KRW: USD/KRW Gaps Lower, No Clear Headline Drivers

USD/KRW lower in latest dealings, last near 1391.50, up around 0.55% in won terms. We haven't seen any fresh headline drivers for the move, looks isolated compared to other USD/Asia moves, or the G10. Resistance has been evident in the pair around the 1400 level so far this week, albeit with a brief test above this level in Thursday trade.

- The Kospi tracking higher, last up around 0.70%, with offshore investors modest buyers so far today (per NBUY on BBG).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA: Focus On Trade Flows

A European official stated that the European delegation is not expected to reach a substantial deal from its upcoming Chinese meeting. It hopes to make it clear what it wants Beijing to do to generate sustainable economic relations and rebalance ties. Our China policy team noted at the start of the week: “European Commission President Ursula von der Leyen will warn Chinese Premier Li Qiang at a one-day summit in Beijing on July 24 that the state of trade relations is "unsustainable,” raising issues of China's industrial overcapacity, as well as lack of market access and free and fair competition, the official said.” Below are some more viewpoints which have been expressed on X:

- Brad Setser on X: “The (European)Commission has (I hope) recognized that it can no longer make do with pretend deals that offer the illusion of progress without resolving the very real underlying problem …Europe (and Germany) has sort of gotten mugged by trade reality.”

- “German exports of autos to China, for example, are down by about 50% relative to their levels in 2014 -- 2022. The slump in German exports to China over the past couple of years is actually bigger, relative to German GDP, than the slump in German exports to the US during the great financial crisis.”

- “Europe's exports to China, as a share of China's GDP, are about half of what they were before China joined the WTO. It sort of goes without saying that a lot of this has been driven by auto trade.”

- “These dramatic sector shifts are what China's $2 trillion surplus in manufacturing trade means in practice. I welcome Europe's new realization that Europe has a clear interest in rebalancing its trade with China, which ultimately requires rebalancing China's own economy.’

- Robin Brooks on X: “Macro 101 on China tariffs. If China doesn't transship goods to the US, it must export them to the rest of the world (ROW). Supply of goods to ROW goes up. Since ROW demand is unchanged, prices must fall to generate demand. US tariffs are a deflationary shock for China and ROW.”

- “China is in a tough spot. Its exports to the US are down -24% q/q in Jun '25. Exporters have only 2 options: (i) transship to the US; (ii) export goods to other countries at a discount to generate demand. Either way, a big hit to profitability and a deflationary shock for China.”

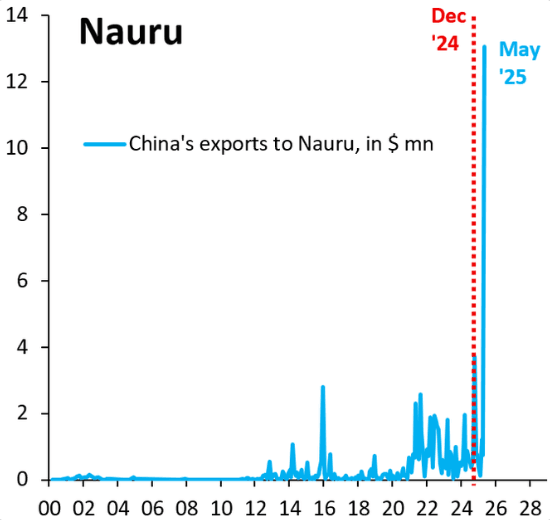

- “Nauru is the 3rd smallest country in the world after the Vatican and Monaco. But more importantly right now, it's also the Kyrgyzstan of Micronesia. China's exports to Nauru are up 1400% in May from a year before. A sign how desperate China's exporters are to offload their stuff.”

Fig 1: China Exports To Nauru

Source: MNI/@robin_j_brooks

JGBS: Holding Sharply Cheaper Ahead of 40Y Supply

At the Tokyo lunch break, JGB futures are sharply lower, -92 compared to settlement levels.

- US President Trump has posted via Truth Social that the US and Japan have reached a trade/investment deal. Trump stated that Japan will invest $550bn into the US, while Japan will also open up access to cars, agriculture exports from the US. Japan will pay a 15% reciprocal tariff to US Trump notes. This is lower than the 25% rate which had been threatened.

- Japan equities are rallying in the first part of Wednesday trade, as details filter out around the trade agreement with the US. This is aiding Japan automakers in the first part of trade.

- Cash US tsys are 1-2bps cheaper in today’s Asia-Pac session after yesterday’s modest rally.

- Cash JGBs are 4-8bps cheaper across benchmarks. The benchmark 40-year yield is 4.1bps higher at 3.418% ahead of today’s supply.

- The previous 40-year auction was notably weak, with the high yield clearing well above dealer expectations. According to a Bloomberg survey, the market anticipated a yield of 3.085%, while the actual result came in at 3.135%.

- Swap rates are 3-9bps higher, led by the belly of the curve. Swap spreads are mostly wider.

JGBS AUCTION: Poll: 40-Year JGB Auction

*JAPAN 40Y GOVT BOND AUCTION MAY HAVE 3.35% HIGHEST YIELD:POLL – BLOOMBERG