CNH: USD/CNY Fixing Holds Above Recent Lows, Fixing Error Close To Flat

The USD/CNY fix printed at 7.1013, versus a BBG market consensus of 7.1027.

- Today's fix is still above recent lows (7.1008 from Sep 9). The fixing error was close to flat at -14pips.

- The fact we haven't broken down through 7.1000 from a fixing standpoint, despite broader USD softness, has helped push USD/CNH in latest dealings. We were alst around 7.1070. Earlier lows today were at 7.1007 for the pair.

- This backdrop is likely to see CNH maintain a low beta with respect to further USD losses.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA SETS YUAN CENTRAL PARITY AT 7.1322 MON VS 7.1331

- CHINA SETS YUAN CENTRAL PARITY AT 7.1322 MON VS 7.1331

CHINA: China - Macro, Valuations, Sentiment & Technicals

Macro: Following a large release of data last Friday, a quieter week ahead for China. Key data last week showed growth moderating across key indicators such as retail sales, industrial production, fixed asset and property investment and capped off by further declines in house prices. For this week, the July FDI stats will be released and is expected that the contracting will continue. Wednesday sees the decision on Loan Prime Rate decision and with bank's margins already pressured, there seems little probability that there will be changes to LPR's. Important to note that changes over the last 12 months has diminished the importance of LPR, with focus on daily open market operations and the 7-day repo rate. China's next steps involve a multi-pronged approach to stimulate economic growth by balancing monetary and fiscal policies, strengthening domestic demand, modernizing its industrial base, and managing financial risks. The fourth plenary session of the 20th Communist Party of China (CPC) Central Committee will be held in Beijing in October when the 15th five year plan will be announced.

Valuations : The CSI 300 delivered another strong week last week with gains over 2% to trade above the 4,200 level. With P/Es at 16.9 the CSI 300 remains well above December near term lows but below the 5-year highs of late 2020. Bond valuations remain anchored with the 10yr finding it difficult to break away from the 1.70% level. Currency wise last week we saw the fix hit a fresh levels not seen since early November last year, while USD/CNH remained within recent ranges. The CNY basket tracker remains close to recent lows.

Sentiment: The performance in the stock market will no doubt lead into some improvements in sentiment but the realities of the housing market continue to weigh heavy over the broader economy. We are seeing signs of asset allocation shifts out of bonds into stocks but seem limited upward pressure on bond yields for now. There is approximately 30 companies reporting results this week and several IPOs which should be the main driver of investor sentiment, though are likely to be mixed at best

Technicals: The technicals remain very much skewed to low volatility in bonds, in what appears to be a very tightly held market for now. The PBOC seems to have limited appetite for bond yields to move higher, especially with the volume of issuance expected for the back end of the year. The move higher in August for the CSI 300 has taken it above all major moving averages, and a poor set of company releases could feed into a pullback. For USD/CNH, we sit near key EMA level, with the 50-day around 7.1880.

FOREX: AUD Crosses - Underperform Against GBP & EUR

US equities momentum stalled heading into the weekend. This morning US futures opened a little higher, ESU5 +0.15%, NQU5 +0.25%. The AUD performance continues to be mixed in the crosses, with only the GBP and EUR remaining well supported against it.

- EUR/AUD - Friday night range 1.7933 - 1.7993, Asia is currently trading around 1.7865. The direction US stocks ultimately decide on following will have a direct impact on the direction of this pair. It is currently probing the top end of its 1.7650/1.8100 range, which has seen decent supply cap it the last few months.

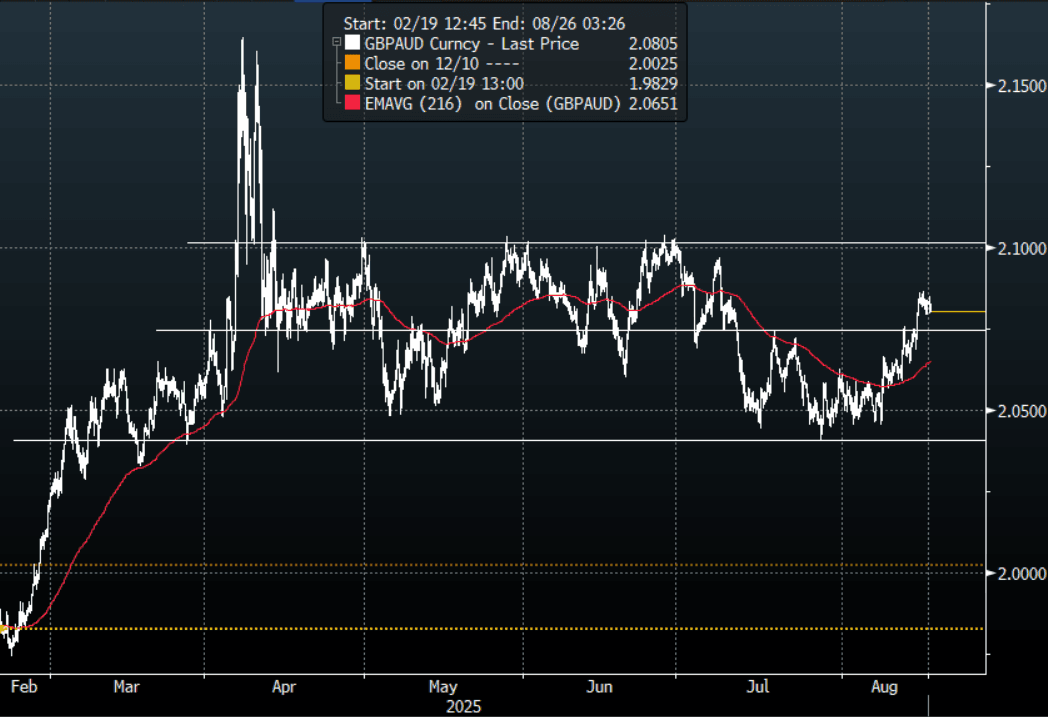

- GBP/AUD - Friday night range 2.0791 - 2.0840, Asia is trading around 2.0810. The pair is breaking above the pivot within its 2.0400 - 2.1050 range and should this hold dips will be supported enroute to 2.10/11.

- AUD/JPY - Friday night range 95.53 - 95.88, Asia is trading around 96.05. The pair found good demand last week towards 95.50, price is now firmly back into the 94.50-97.50 range looking for clearer direction.

- AUD/NZD - Friday night range 1.0979 - 1.0995, the cross is dealing in Asia around 1.0965. The Cross is trying to push higher but will need a sustained break above the 1.1000 area. Until then the range looks to be 1.0850-1.1000.

Fig 1: GBP/AUD spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P