LOOK AHEAD: Waller Still To Come

Still to come today but after the close, potentially important remarks from Fed Gov. Waller (permanent voter, dove) on monetary policy at 1800ET (text + Q&A).

- A leading contender for the next Fed Chair role and now one of the outright doves on the FOMC, there are two-sided risks to market reaction.

- Whilst there is a low bar to him surprising hawkishly vs prior comments (especially if he offers stronger pushback against recent independence challenges), it’s worth noting that his dissenting statement warning on labor market stresses came just before the July payrolls report on Aug 1 with its huge downward revisions.

- Waller on his July dissent in favor of a 25bp cut (Aug 1): “I believe that the wait and see approach is overly cautious, and, in my opinion, does not properly balance the risks to the outlook and could lead to policy falling behind the curve. The price effects from tariffs have been small so far, and since we will likely not get clarity on tariff levels or their ultimate impact on the economy over the course of the next several months, it is possible that the labor market falters before that clarity is obtained—if it ever is obtained. When labor markets turn, they often turn fast. If we find ourselves needing to support the economy, waiting may unduly delay moving toward appropriate policy.”

- Kalshi betting has for a few weeks now had Waller as the top contender for the next Fed Chair, with a 30% chance. The “two Kevins” are next with Warsh at 22% and Hassett at 18%, with Stephen Miran (11%) and David Zervos (10%) rounding out the other candidates with >5% chance.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURJPY TECHS: Pierces 20-day EMA

- RES 4: 177.08 2.000 proj of the Feb 28 - Mar 18 - Apr 7 price swing

- RES 3: 175.43 High Jul 11 ‘24 and a key medium-term resistance

- RES 2: 174.86 1.764 proj of the Feb 28 - Mar 18 - Apr 7 price swing

- RES 1: 173.97 High Jul 27 and the bull trigger

- PRICE: 171.43 @ 18:27 BST Jul 29

- SUP 1: 171.05 Intraday low

- SUP 2: 170.81 Low Jul 11

- SUP 3: 169.77 Low Jul 7

- SUP 4: 168.89 50-day EMA

The bullish trend condition in EURJPY remains intact, and for now a pullback is considered corrective. Initial support has been pierced at the 171.53 20-day EMA. A clear breach of this average would signal scope for a deeper correction and highlight potential for a move towards the 50-day EMA, at 168.89. Moving average studies remain in a bull-mode position highlighting an uptrend. A break of Monday's 173.97 high would resume the bull cycle.

BOC: Instant Answers For BOC Decision (4/4)

Following are the Instant Answers for the Bank of Canada decision due Wed at 945am EST:

- Overnight Rate Target (%)

- Does the Bank signal it's prepared to LOWER rates in the future?

- Does the Bank reiterate it could LOWER rates if the economy weakens amid tariffs and inflation is contained?

- Does the Bank signal it is prepared to RAISE rates in the future?

- Does the Bank signal it intends to leave rates ON HOLD?

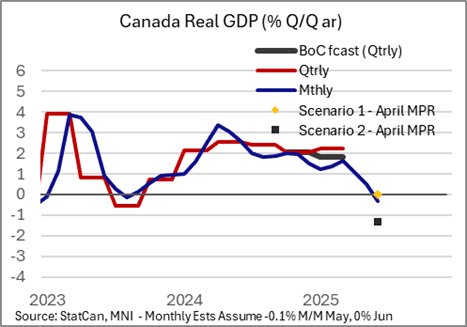

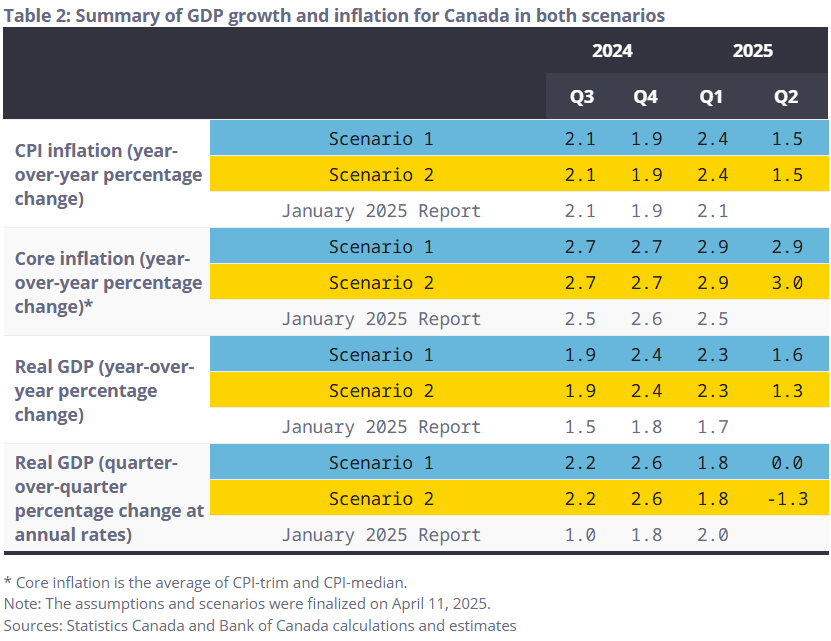

BOC: Forecasts To Be Less Pessimistic, Uncertainty Precludes Firm Guidance(3/4)

The prior Monetary Policy Report (April)'s summary table is below, showing two “scenarios”, one more pessimistic on the outlook than the other amid tariff threats. The BOC has signaled a preference to get back to a central forecast as opposed to dual scenarios, though it’s not likely that will happen in July.

- That’s because of multiple areas of uncertainty that could continue to warrant scenario-based analysis. First and foremost is US President Trump’s stated deadline of August 1 to reach a trade deal with Canada, absent which a 35% tariff rate on Canadian exports to the US has been threatened.

- We could add to such areas of uncertainty the federal government’s fall budget and various incoming data, but those are fairly ordinary areas of uncertainty and the US tariff situation is enough to keep the outlook extremely clouded.

- Given the above, we expect to see another dual-scenario outlook, albeit a more optimistic one than April’s on the activity front.

- As the aforementioned data since April suggests, this will include a less negative estimate for Q2 GDP with slightly higher core inflation. If they do publish a single, central forecast, this would be a surprise and suggest that the BOC has more confidence in its ability to make projections despite aforementioned uncertainties.

- The policy statement should reflect this better-than-expected economic activity evolution as well, suggesting as Gov Macklem has previously that reality has unfolded much closer to Scenario 1 than Scenario 2. There could be some note of continued elevation in core inflation metrics. In June the BOC noted "firmness in recent inflation data" which could stand, though "softer but not sharply weaker" economic activity could sound a little more positive this time.

- Once again, however, we do not expect any firm forward guidance given tariff uncertainty.