US DATA: UMich Survey Revisions Should Ease Stagflationary Concerns

May-30 14:20

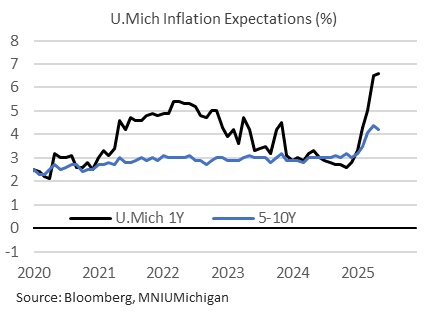

The sharp drop in UMichigan inflation expectations in the final versus preliminary report for May (1Y to 6.6% vs 7.3% prelim, 5-10Y to 4.2% vs 4.6% prelim) largely if not entirely reflects the timing of the survey before and after the US-China tariff climbdown on May 12.

- Indeed the survey dates (prelim survey period ended May 13, but the final survey deadline was May 26) are key to any interpretation of the report, which noted that "sentiment had ebbed at the preliminary reading for May but turned a corner in the latter half of the month following the temporary pause on some tariffs on China goods."

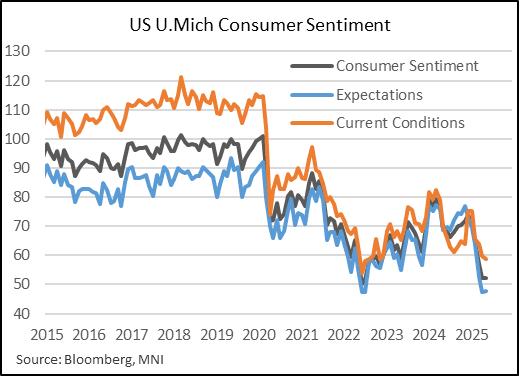

- The headline sentiment figure was revised up 1.4pp to 52.2, leaving it unchanged from April, with current economic conditions up 1.3pp to 58.9 (59.8 April), expectations up 1.4pp to 47.9 (47.3 Apr), and the household finance index up 3pp to 67.

- Even though the improvement vs prelim had been expected, the May final report looks better than consensus anticipated and will alleviate some concerns over a stagflationary consumer outlook that had looked among the worst in survey history.

- Make no mistake, these are very worrying figures for the outlook in their own right.

- But in particular, longer-term inflation expectations appear to be turning a corner lower, after a 4.4% peak in April, potentially giving the Fed (some of whose members had mentioned some concern over the UMich survey, even if only skeptically) a bit more confidence that higher expectations aren't becoming entrenched.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US DATA: Recapping Latest PCE Inflation Trends

Apr-30 14:18

Core PCE:

- 2.65% Y/Y drops from 2.96% in Feb for lowest since Jun 2024. However:

- 3.5% annualized over three months vs 2.4% in Dec

- 3.0% annualized over six months

Supercore PCE:

- 3.25% Y/Y from 3.65% in Feb for lowest since Jan. Recent trends also running hotter:

- 3.9% annualized over three months vs 3.7% in Dec

- 3.8% annualized over six months

PIPELINE: Corporate Bond Update: $1.25B NIB & $1B CoE Priced

Apr-30 14:12

- Date $MM Issuer (Priced *, Launch #)

- 04/30 $1.25B *Nordic Investment Bank 5Y SOFR+43

- 04/30 $1B *CoE Dev Bank 3Y SOFR+36

- 04/30 $Benchmark IADB 5Y SOFR+44

- 04/30 $Benchmark BNP Paribas 4NC3 fix/SOFR, 6NC5

- 04/30 $Benchmark Bahrain 12Y 7.5%, 8Y Sukuk 6.25%

EUROPEAN INFLATION: Slight Upside Risks For April EZ Core HICP - Analysts

Apr-30 14:09

Sellside analysts tend to see slight upside risks vs their initial estimates on EZ April Flash HICP (consensus stood at 2.1% headline and 2.5% core ahead of the national-level data released since yesterday, our full preview here) - overall, analysts are looking for for core somewhere between 2.5% to 2.6% now:

- Barclays: "We track EA headline and core HICP at 2.0% y/y and 2.5% y/y, respectively. This is in line with our forecast for headline inflation but 0.1pp higher than our forecast for core due to relatively firm data from Italy and Spain."

- Berenberg: "Eurozone inflation may not (yet) fall all the way to the 1.9% yoy rate we are forecasting for April. The expensive Easter holiday season seems to have contributed to stubborn services inflation in April. As this effect unwinds in May, inflation will likely decline further next month."

- Commerzbank: "We maintain our eurozone forecast that inflation in April is likely to have slightly fallen from 2.2% to 2.1%. However, we see upside risks to our forecast that the core rate has likely remained at 2.4%."

- Goldman Sachs: "We upgrade our Euro area headline inflation forecast for April to 2.12%yoy, from 2.11%yoy previously [2.09% initial]. We also revise up our Euro area core inflation forecast by 8bp to 2.63%yoy [2.54% initial], mostly driven by stronger-than-expected French and Italian core pressures. This would imply seasonally adjusted sequential core inflation of 0.25%mom in April on our estimates."

- JP Morgan: "Euro area headline inflation likely declined a tenth to 2.1%oya, with risks tilted towards a 2.0%oya reading. Core data, meanwhile, suggest that the Euro area core inflation likely increased more than we expected. We thus raise our Euro area core forecast from 2.5%oya to 2.6%."

Trending Top

Mar-27 20:13