EU REAL ESTATE: Logicor: 1H 25 Results

Stable Results. Issued recently.

• Net Rental Income €395m +2.3%; +5% lfl

• NOI €364m +1.9%

• Occupancy 93.2% down slightly from 94.0%. Nordics low at 85.8% (is 8.9% of portfolio)

• GAV €15.1bn with stable valuations. Disposals of 500m

• Adj EBITDA €304m down 3% on higher expenses.

• Strong Re-leasing spread of 32%.

• ND/Adj EBITDA 12.0x vs 12.5x

• ICR 2.9x vs 3.3x.

• Net Debt reduced to €7.3bn from €7.7bn

• Weighted Ave Maturity was reported at 3.4yrs down from 3.8yrs but the company raised €500m July 32 after the reporting period.

(LOGICR; NR/BBB/NR)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: 10-year Gilt/Bund Spread Tightens Post Auction

Solid demand at today’s 10-year Gilt auction helps the Gilt/Bund spread fully unwind early widening. The spread is now 0.5bps tighter on the session at 188bps, after reaching a high of 190bps ahead of the Gilt supply.

- 10-year Gilt yields are currently 4.51%, eyeing another test of the 4.50% level which provided support earlier this morning. The UK curve is lightly twist flatter, with 2-year yields up 0.5bps.

- German yields are up to 1bp higher across the curve, ahead of E5bln 1.90% Sep-27 Schatz supply at 1030BST.

- 10-year EGB spreads to Bunds are within 0.5bps of yesterday’s closing levels. Austria sold 8/10-year RAGBs this morning.

- Gilt and Bund futures are up to 5 ticks above yesterday’s settlement levels, still holding onto most of Friday’s US labour market report-inspired rally. A bullish theme is currently intact in both contracts.

- Today’s regional data calendar has been heavy, but not very market moving. Industrial production was stronger-than-expected in France and Spain, while the Eurozone final July services/composite PMIs saw marginal downward revisions. Eurozone June PPI was 0.8% M/M (vs 0.9% cons, -0.6% prior).

- The UK final July services PMI was revised up to 51.8 (vs 51.2 flash), but labour market details remain weak.

- Broader focus remains on Thursday’s BOE decision. MNI preview here.

FOREX: USD Index Awaiting Directional Input from Trump's Appointments

- Markets are in consolidation mode Tuesday, with the USD Index holding well above the weekly low. Focus for markets near-term is on the trajectory of the USD from here: whether the USD shift lower on NFP is the start of a resumption of the YTD downtrend, or a corrective pullback as part of the recovery off the oversold condition. This leaves Trump's appointments at both the BLS and Fed this week in sharper focus - as he's expected to appoint a governor to replace Kugler that favours his preference for lower policy rates, as well as a BLS head willing to look into Trump's concerns over government data.

- As a result, the key parameters for the USD Index remain unchanged: the 50-dma undercuts as support at 98.293, while 99.241 marks the 50% retracement for the NFP downleg.

- CHF remains a currency of concern as the Swiss-US governments are yet to reach a broader trade agreement after the installation of 39% tariffs on Swiss exports to the US. The Swiss Franc is among the poorest performers in G10 for a second consecutive day despite yesterday's firmer-than-expected Swiss July CPI print. While USDCHF continues to hover around its 0.8092 50-dma, Franc weakness arguably stands out the most against the Japanese Yen, with CHFJPY losses over the last three sessions exceeding 2.1%.

- A swift tariff resolution here is expected to prove CHF positive - but for now, notable tariff premia holds over the currency.

- The session ahead sees ISM Services Index data - currently expected to rise to 51.5 from 50.8 prior, although prices paid is seen moderating slightly. US and Canadian trade balance stats also cross.

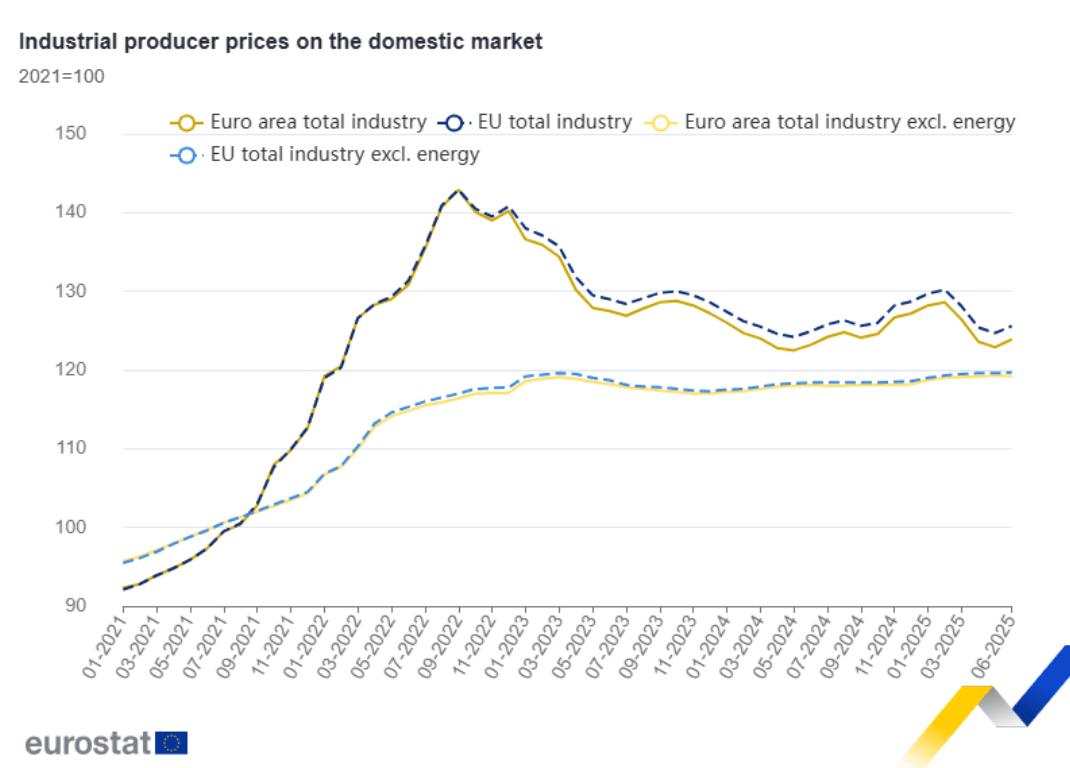

EUROPEAN INFLATION: PPI ex-Energy Moderates But With Mixed Drivers

Eurozone PPI inflation was as expected in June on a Y/Y basis at 0.6% after 0.3% in May, despite a small miss for the M/M at 0.8% (cons 0.9) after -0.6% M/M - all NSA data.

- Energy PPI deflation slowed from -1.5% in May to -0.1% Y/Y (highest since March) amid a firm 3.2% M/M jump in the category.

- PPI ex-energy inflation meanwhile eased from 1.1% to 0.9% Y/Y for the lowest rate since November.

- Across the non-energy categories, Y/Y rates were mixed vs May: Non-durable consumer goods at 2.0% (1.9% May), durable consumer goods at 1.5% (1.4% May), and capital goods stayed put at 1.7%. Intermediate goods meanwhile moved into negative territory, at -0.1% Y/Y (0.2% May) for the first time since last November (at least before potential revisions to the data).

- Whilst there recently appears to be only limited impact of disinflationary effects from potential Chinese goods re-routing to Europe under Trump administration trade policy, the further moderation in intermediate goods inflation is worth watching. That said, whilst small parcel taxes have been considered in some countries such as France as a possible anti-dumping measure, we note that industrial prices of consumer goods are still growing more solidly.