 puts, 4 (expire today)

- Several wk1 TY put flows via outright, trees & spds, total volumes so far: over 12,800 wk1 TY 108 puts; over 19,200 wk1 TY 108.5 puts; over 13,000 wk1 TY 109 puts

- SOFR Options:

- 2,300 SFRK5 95.62/95.75/95.81/95.87 put condors ref 95.90

- 6,000 0QH5 95.50/95.81/96.00 broken put trees ref 96.14

- 2,000 SFRM5 96.12/96.18 call spds ref 95.895

- 1,500 0QM5/0QU5 96.75/97.25 call spd spd vs.

- 1,500 3QM5/3QU5 96.75/97.25 call spd spd

US TSYS/SUPPLY: Refunding: Watch Guidance

A recap of expectations for today's Treasury Quarterly Refunding Announcement (0830ET):

- There is no expectation of any changes to nominal coupon sizes in the upcoming Feb-Apr quarter vs the previous quarter. Issuance is set to resume next week with sales of $58B in 3Y Note, $42B in 10Y Note, and $25B in 30Y Bond.

- The main question is whether Treasury changes its current guidance that it does not "anticipate needing to increase nominal coupon or FRN auction sizes for at least the next several quarters." MNI will cover this via "Instant Answers".

- A majority of analysts whose Refunding previews we saw expect this guidance to be changed, with some (fairly limited) risks of removal of the phrase altogether. Eliminating, or softening, that language could be negative for Treasury markets as it would signal that an increase in coupon sizes is fairly imminent.

- “No change” would bring a mildly bullish relief rally for longer-end Treasuries in the very short run, we feel. Other possibilities (all of them softening the guidance) include:

- Affirmatively stating that coupon sizes are expected to rise at some point (ie later this year)

- Deleting "at least" (so it reads "does not anticipate needing to increase ... for at least the next several quarters")

- Changing the duration from "several quarters" to a shorter time period

- We may also get some limited commentary on Treasury's approach to the debt limit, though not much is expected at this time.

- Full preview here

STIR: Bank Of America Continue To Like Receiving Dec OIS

Bank of America continue to like receiving Dec ECB-dated OIS (target: 1.30%, stop: 2.05%).

- They write “the ECB continues its dovish shift, consistent with the deterioration in the outlook: (1) GDP disappointed; (2) consumers remain cautious; (3) tariff risks weigh on prospects.”

- They believe that the Bank’s “comments on the neutral rates suggest: (1) policy rates are still restrictive; (2) the ECB is not necessarily "only" normalising policy rates.”

- As a result, they see “a low hurdle for 2.00% rates by mid-year, absent any energy price shock”, noting their economists still forecast a 1.50% deposit rate come September.