CNH: USD/CNY Fixing Lower, Error Term Slightly Tighter

The USD/CNY fix printed at 7.1350, versus a Bloomberg market consensus of 7.1768.

- Today's fix is just a touch above recent lows of 7.1345. The fixing error was a touch tighter at -418pips. Yesterday's outcome was -487pips.

- USD/CNH is little changed so far today, last near 7.1850 and hasn't shown much reaction to the fixing outcome.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: 10Y Leads Market Cheaper, Machine Orders Slightly Above Est.

In Tokyo morning trade, JGB futures are weaker, -32 compared to settlement levels.

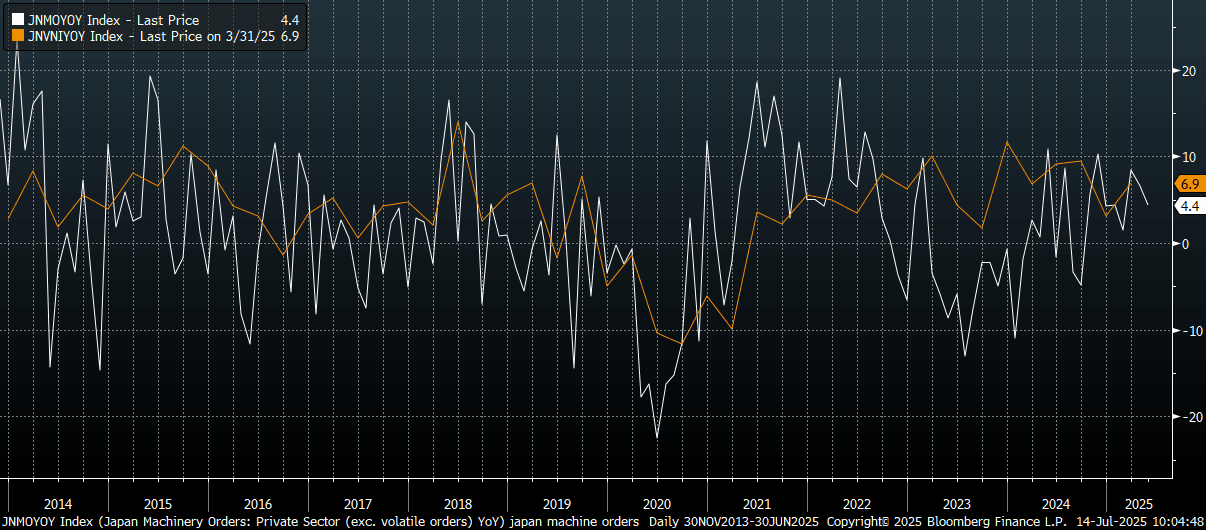

- Japan May machine orders were slightly above market forecasts in m/m terms. We printed at -0.6%m/m, versus the -1.5% forecast. The April fall of -9.1% was unrevised. In y/y terms, we were slightly below forecasts, printing 4.4%, versus 5.2% expected, while 6.6% was the May outcome.

- Cash US tsys have extended Friday’s bear-steepener in today’s Asia-Pac session, with yields flat to 2bps higher.

- Cash JGBs are flat to 3bps cheaper across benchmarks, with the 10-year leading. The benchmark 10-year yield is 2.5bps higher at 1.547% versus the cycle high of 1.596%.

- (Bloomberg) "JGBs can’t expect much help from the calendar this week with auctions light and macro risks high, so the path of least resistance is steeper. Along with the read across from a widening Treasuries curve is the threat of Japan’s ruling LDP losing its majority in Sunday’s upper house elections. That’s a warning for the nation’s fiscal trajectory, already one of the ugliest among developed markets."

- Swap rates are little changed. Swap spreads are mostly tighter.

US STOCKS: S&P Pauses Ahead Of 6300, New Tariffs See Futures Open Lower In Asia

The ESU5 Friday night range was 6276.75 - 6312.75, Asia is currently trading around 6276. The September contract traded sideways on Friday just off its all-time highs. This morning has seen US futures open under pressure with Trump issuing fresh 30% tariffs on Europe and Mexico starting Aug. 1, ESU5 -0.40%, NQU5 -0.40%. The market has most recently been able to look through these tariffs, is this just another dip to be added to or will their accumulation finally tell ?

- Daily Chartbook on X: "While the rally has surprised many investors (including us), risk sentiment indicators remain broadly neutral, which suggests that many investors haven't participated in the rally. - TS Lombard”

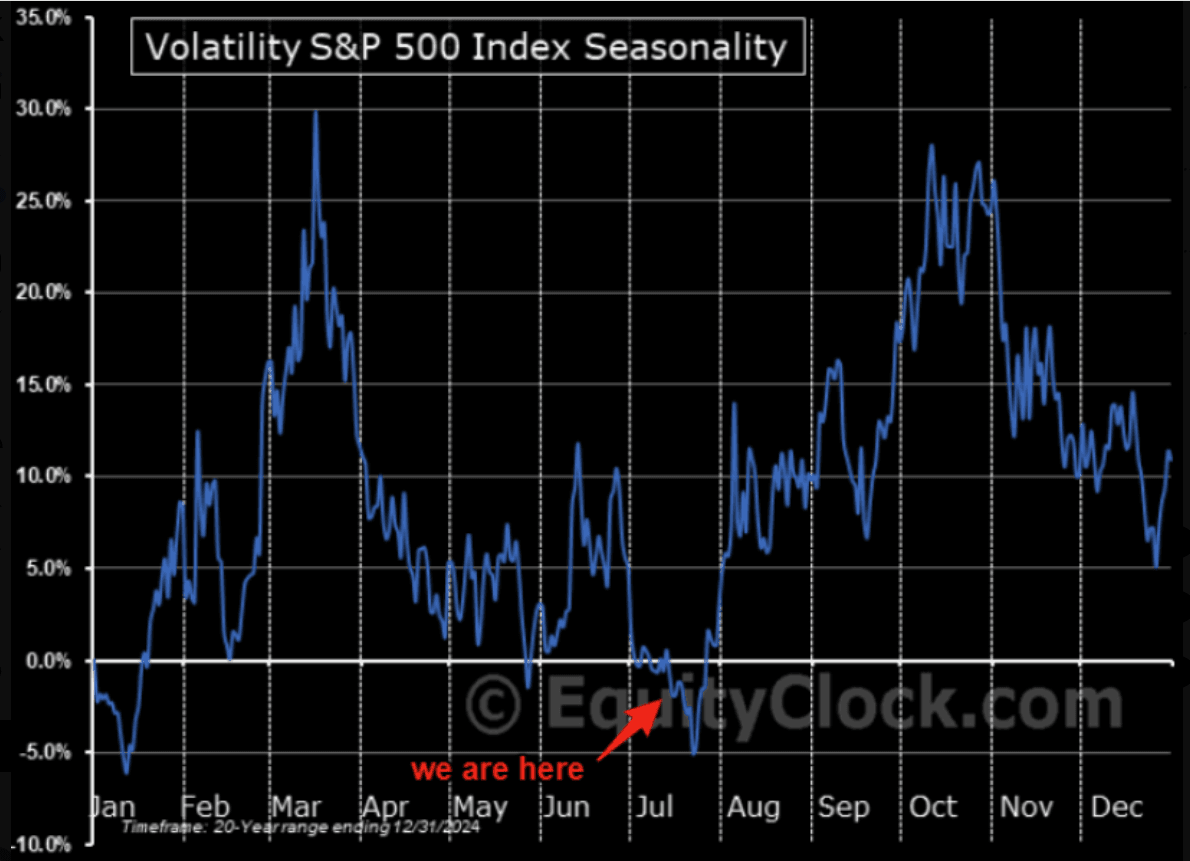

- Lance Roberts on X: “The markets are very complacent and expectations are high for a continued bull run. However, one thing to consider is that we are moving into the seasonally strong period for volatility." See Graph Below.

- (Bloomberg) - “Perhaps the most remarkable thing about the resurgence of tariff risk this week is how markets ignored it. The dollar climbed, high-yield spreads widened a measly 11 bps in the first four days of the week, and the S&P 500 notched up yet another record high as the VIX basically yawned.”

- “Earnings season starts again with the focus on the big banks. Volatility over the last quarter will have helped trading desks across the street, however investment banking revenues may be impacted by the slower pace of dealmaking.” - BBG

- Short-term this is starting to look a little overdone but the market clearly disagrees for now and sees the potential for a melt-up. First support is back towards the 6100 area.

Fig 1: VIX S&P Seasonality

Source: MNI/@LanceRoberts/EquityClock

JAPAN DATA: Core Machine Orders Y/Y Slows, But Still Pointing To Resilient Capex

Japan May machine orders were slightly above market forecasts in m/m terms. We printed at -0.6%m/m, versus the -1.5% forecast. The April fall of -9.1% was unrevised. In y/y terms we were slightly below forecasts, printing 4.4%, versus 5.2% expected, while 6.6% was the May outcome.

- The chart below plots core machine orders, in y/y terms, against Japan quarterly capex (also in y/y terms). It implies some softer Capex momentum risks all else equal, but still positive growth.

- Looking at the detail, manufacturing orders fell by 1.8%m/m (after a 0.6% dip in April). Non-manufacturing surged by 30.4%m/m though, to provide some offset.

Fig 1: Japan Core Machine Orders & Capex (Y/Y)

Source: Bloomberg Finance L.P./MNI