USD: USD losing further shine

The USD is starting the week on the backfoot, the DXY is back sub 103.00, tracking towards last week's lows around 102.65/70.

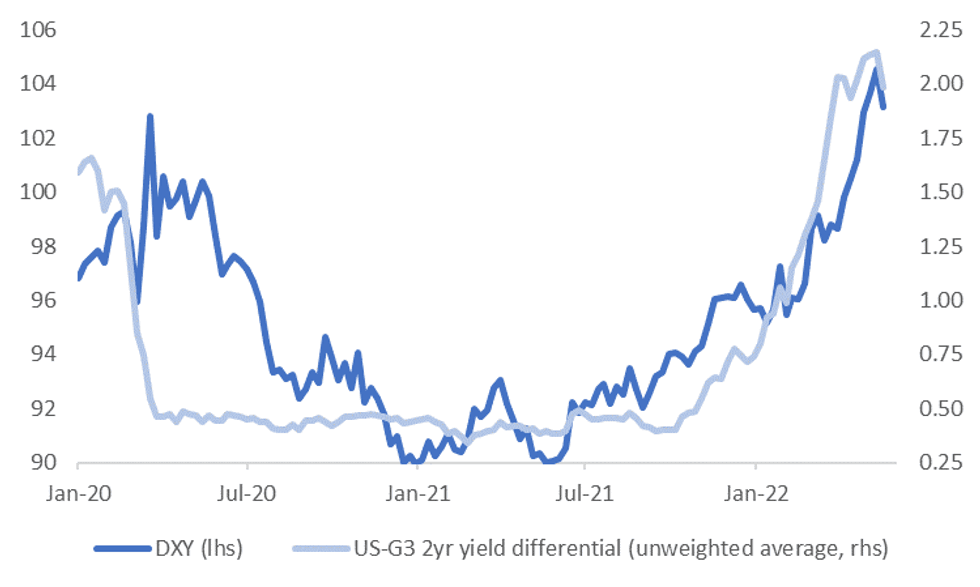

- Last week saw a decent pull back in the yield differential for the USD against other core markets. The first chart below plots the DXY versus the unweighted 2yr yield differential with the G3 markets. The spread fell by 16bps last week, which is the largest weekly drop since the early 2020 period.

- US yields were relatively steady, with much of the waning yield differential reflecting higher EU and UK yields.

Fig 1: DXY & US Yield Differential

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

- Still, stability in US yields no doubt helped. Fed expectations for end 2022/early 2023 have been fairly rangebound over this period.

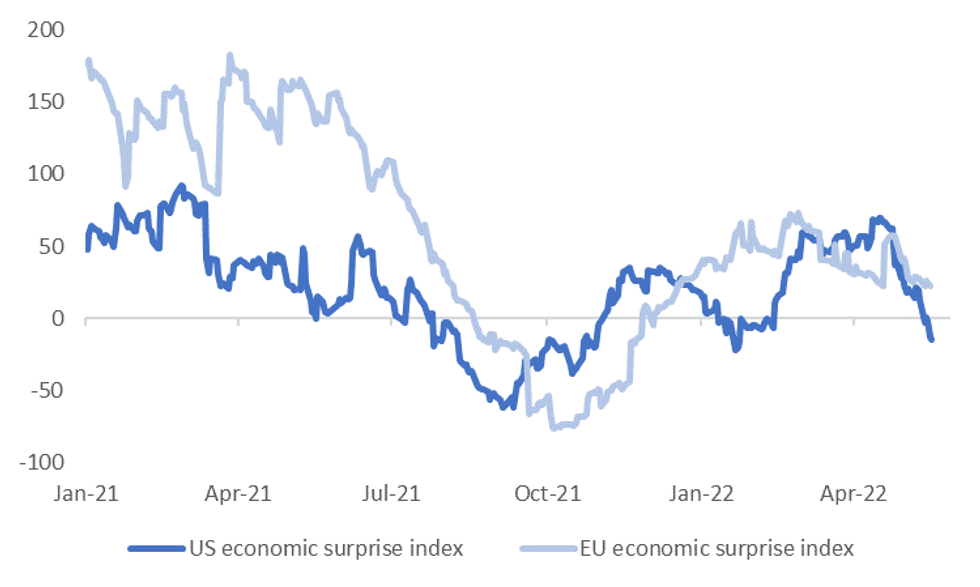

- As we highlighted last week, US data momentum has clearly rolled over, relative to expectations. The Citi US economic surprise index is almost back to year to date lows, see the second chart below. On a relative basis, there is now a reasonable wedge between this index and the equivalent reading for the EU.

- These relative shifts have weighed more on US growth expectations in recent weeks, at least according to the J.P. Morgan growth Forecast Revision Indices (FRIs).

- Better risk appetite, as reflected in higher US equity futures today, is also helping higher beta plays like AUD and NZD, although futures are off best levels. China and Hong Kong stocks are also struggling to replicate last week's strong performance in early trade today.

Fig 2: Citi US & EU Economic Surprise Indices

Source: Citi, MNI - Market News/Bloomberg

Source: Citi, MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY FUTURES: BLOCK, Late 2s/10s Steepener

Underscoring the bounce in 2s10s off earlier lows:

- +10,000 TUM2 105-10.12 post-time offer at 1606:05ET vs.

- -5,450 TYM2 118-30, sell through 118-31.5 post-time bid

US TSYS: Cleveland Fed Mester Pushes Back on 75Bp May Hike, Favors 50Bp

Rates trade modestly higher after the bell, recovering a portion of Thursday's sell-off. Bonds see-sawed +/- a few ticks around steady in early trade before making session highs around 1000ET, 30YY slipped to 2.8850% before climbing and holding a range from noon on around 2.9470%.

- Short end rates were under pressure for much of the session recovered slightly after the bell as Cleveland Fed Mester pushed back on any need for 75bps hike at May 4 FOMC, in favor of 50bp moves.

- Curves bounced off flatter levels: After tapping 42.0 ahead Mon's open, 2s10s fell to 14.108 low in the first half as markets price in the off chance of 75bp hike at the May 4 FOMC. Bbg noted Fed Swaps priced in 250bp in hikes by year end.

- Nomura analysts anticipate the Fed to make two consecutive 75bp hikes (June and July) after a 50bp hike on May 4:

- "For some time, our view has been that if the Fed could hike 200bp at one meeting without significantly affecting market functioning, they would. So far, markets have been reluctant to price 75bp hikes, but stronger pricing for such a move would likely ease the path for the FOMC and participants could likely forge a consensus on such action quickly".

- Fed enters Policy blackout at midnight tonight.

US TSYS: Eurodollar/Tsy Option Roundup

Gyrations in underlying FI futures Friday spurred buyers of wing insurance (low delta calls and puts), challenging environment for active traders. Bonds see-sawed around steady before rallying around midmorning, curves flattening with short end rates underperforming all session.

- Bonds trimmed gains by noon, holding to a narrow range while the short end pared losses after Cleveland Fed President Mester pushed back on any need to hike 75 bp at the May 4 FOMC in an interview on CNBC after the close. Note, lead quarterly Eurodollar futures EDM2 traded 98.11 (-0.065) after the bell vs. 98.050 session low.

- Salient Eurodollar trade included a buy of 5,000 Sep 97.75/98.00/98.25/98.50 call condors after block buy +10,000 Sep 96.00 puts, 7.0 ref 97.275.

- Treasury options saw decent 5Y volumes with 12,000 FVM 113/114 1x2 call spds at 5.5 and over 22,000 FVM 114 calls, 12.5-13. Early Blocks: total 25,000 FVM 111.5 puts, 34.5 vs. 15,000 FVM 112.5 puts, 62.