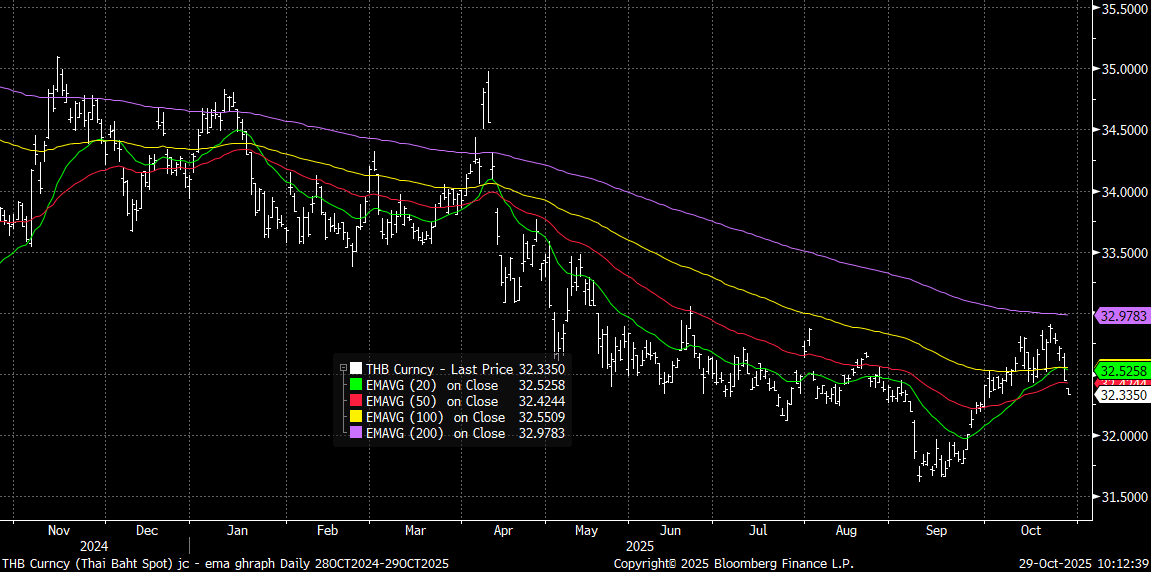

THB: USD/THB Breaking Lower, Back Under All Key EMAs

USD/THB is lower from the open, last under 32.35, up around 0.355 in THB terms. A few snippets below from Rtrs on stops and intervention. This puts us back under all key EMAs, with both the 20 and 100-day being support points of late (both around 32.53/55). Broader USD softness is being led today by fresh USD/JPY weakness. Gold steady, but comfortably off recent highs (last under $4000).

- "USD/THB opens lower, stops below 32.50, 32.40 hit, Pair traded 32.28-57 range overnight, closed at 32.36, Absence of BOT intervention risks 32.20 next, eyes exporters sales" - RTRS

Fig 1: USD/THB Back Under Key EMAs

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Cash Open

TYZ5 is trading 112-12+, up 0-04 from its close.

- The US 2-year yield opens around 3.635%, down 0.01 from its close.

- The US 10-year yield opens around 4.166%, down 0.01 from its close.

- 10-Year yields persisted with its probe of the 4.20% area, I suspect buyers continue to be around 4.20% initially and look to fade the move higher. The jobs data if released will be key this week. A move back above 4.35%/4.40% is needed to negate the downtrend.

- MNI FED BRIEF: Fed's Barkin-Jobs Shakier, Inflation Less Troubling. The U.S. employment outlook has deteriorated following recent weakening in payroll growth and large downward revisions to past numbers, while inflation has not risen as much as had been feared due to tariffs.

- MNI US DATA: PCE Spending Looks More Robust After Revisions. August's PCE spending and income data showed robust spending dynamics, especially when strong upward revisions to Q2 are considered. However, the income data didn't cast quite as solid a light on the underlying dynamics.

- Data/Events: Pending Home Sales, Dallas Fed Manf. Activity

AUSTRALIA: RBA Widely Expected To Hold On 30 September

The focus of the week will be Tuesday’s RBA decision followed by Governor Bullock’s press conference. As it is widely expected to keep rates at 3.6% and there won’t be an updated set of forecasts, the tone of the statement and Bullock’s comments will be scrutinised after disinflation appears to have stalled in Q3 and the Governor said to a parliamentary committee last week that "domestic data have been broadly in line with our expectations or if anything slightly stronger". The Board is likely to remain highly data dependent.

- The RBA’s Financial Stability Review is published on Thursday.

- There is quite a bit of second tier data starting with August building approvals on Tuesday. After falling sharply in July due to the volatile multi-dwelling component, it is forecast to rise 2.6% m/m.

- Tuesday also sees private credit for August which is forecast to rise by 0.6% m/m again. In July it was 7.2% higher than a year ago.

- The final September S&P Global manufacturing PMI is released on Wednesday and services/composite on Friday. The preliminary readings moderated across manufacturing and services.

- August household spending, which has replaced retail sales, prints on Thursday and Bloomberg consensus expects a 0.3% m/m increase after 0.5% the previous month which would leave the annual rate at 5.2%.

- Merchandise trade for August is also published on Thursday and the surplus is projected to narrow to $6.2bn from $7.3bn.