EU CONSUMER STAPLES: Unilever: Ice Cream Rated Baa2 by Moody's

(UNANA; A1/A+) (TMICC: Baa2)

Moody's initiates on the planned spin-off Ice Cream co at Baa2. In last earnings call Unilever said; "as part of the demerger process, we will be allocating debt between Unilever and The Magnum Ice Cream Company. This is expected to result in a net debt-to-EBITDA ratio of approximately 2x for Unilever, and a solid investment-grade profile of around 2.4x for The Magnum Ice Cream Company."

- Ice cream is a €8.3b in sales business running a 11.8% margin (<10% of Unilever's bottom line).

- The capital markets day for the spin-off is scheduled for 9th/coming Tuesday.

- Demerger and listing planned for mid-November.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: US TSY 17W BILL AUCTION: HIGH 4.105%(ALLOT 83.04%)

- US TSY 17W BILL AUCTION: HIGH 4.105%(ALLOT 83.04%)

- US TSY 17W BILL AUCTION: DEALERS TAKE 26.35% OF COMPETITIVES

- US TSY 17W BILL AUCTION: DIRECTS TAKE 5.67% OF COMPETITIVES

- US TSY 17W BILL AUCTION: INDIRECTS TAKE 67.98% OF COMPETITIVES

- US TSY 17W BILL AUCTION: BID/CVR 3.31

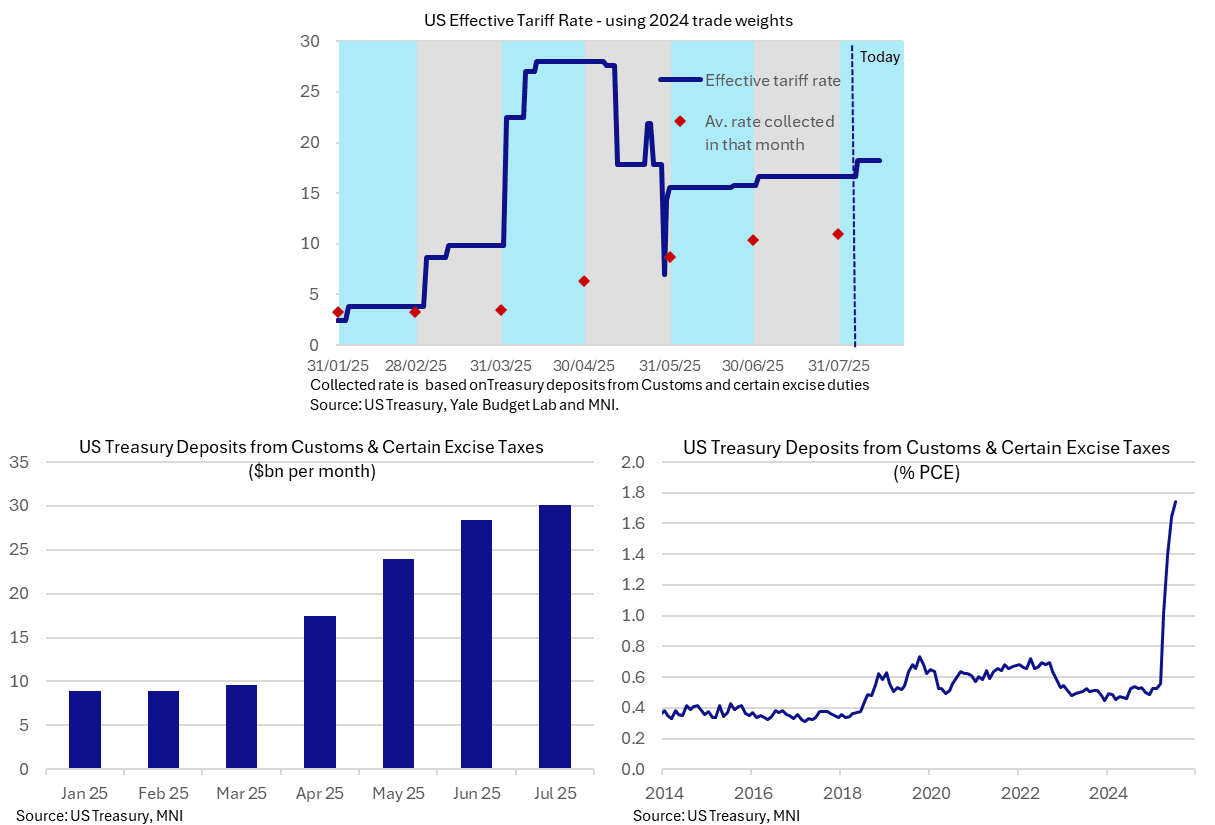

US OUTLOOK/OPINION: Still Some Way For Full Tariff Impact To Show On Prices

Looking ahead to next week’s US CPI (Tue) and PPI (Thu) releases, latest monthly tariff revenue for July suggests we’re still some way off seeing the full impact from tariffs on prices.

- The effective tariff rate currently stands at 18.3% according to Yale Budget Lab calculations (pre-substitution, i.e. keeping trade shares constant), up from 15.5-16% through June and 16.6% in July.

- In contrast, the $30bn of Treasury deposits from customs and certain excise duties in July was worth 11.0% of goods imports in 2024 (likely reflecting June average tariff rates suggesting further increases still to come). That’s up from 10.3% in June, 8.7% in May, 6.3% in April and 3.0% in Dec 2024 prior to the second Trump administration to give a sense of baseline.

- (Note that this 11.0% rate would be 10.3% if using a 12mth sum up to latest data for June owing to the sharp rise in imports in 1Q25. This dynamic approach with recent data can be misleading).

- Alternatively, these tariff revenues in July were worth ~1.7% of overall personal consumption expenditure, an increase of 1.3pp under the Trump administration.

- Of course, this doesn’t give insight into burden sharing across importers, businesses and consumers.

- On the former, June US import prices showed a partial correction stronger for those from China after what had looked like some taking of a tariff hit in April and May (implied by lower than usual import prices), but import prices more generally haven’t shown much concession. That’s in contrast to NEC Director Hassett saying on Aug 4 that data shows tariffs are being borne by foreign producers, although admittedly the extent to which they’re being borne is vague in that headline.

EQUITY TECHS: E-MINI S&P: (U5) Corrective Pullback Extends

- RES 4: 6523.63 1.764 proj of the May 23 - Jun 11 - 23 price swing

- RES 3: 6500.00 Round number resistance

- RES 2: 6477.31 1.618 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6468.50 High Jul 31 and the bull trigger

- PRICE: 6358.00 @ 16:20 BST Aug 6

- SUP 1: 6244.36 2.0% 10-dma Envelope

- SUP 2: 6239.50 Low Aug 1

- SUP 3: 6213.75 50% retracement of Jun - Aug Upleg

- SUP 4: 6203.65 50-day EMA

Equities sold off sharply Friday on the back of the soft NFP print - pushing prices through mid-July lows in the process. Since that spell of weakness, price has traded either side of support at the 20-day EMA, at 6325.25, signalling scope for a deeper retracement toward the 50-day EMA at 6203.65. Clearance of this average is required to signal a stronger reversal. The primary trend remains up, leaving key short-term resistance and the bull trigger at 6468.50, the Jul 31 high.