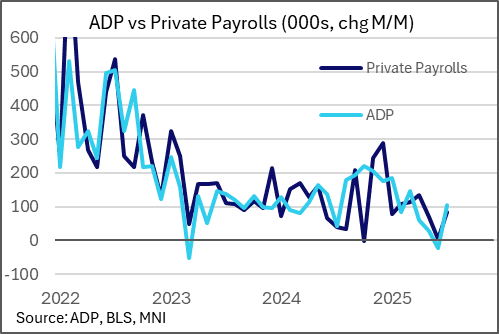

US LABOR MARKET: Waller's Speech Hints At Further Weakness In Private Payrolls

Aug-29 12:04

Fed Gov Waller's speech Thursday arguing for a 25bp rate cut in September and "additional cuts over the next three to six months" makes the case largely on the basis of risks to the labor market. In this context, he says "I tend to focus on the private sector as a better indication of the underlying momentum in the labor market", and the speech contains an intriguing footnote in saying that after getting the Sep 9 benchmark revisions that "private-sector employment actually shrank, on average, in the past three months":

- The footnote: "I also look at timely data that Federal Reserve staff maintains in collaboration with the employment services firm ADP to construct a measure of weekly payroll employment, which covers about 20 percent of the nation's private workforce. This measure is comparable to the one ADP publishes. The current May–July contour for the staff measure of ADP-based private employment is broadly consistent with that of the Current Employment Statistics numbers. And in the weeks after the July jobs report's reference period, preliminary estimates from ADP show continued deterioration."

- The Fed has long collaborated with ADP as a way to experiment with using timely big data from private sector sources but they don't make their internal analysis public regularly, so this is a bit of an interesting insight into underlying deterioration that may only become clearer in the upcoming ADP report (if not the nonfarm payrolls report itself). A Fed article on the topic from 2019 is here.

- Current consensus for August ADP employment (out on Thurs Sep 4, a day ahead of NFPs) is for 60k gains, after 104k in July (which had been an upside surprise vs 76k consensus); nonfarm private payrolls are seen rising 75k after 83k. There are only a handful of ADP estimates so far and all appear to have been made before Waller's speech, and we wonder if consensus will shift even lower to reflect this observation.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY FUTURES: BLOCK: Sep'25 2Y/5Y/30Y Ultra Package

Jul-30 12:02

- 3-Leg package crosses on the CME Group's Block screen at 0741:37ET:

- 3,000 TUU5 103-21.12, post time offer

- 2,500 FVU5 108-14.75, post time offer

- 1,500 WNU5 117-23, well through 117-20 post time offer

MNI: Instant Answers For Refunding, Bank of Canada, Fed Today

Jul-30 12:01

We have selected the following questions for MNI's Instant Answers for today's major North American events - will be published upon release:

Treasury Quarterly Refunding (0830ET):

- In addition to providing the new auction sizes for the upcoming quarter, we will answer this question upon release of the Treasury Quarterly Refunding Statement (with color on changes if any): Is the guidance on coupon issuance unchanged? “Treasury anticipates maintaining nominal coupon and FRN auction sizes for at least the next several quarters.”

- Additionally we include the following questions on buybacks:

- Total maximum purchase amount of buybacks in the 20Y-30Y range (B USD)

- Total maximum purchase amount of buybacks in the 10Y-20Y range (B USD)

Bank of Canada (0945ET):

- Overnight Rate Target (%)

- Does the Bank signal it's prepared to LOWER rates in the future?

- Does the Bank reiterate it could LOWER rates if the economy weakens amid tariffs and inflation is contained?

- Does the Bank signal it is prepared to RAISE rates in the future?

- Does the Bank signal it intends to leave rates ON HOLD?

Federal Reserve (1400ET):

- Federal Funds Rate Range Maximum

- Number of dissenters

- Number of dissenters preferring a rate cut

- Number of dissenters preferring a 50bp cut

EGBS: Relief Rally Fades

Jul-30 11:58

Bund futures fade from recovery highs, leaving the range established in early London hours intact.

- A relief rally came on the lack of meaningful upside spending surprise in the German fiscal update, although the lack of truly new news meant that the rally was quickly halved as the initial impetus faded, with some recent selling pressure in Tsys also factoring in.

- Bund futures last little changed at 129.63, German yields flat to 1.5bp lower, 10s outperform on the curve.

- EGB spreads to Bunds are little changed to 1.5bp wider on the day, with little in the way of meaningful European headline flow to note outside of this morning’s data and German fiscal matters.