CNH: USD/CNH Back To Low 6.6900 Region, Caveats On Stimulus

After USD/CNH couldn't breach 6.7200 early yesterday, we tracked lower, getting close to 6.6900 late in NY trading. We currently trade around 6.6940.

- Much of the focus rested on China's proposed $220bn (1.5 trillion yuan) stimulus boost, whereby local governments can bring forward special bond sales from 2023 to the second half of this year.

- While clearly a positive development, some analysts have highlighted important caveats. Firstly, it could leave a fiscal cliff in 2023. Secondly, special purpose bond issuance needs to be tied to a specific project, so the stimulus could take a while to implement. Infrastructure investment is also less resource intensive compared to previous cycles.

- Nevertheless, anything that aids the China outlook can still underpin the outperformance theme. This week has seen some reversal in equities outperformance, with major developed market equities seeing some positive impetus.

- CNH resilience persists though, with USD/CNH flat on the week versus the DXY's 1.75% gain so far.

- On the Covid front, Shanghai reported a further 45 cases yesterday, down slightly from Wednesday's number, although no cases were found outside quarantine. Beijing reported no new local cases yesterday.

- The data calendar is quiet today, but tomorrow delivers PPI and CPI prints for June. PPI is expected to ease to 6.4% from 6.0%, but CPI is forecast to rise to 2.4%, versus 2.1% previously. Note from Saturday onwards aggregate financing and new loans for June are also due. Further gains are expected In both prints (agg finance to 4192.5bn yuan versus 2792.1bn previously, and new loans to 2400bn yuan from 1883.6bn yuan).

- Also note that US President Biden will reportedly meet with economic advisors on Friday (US time) to discuss possible tariff reductions.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: AUCTION PREVIEW: AOFM to sell A$800mn of 0.50% 21 Sep '26 Bond, issue #TB164

The Australian Office of Financial Management (AOFM) will today sell A$800mn of the 0.50% 21 September 2026 Bond, issue #TB164. The line was last sold on 29 April 2022 for A$1.0bn. The sale drew an average yield of 2.9040%, at a high yield of 2.9100% and was covered 4.6350x. There were 40 bidders, 10 of which were successful and 5 were allocated in full. Amount allotted at highest yield as percentage of amount bid at that yield was 9.2%.

- Results due at 0200BST/1100AEST.

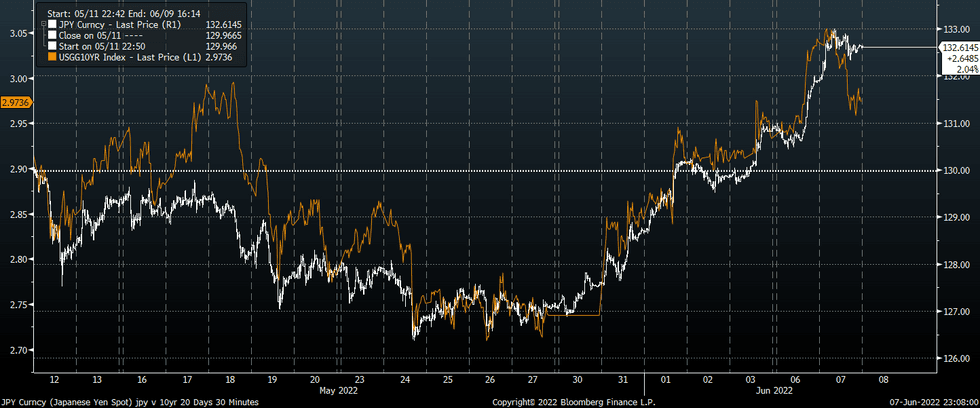

JPY: No Reprieve For Yen

Demand for USD/JPY emerged in early Tokyo trade Tuesday and intensified as BoJ Gov Kuroda reiterated his ultra-dovish policy mantra, with the pair printing a fresh two-decade high at Y133.00. The rate managed to remain afloat through the rest of the day despite a pullback in U.S. Tsy yields (see fig. 1).

- A decline in the VIX index to 24%, the lowest level since Apr 22, may have served as an offset to lower U.S. Tsy yields (carry trades are supported by lower equity vol). But if U.S. Tsy yields keep correcting, we may well see USD/JPY losing ground.

- In addition, the yen remained pressured via other currency pairs as the BoJ remains the lone dove among major central banks. A hawkish RBA rate decision pushed AUD/JPY above Y96.00, while EUR/JPY soared above Y142.00 ahead of this week's ECB meet.

- USD/JPY 1-month risk reversal extended gains after rising above par for the first time since May 11 on Monday, as bullish sentiment among option traders kept strengthening.

- Final quarterly GDP figures and monthly BoP current account balance will hit the wires shortly, with Eco Watchers Survey due later in the day.

- Yen weakness persists this morning, with USD/JPY trading +19 pips at Y132.78 as EUR/JPY rips through yesterday's best levels. Should USD/JPY break above round figure/ Apr 4, 2002 high of Y133.00/11, bulls could set their sights on Apr 1, 2002 high of Y133.84. Bears keep an eye on the 50-DMA, which intersects at Y127.96.

Fig. 1: USD/JPY vs. U.S. 10-Year Tsy Yield (%)

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

KRW: Tech Equity Sentiment Better, Q1 GDP Revised Lower

1 month USD/KRW spent most of the post-Asia close drifting lower. After touching a high of 1259.6, we got to 1254 in NY trading, in line with USD weakness and better equity market sentiment. Note spot closed yesterday onshore at 1257.40. The 50-day MA is at 1248.23.

- Tech equity sentiment was better overnight, the SOX up 0.99%, while the MSCI IT index gained over 1%. Both indices remain within recent ranges though. The China Golden Dragon index continued to recover, up a further 3.33% and above the 100-day MA in a meaningful way for the first time since March 2021.

- Still, the Kospi struggled yesterday, down 1.66%, while offshore investors shed $244mn of local equities. Sentiment should be better today.

- Locally, the focus will be on a potential North Korea nuclear test. This would be the first such test since 2017. The US has stated its response to such a test will be forceful, although it is unlikely to get much support at the UN for a coordinated response in terms of new sanctions, given Russia and China's likely veto.

- On the data front, Q1 GDP has been revised down a touch to 0.6% QoQ (from 0.7%), while YoY growth is 3.0%, versus 3.1% initially reported.